Research Report | Blockchain launches innovation in the underlying infrastructure of financial infrastructure and advances to the 3.0 stage of the enabling industry

Source of this article: Chuancai Securities

Author: Chen Fang Gimli Branch Zhou Zirui

I. Financial industry innovation triggered by blockchain

1.1 Phase 2.0, financial blockchain is the focus

The origin of the blockchain is relatively late, and the epidemic has catalyzed new opportunities for development of the blockchain. The origin of the blockchain is relatively late. The development of the industry is at an early stage. There are many difficult problems objectively, but opportunities are constantly emerging. The outbreak of the epidemic has driven changes in social life models and business models. The demand for digital transformation in all walks of life has surged. The epidemic has stimulated more application scenarios and forced the development of blockchain. At present, the business opportunities brought by the epidemic to the blockchain industry are mainly in public early warning systems, followed by material tracing and public opinion monitoring. At the same time, identity information registration and financial services are also optimistic. On the other hand, compared to emerging technologies such as cloud computing and artificial intelligence, the development history of blockchain is only about ten years. It belongs to a brand new circuit. The gap between countries is not large, and China is more likely to have the right to speak internationally. Occupy the commanding heights of technology.

- 10% of net worth bets on BTC, ETH makes a net profit of 1.5 billion, Wall Street giant Mike's road to crypto kingdom?

- Blockchain security | 19 security incidents in March, DeFi security issues highlighted

- Tether's market value exceeds $ 6 billion. Investors "load bullets" are ready to make a dip?

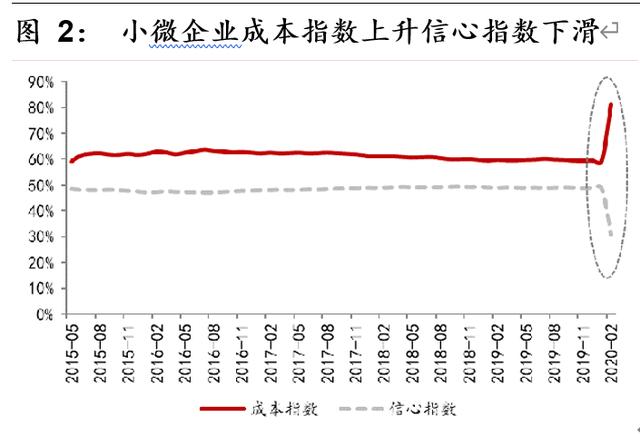

Affected by the new crown epidemic, 85% of corporate cash could not be maintained for more than 3 months, the confidence index of small and micro enterprises fell to 30.6% from 49.1% at the end of 2019, and the cost index rose to 81.4% from 59.6% at the end of 2019. The SME loan demand index in 2019 is greater than 50%, and it may exceed 80% in 2020. However, the bank loan approval index continued to fall below 50%, and the financing gap of SMEs at the long end of the supply chain has not been effectively filled.

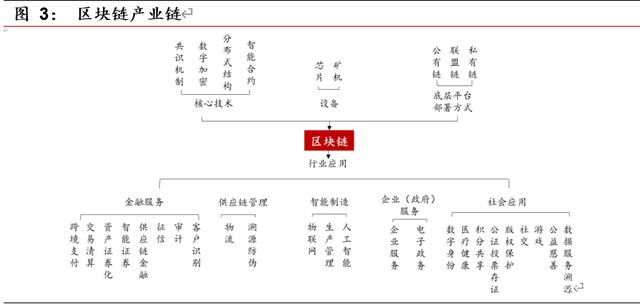

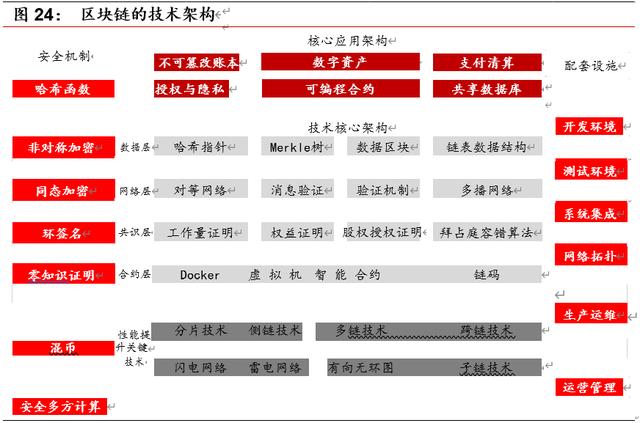

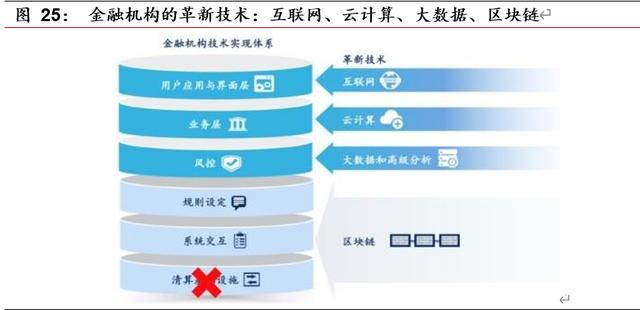

The upstream of the blockchain industry chain includes core technology, equipment, and underlying platform deployment methods. The downstream includes finance, supply chain management, intelligent manufacturing, enterprise (government) services, and social applications. The core technologies are mainly consensus mechanism, digital encryption, distributed structure and smart contracts. The equipment includes chips and miners. The underlying platform deployment methods can be divided into public chains, alliance chains, and private chains. In the "China Blockchain Technology and Application Development White Paper (2016)" issued by the Ministry of Industry and Information Technology of China on October 18, 2016, finance was clearly identified as the first application area of blockchain technology.

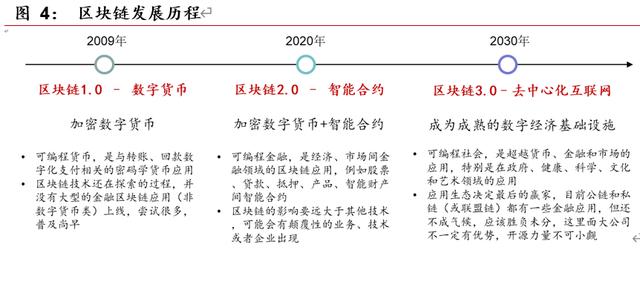

Currently in the 2.0 stage of the blockchain, it is moving towards the 3.0 stage of the enabling industry. Blockchain technology continues to expand application scenarios in all walks of life, especially in the financial field. Blockchain technology has the inherent advantage of optimizing the financial infrastructure. Blockchain is naturally suitable for transforming payment settlement systems, and has outstanding significance in the fields of digital currency and payment, digital bill and letter of credit innovation, and registration and trading of financial products such as securities. Now it has transitioned to the 2.0 smart contract stage, that is, programmable finance can promote financial industry infrastructure innovation. In 2019, the highest level collectively learns about blockchain. Under the dual promotion of policies and markets, the pace of blockchain technology enabling the real economy is accelerating, and blockchain is moving towards the 3.0 stage of enabling industries.

The development of blockchain technology was initially promoted by the financial industry, and blockchain has a natural and close relationship with finance. As the technical solution of "Bitcoin" and the birth of the blockchain, "Bitcoin" can be understood as a peer-to-peer electronic cash payment system, and payment is an important basis for all financial activities. In 2015, blockchain technology was separated from the concept of "Bitcoin" and became an independent research direction, mainly relying on the promotion of the financial industry. At present, the banking, insurance, and securities industries have begun their actual landing attempts. The application scenarios mainly include digital currency, payment clearing, digital bills, asset securitization, supply chain finance, bank credit, loan business, asset transfer and equity transactions, KYC information transfer, etc.

1.2 Macro Impact of Blockchain on Financial System

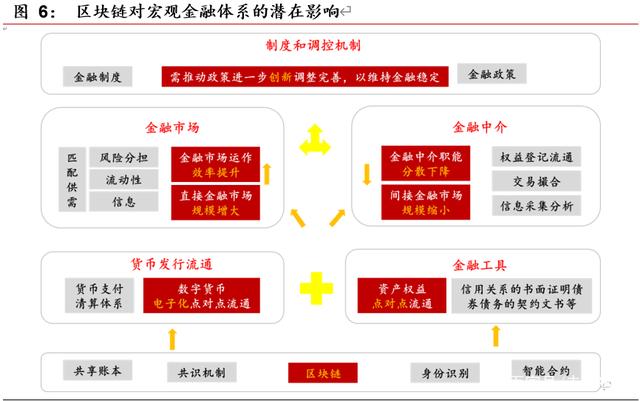

The analysis of the impact of blockchain on the financial sector should first be considered from the macro level of the financial system. By analyzing the specific impact of the blockchain on the constituent elements of the financial system, the overall trend of its application in the financial field is judged. The financial system consists of currency issuance and circulation, financial instruments, financial markets, financial intermediaries, institutions and regulatory mechanisms. Blockchain will affect these five core components through "one rise, one drop, and three innovations", bringing potentially positive effects to the financial system.

(1) "One Liter": The innovative application of electronicization and point-to-point circulation of encrypted digital tokens and financial asset rights based on the blockchain can enhance the point-to-point relationship between investors and borrowers in the financial process. Improve the operating efficiency of financial markets, thereby increasing the size of direct financial markets.

(2) "One drop": The improvement of the efficiency of financial markets may lead to the decline, focus and even change of the function of financial intermediaries. The reduction of the size of indirect financial markets The future function of financial intermediaries will mainly be aimed at the realization of transactions between investors and borrowers, The most important functions of information collection and analysis, rights registration and circulation.

(3) "Three innovations": the first "innovation": the impact of blockchain on financial markets and financial intermediaries will promote the adjustment and improvement of financial systems and regulatory mechanisms to maintain currency stability and Financial stability. The second "innovation": based on the blockchain, encrypted digital tokens realize remote point-to-point circulation of asset rights and interests, and gradually stimulate the discussion of the application of blockchain in currency issuance and circulation. The third "innovation": financial instruments (financial assets), as an important means for investors and borrowers to transfer funds, blockchain can innovatively achieve efficient peer-to-peer registration and circulation of financial asset rights.

On October 24, since the highest-level collective learning of the blockchain, the blockchain has attracted much attention, related policies have been intensively introduced, and industry standards have gradually come into effect. After the 1024 meeting, the introduction of blockchain-related policies at the national level has further accelerated. According to IPRI statistics, as of 2019, the central ministries and commissions issued as many as 45 blockchain-related support policy information. Only in January 2020, there were 11 The introduction of policy information to promote the integration of blockchain and various fields, and the blockchain has gradually advanced in many technological rankings. On February 5th, the "Technical Security Specification for Financial Distributed Ledgers", known as "the first blockchain standard in the domestic financial industry," was officially released. Compared with the previous, this "Specification" is mainly aimed at the financial industry, and puts forward higher requirements on user management, regulatory support, and privacy protection of distributed ledgers. Financial blockchain has reference benchmarks in all aspects of architecture design, module functions, software interfaces, etc., and these benchmarks are at the forefront of the world. At the same time, the Blockchain Research Group of the Digital Currency Research Institute of the People's Bank of China also wrote an article entitled "Development and Management of Blockchain Technology" to clarify the "right and wrong" and "authenticity applications" of the blockchain. During the epidemic, blockchain technology also played a role in boosting corporate financing.

1.3 Blockchain responds to micro pain points in the financial industry

In financial scenarios such as insurance, supply chain finance, and asset securitization, the large number of participants, the high cost of credit evaluation, and the low settlement efficiency of intermediaries have led to long-term information asymmetry (security) in the financial industry and high cost of information verification ( Trust), complex and redundant processes (efficiency), etc. The core meaning of finance is to improve the level and efficiency of investment and financing, and to better complete asset allocation. Therefore, security, trust and efficiency have become important factors restricting the level of financial development.

Blockchain is not a disruptive technology, but an integrated innovation of multiple technologies. The blockchain integrates a number of basic technologies such as distributed accounting, immutability, and built-in contracts, and builds a trust mechanism at a lower cost. The advantages of blockchain technology can effectively solve the pain points in the above financial scenarios. All market participants can obtain all transaction information and asset ownership records in the market without any difference, effectively solving the problem of information asymmetry; at the same time, based on transparent information and a new trust mechanism between participants, there is no need to expend human, material and financial resources The information is true, which will greatly reduce the cost of trust between institutions and thus the price of financial services; embedded smart contracts reduce the error rate in the payment and settlement process, simplify processes and improve efficiency.

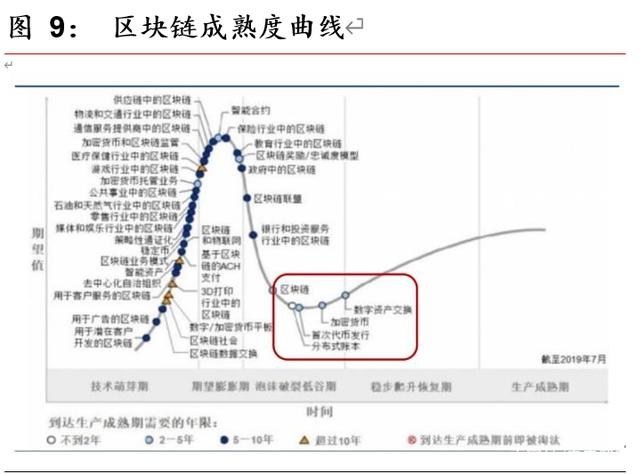

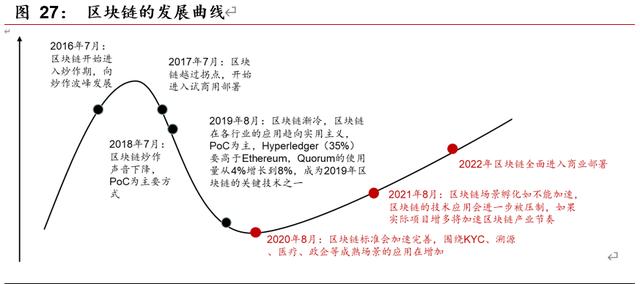

According to the two dimensions of technology maturity and impact, emerging technologies can be divided into four categories: key applications, tracking experiments, appropriate introduction, and selective attention. Blockchain technology has a low maturity but a high degree of impact, so financial institutions' adoption of blockchain technology is tracking experiments. According to the blockchain maturity curve released by Gartner in July 2019, digital asset exchanges, cryptocurrencies, and initial coin offerings were the first to pass the bubble burst trough and are about to enter a period of steady climb recovery. Blockchain in the banking and investment services industry After experiencing the expected expansion period, the bubble burst trough period, and the blockchain in the insurance industry has just passed the industry inflection point.

At present, blockchain technology is basically in the proof-of-concept stage in the financial field. Major financial institutions have launched blockchain pilot projects, but have not yet launched large-scale commercial use. There have been some blockchain pilot projects of financial institutions in the fields of digital bills, accounts receivable management, letters of credit, and asset securitization.

Second, the development status of the blockchain-enabled financial industry

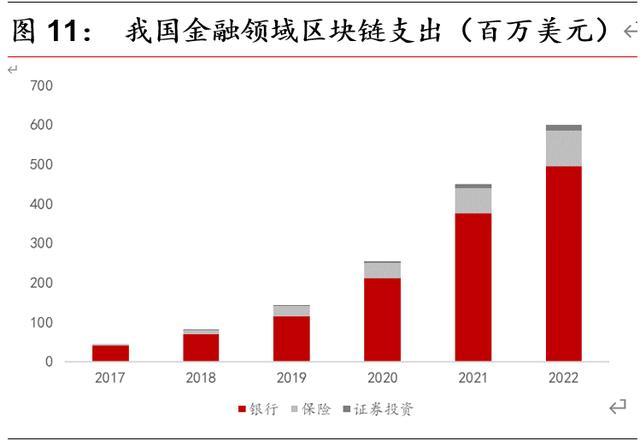

The scale of the blockchain market has maintained rapid growth. Finance has invested the most in blockchain technology, with banks accounting for the highest proportion. According to IDC, the scale of China's blockchain market expenditure in 2018 was US $ 160 million, a year-on-year increase of 108%. It is expected to maintain rapid growth in the next three years, with expenditure reaching USD 1.67 billion in 2022 and a compound growth rate of 83.9% in 2017-2022. IDC recently released the top ten predictions for the Chinese blockchain market in 2020: By 2023, Chinese companies will invest $ 2.7 billion in blockchain services, accounting for 29 of corporate management service spending. From the perspective of the industry, the financial industry has an absolute leading position. Of the global blockchain market share in 2018, the financial industry accounted for 60.5%, the manufacturing and resource industries accounted for 17.6%, the service industry accounted for 14.6%, and the public sector and infrastructure industries accounted for 4.2% and 3.1%. In the financial industry segment, the scale of banking blockchain spending accounts for more than 80% of the overall blockchain spending in the financial industry. In the next five years, the banking industry will maintain this trend and proportion.

Blockchain guarantees the system's data credibility, results credibility and historical credibility at the technical level. It is especially suitable for industry applications where the collaborators are unreliable, the interests are inconsistent, or the lack of authoritative third-party involvement. In terms of application of transformation power, obviously, the transformation of blockchain technology in the field of payment and settlement is the most obvious. However, as an important cornerstone of the financial industry, its breakthrough innovation requires top-down construction centered on the central bank. . At present, in the application of the blockchain promoted by the global banking industry and securities institutions, the development of non-standardized financial products such as bills and letters of credit circulation and unlisted private equity transactions is relatively leading. In other financial fields, the application of blockchain supply chain financial applications is the most optimistic, and emerging platforms of banks and the Internet have shown a trend of diversified competition. The core difficulty of solving the problem of data islands in the insurance and credit reporting fields is that the popularity of blockchain technology is not enough, and the motivation for traditional technology solutions to self-optimize is not strong.

2.1 Cross-border payment: high maturity

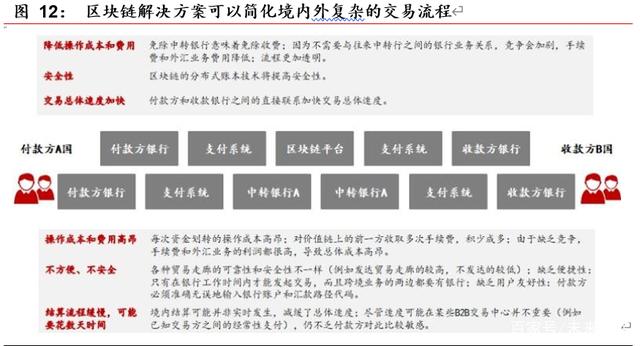

Blockchain is not yet suitable for high-concurrency scenarios such as traditional retail payment. It is suitable for areas that have high requirements for trusted information sharing and low requirements for concurrency. Because the blockchain needs to store a large amount of redundant data and co-calculate, it will sacrifice The system handles performance and some of the customer's privacy. Payment clearing is the second largest financial sector in terms of the popularity and maturity of blockchain applications. Among them, cross-border payment is a typical example. The payment and settlement process is a typical multi-center scenario, which has a high degree of matching with the characteristics of the blockchain. Domestic and foreign market players have begun to apply blockchain technology to cross-border payment scenarios. Some central banks have tested blockchain (DLT) technology as an alternative technical solution for large-value payment systems.

Cross-border payments have pain points such as low efficiency, high costs, and high thresholds. Cross-border payment refers to the act of transferring funds across two or more countries or regions due to international trade, international investment, and other aspects of international bond debts through the use of certain settlement tools and payment systems. According to Egerson, cross-border payments processed between banks each year range from $ 25 to $ 30 trillion, with transaction volume reaching 10 to 15 billion. In the current cross-border payment process, each transaction needs to be transmitted between multiple institutions. Currently, the bank's cross-border payment mainly uses the SWIFT system. Cross-border payment still has high intermediate fees, low payment efficiency and centralization Hidden dangers and other issues. At the same time, SWIFT uses a membership system, which has a high barrier to entry. Compared with the traditional cross-border payment model, the blockchain-based cross-border payment model has the advantages of higher efficiency, lower cost, more liquidity, and more equal rights. The process of cross-border payment can be divided into four stages: the payment initiation stage, the fund transfer stage, the fund delivery stage, and the post-transaction stage. Each stage has a corresponding pain point and a blockchain solution.

Ripple is the earliest and most mature solution for cross-border payment blockchain applications. Developed by Ripple Labs in 2012, Ripple is an open source internet protocol for financial transaction settlement. By the end of 2017, Ripple had realized real-time global payments across 27 countries, and many of the world's leading banks were participating in Ripple's technical testing and related cooperation. The current Ripple system can reduce the liquidity losses, payment fees, exchange fees, and capital operation costs involved in correspondent banks and SWIFT. According to Ripple's estimation, the cost of each interbank transaction will decrease from US $ 5.56 to US $ 2.21, a 60% reduction. Based on the number of more than 3 billion payment messages completed through SWIFT in 2016, approximately US $ 10 billion can be saved in 2016 cost of.

2.2 Supply chain finance: current demand is large

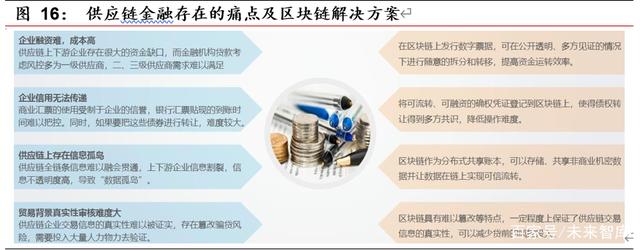

Supply chain finance refers to the core enterprises in the supply chain and related upstream and downstream enterprises as a whole, relying on the core enterprises and the premise of real trade, using self-repaying trade financing methods, Comprehensive financial products and services provided. According to the forecast of the Institute of Foresight Industry, the market scale of China's supply chain finance will maintain a steady growth. By 2020, the scale of China's supply chain finance market may reach 15 trillion yuan. At present, there are four main types of financial products in the supply chain: receivables, prepayments, inventory and credit products.

During the resumption of work and production, the policy repeatedly mentioned supply chain finance. On February 18th, the Ministry of Industry and Information Technology issued the "Notice on the Use of New Generation Information Technology to Support Epidemic Prevention and Resumption of Work and Resumption of Work", emphasizing the promotion and application of supply chain finance based on models such as online services through strengthening scientific and technological capabilities to protect enterprises Funding needs for resumption of work and production to prevent capital chain breaks. On March 13, the Information Office of the State Council held a press conference on “Supporting the Relevant Resumption of Production and Collaboration in the Industrial Chain”. The meeting emphasized the use of fintech to optimize the supply chain financial services, and encouraged qualified financial institutions to develop supply chain business systems and adopt The combination of online and offline provides customers on the chain with more convenient and efficient supply chain financing services.

With the rapid development of supply chain finance, many problems and challenges have emerged. There are corresponding solutions to different pain points of blockchain technology. To sum up, supply chain finance faces four major challenges: First, it is difficult for companies to raise funds, and their costs are high; Second, corporate credit cannot be passed; Third, there are islands of information in the supply chain; Fourth, it is difficult to verify the authenticity of the trade background . By issuing digital bills on the blockchain, the efficiency of fund operation can be improved; the transferable and financing confirmation vouchers can be registered on the blockchain so that the creditor's rights are transferred to multiple parties to reduce the difficulty of operation; distributed shared ledger storage and shared non-commercial Confidential data and the credible flow of data on the chain; the tamper-resistant characteristics of the blockchain guarantee the authenticity of the supply chain transaction information to a certain extent, thereby reducing the risk control investment before the loan.

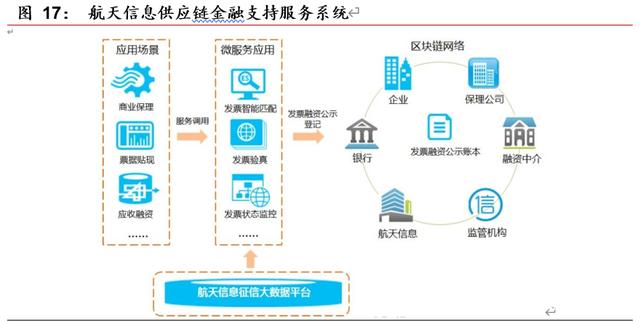

Aerospace Information seizes the development opportunities of blockchain technology and carries out a series of innovations and transformations in taxation and finance. In 2016, Aerospace Information began to study blockchain technology, explore typical applications, and prepare for the large-scale application of blockchain technology. After two years of continuous tracking and research and development, Aerospace Information has developed an independent intellectual property rights-oriented basic development platform for enterprise-level applications-the blockchain technology development platform. It has been in the application of national secret algorithms, transaction throughput, and massive data processing. Leading industry. The company currently forms a full-time blockchain technology research and development team to develop a series of application products in the three major fields of gold tax, finance and the Internet of Things. Aerospace Information is based on the supply chain financial application research of the blockchain. Through distributed ledger technology, the payment commitments of core companies are transferred between multi-level suppliers on the chain, and the core enterprise credit is passed to small and medium-sized enterprises that need financing.

2.3 Insurance: Broad prospects for the future

The insurance industry regards trust as its core value proposition, and blockchain technology inherently carries a gene of trust, so insurance has become one of the most ideal landing scenarios for blockchain. In essence, insurance is a social and economic institutional arrangement. The collection and coordination of individuals is an important foundation and core connotation of its existence, and ultimately it is the realization of social mutual assistance based on market mechanisms. According to PricewaterhouseCoopers, more than 20 of the blockchain application scenarios currently underway around the world involve insurance.

At present, the insurance industry still has problems such as misleading consumption, low claims efficiency, inability to share industry information, cheating insurance claims, and distrust of insurance. Blockchain is tamper-resistant and can implement smart contracts on this basis, which can be used to optimize insurance business processes. On the one hand, to achieve user information consistency management: insurance companies can provide user information blockchains, and users who have been verified and verified can write information into the blockchain. There is no need to repeatedly enter personal information when purchasing different insurances, just query on the blockchain. , Shorten the insurance time. On the other hand, automatic claim settlement: combining the blockchain with smart contracts, once the specific risk conditions are met, claims can be quickly settled, and once the smart contract is triggered, compensation is automatically paid, which better protects the interests of insurance consumers and increases customer satisfaction. . In addition, it reduces human error, saves labor costs, and saves 15 to 20 operating expenses for reinsurers.

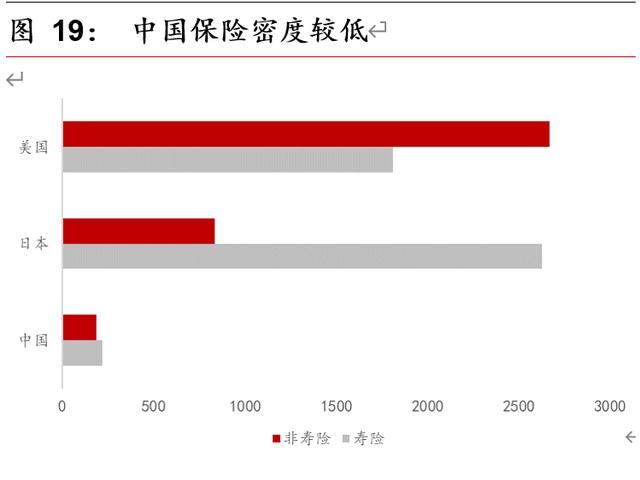

The development prospect of China's insurance industry is good, but there is still a large gap with mature markets. Benefiting from factors such as stable economic growth, continuous accumulation of social wealth, changes in population structure and policy dividends, consumers' ability to purchase insurance and willingness to buy insurance have continued to increase, and the scale of China's insurance market has maintained rapid growth. In August 2016, the "13th Five-Year Plan" for China's insurance industry issued by the China Insurance Regulatory Commission clearly stated that by 2020, the national insurance premium income will reach about 4.5 trillion yuan, the insurance depth will reach 5, and the insurance density will reach 3,500 yuan. / Person, the total assets of the insurance industry strive to reach about 25 trillion yuan. The scale of China's insurance market has grown rapidly, but it is still in the primary stage of development compared with developed markets, and the insurance depth and insurance density are still at a relatively low level.

In recent years, a large number of insurance companies have begun to deploy blockchain business. From the perspective of specific applications, the current exploration of insurance companies in the field of blockchain can be divided into two categories: one is based on the "open ledger" capability of the blockchain, which brings business data on the chain to achieve information disclosure. The other is trying to build an insurance industry alliance chain. Different types of insurance companies have different layouts. Traditional insurance giants apply blockchain to insurance products, and technical insurance companies focus on developing B-side blockchain platforms.

In addition to the maturity of the blockchain technology itself, institutional participation and the amount of public chain data are also key factors that affect the value of blockchain applications. Judging from the current investment status of blockchain and the development status of blockchain in insurance companies, blockchain technology is still in the exploration and trial stage in the insurance industry, and there is still some time before large-scale application. With the blockchain being raised to the national strategic height in 2019, the insurance regulator is also actively promoting the formulation and research of industry rules. It is expected that the next 5-10 years will be a golden time for the rapid development of the insurance blockchain.

2.4 Credit Report: Credit Society Can Be Expected

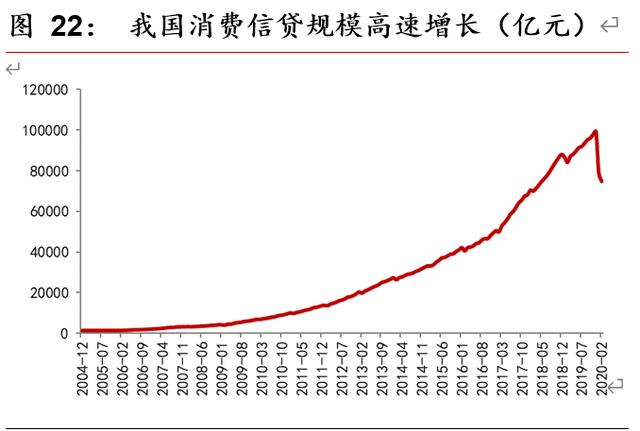

China's credit information industry is dominated by corporate credit information, personal credit information needs to be developed, and the overall market prospects are broad. The credit development of Chinese enterprises has developed earlier and the market is relatively mature. As of October 2017, there were 137 credit reporting agencies in China that have completed filing. According to the central bank, the latest data shows that the central bank credit center includes 990 million natural person information, about 530 million people with loan records, and a coverage rate of 53.50. The remaining 460 million people have simple identification information and no other financial credit data. In addition to these 990 million people, there are still hundreds of millions of natural person information in China that have not been included in the central bank's credit reporting system. In contrast, in the United States, its credit coverage reached 92 in 2014. In recent years, China's personal consumer credit, personal business loans (small and micro loans), and housing mortgage loans have steadily increased, laying a good foundation for the development of personal credit business on the demand side. The scale of China's consumer credit has shown a rapid growth trend, and the rapid popularization of consumer credit has become one of the main driving factors for the development of the credit industry.

It is generally believed that the traditional credit reporting industry has the following pain points: (1) lack of data sharing, asymmetry of information between credit reporting agencies and users; (2) limited formal market-based data collection channels, and data source competition costs a lot of costs; (3) data privacy Protection issues are prominent, and traditional technology architectures are difficult to meet new requirements. In view of the current situation and pain points of the traditional credit information industry in China, blockchain can focus on the field of data sharing and transaction of credit information. Establish a credit information sharing trading platform to facilitate participating parties to minimize risks and costs and accelerate the storage, transfer and trading of credit data. With the development of blockchain technology, the future credit society can be expected.

Third, calm thinking after development disputes

3.1 Three Misunderstandings of the Blockchain Finance Industry

3.1.1 Blockchain is a new technology

Blockchain technology is the fusion and derivation of multiple mature technologies. From the perspective of technological innovation, blockchain is the result of integrating and innovating theories and technologies across different fields such as computers, distributed systems, and cryptography over the past decades. At present, a blockchain technology system mainly based on distributed systems, P2P networks and cryptography, supplemented by a variety of improved technologies has been formed.

3.1.2 Blockchain has a disruptive effect on the financial system

We believe that blockchain will bring technological innovation to financial infrastructure and will not have a disruptive effect on the financial system. The application of blockchain technology in the financial industry is still in the process of gradual development and evolution. The application of blockchain in the financial field is only to provide a new solution for the issue and circulation of asset equity certificates from a new perspective. Judging from the fact that the blockchain has not had a subversive effect on the production relationship in the financial field, the function of the blockchain cannot be exaggerated or superstitious. In the development process of the modern financial system, technological innovations that are conducive to improving the efficiency of financial resource allocation and improving the security and convenience of financial transactions will be integrated into the financial system.

3.1.3 Blockchain "decentralization" means "deregulation"

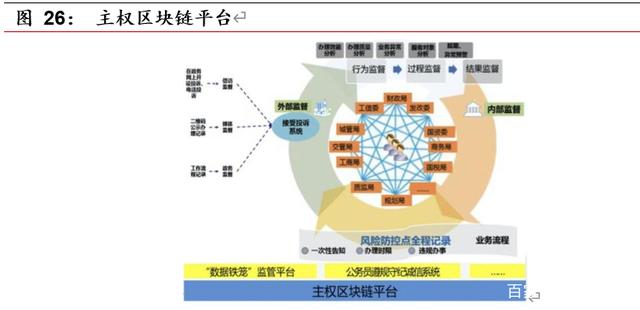

The most obvious feature of the blockchain is decentralization, but decentralization does not mean that there is no center, it may just weaken the center, but it is still under supervision. The value of mediation is compressed, but the mediation function cannot be completely replaced. Decentralization and deregulation are two different concepts. In the weakened center's institutions, how regulators can play a role needs to be considered. There can be many supervisory means in a peer-to-peer system, and the characteristics of the blockchain can even make some existing supervisory technologies more intelligent, making the work of supervisory authorities more real-time and forward-looking. Innovations in the financial industry often need to follow the guidance of the supervisors, and always take security and reliability as the first requirement. The updating and replacement of the underlying financial infrastructure has special caution and requires a long verification process. The Guiyang Municipal People's Government Press Office published "Guiyang Blockchain Development and Application". The white paper repeatedly emphasized that the development of blockchain technology must be placed under the scope of national sovereignty, and under the laws and supervision.

3.2 Development Outlook of Blockchain Finance Industry

2019 is an industry inflection point for blockchain, moving from PoC to trial business. 2019 to 2021 is the key three years for the success of blockchain technology. Blockchain standards and projects determine whether the technology can be commercialized on a large scale. The global blockchain space will be $ 18.4 billion in 2022, and the global blockchain CAGR will be 72.4%, maintaining high growth. It is estimated that by 2022, China ($ 1.4 billion) and APeJC ($ 8.67 billion) will surpass the United States (4.2 billion USD) and become the main battlefield of the global blockchain.

3.2.1 Banks continue to increase investment in science and technology

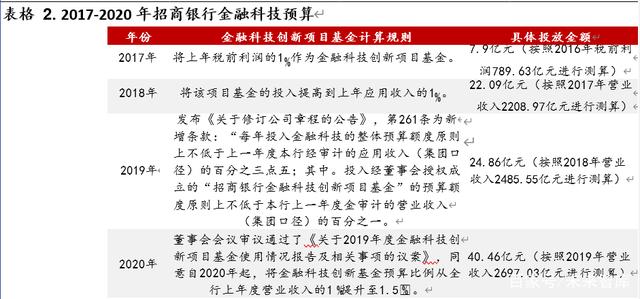

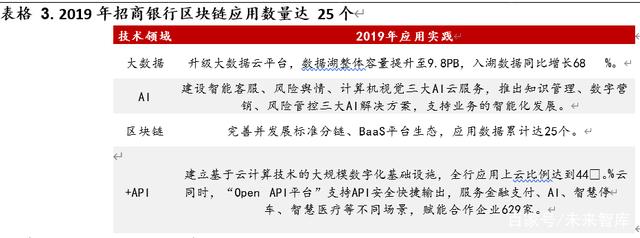

In the future, banks will continue to increase investment in fintech and support emerging technologies such as blockchain in more financial scenarios. According to China Merchants Bank's 2019 annual report, information technology investment was 9.361 billion yuan, a year-on-year increase of 43.97%, which was 3.72% of operating income. In 2019, China Merchants Bank became the first commercial bank in China to include the proportion of financial technology investment in its articles of association. On March 18, 2020, on the eve of the release of the 2019 annual report, China Merchants Bank held a meeting of the board of directors to consider and approve the "Proposal on the Use of Fintech Innovation Project Funds in 2019 and Related Matters", and agreed to start the Fintech Innovation Fund from 2020 onwards. The budget ratio increased from 1% of the bank's previous year's operating income to 1.5%. In addition, China Merchants Bank also has a fintech innovation project fund. 2017 is the first year that China Merchants Bank established the fintech innovation project fund. For the four years to date, the proportion of the fund budget has been continuously increased every year.

3.2.2 Blockchain integration with emerging technologies

Blockchain and artificial intelligence, big data, cloud computing, Internet of Things and other technologies promote each other, integrate and develop, create greater value space, and accelerate the commercial implementation of emerging technologies. As one of the new generation of information technology, the integration of blockchain with cloud computing, Internet of Things, artificial intelligence and other technologies will bring greater development opportunities. Cloud computing has low cost, rapid adjustment, and high reliability, which can help small and medium-sized enterprises to deploy the blockchain at a low cost in a short period of time. Big data has data storage and analysis technologies that can increase the value and use of blockchain data; The development of the next generation mobile communication network, the transmission speed is continuously accelerating, the blockchain data can reach the ultimate synchronization, improve the performance of the blockchain, and expand the application scope of the blockchain; the decentralized characteristics of the blockchain provide self-service for the devices in the Internet of Things Governance methods to achieve distributed decentralized control of the Internet of Things; blockchain-based artificial intelligence can set effective and consistent device registration, authorization, and perfect life cycle management mechanisms, which is beneficial to improving artificial intelligence user experience and security .

The full name of BaaS is Blockchain as a Service. The concept was first proposed by Microsoft and IBM, that is to provide one-stop service for blockchain developers and entrepreneurs, and provide complete blockchain services according to their needs. Using BaaS can extremely Greatly reduce the cost of implementing the underlying technology of the blockchain, and simplify the construction and operation of the blockchain. BaaS is one of the ways to combine cloud computing and blockchain technology. At present, the efficiency of the blockchain BaaS platform is relatively high, providing developers with a convenient development environment and supporting different scenarios development services such as public, alliance, and private chains. Most of the existing BaaS scenarios should be finance, traceability, and supply chain.

Fourth, investment advice

Since the formal implementation of the “ Regulations on the Management of Blockchain Information Services '' on February 15, 2019, the National Internet Information Office has organized filing and review work in accordance with laws and regulations, and issued the first batch of 197 domestic blockchains on March 30, 2019. Information service names and filing numbers. On October 18, 2019, the second batch of 309 domestic blockchain information service names and filing numbers were publicly released, most of which were banks, financial services institutions, or information technology companies.

We believe that we can focus on blockchain finance related industries, because finance is the first industry to implement blockchain technology, and it is also the industry with the most application scenarios. There are many participants in the blockchain financial industry, including traditional financial institutions, Internet companies and blockchain companies.

There are many companies in A-shares that deploy blockchain finance. We believe that we can identify listed companies from two directions: technology and application.

(1) The assessment of technical strength can start from two aspects: technical reserve capacity and technological improvement ability. The reason why technological improvement ability is important is that the current blockchain technology uses open source technology, which can be directly used and correspondingly improved for specific businesses. .

(2) Evaluation from the perspective of application can start from the two aspects of the rationality of the business scenario and the future size space. Blockchain technology is not a "universal" technology, and not all areas are suitable for integrating into the blockchain for "reconstruction". Therefore, when assessing the value of blockchain technology, we should pay attention to whether the blockchain has solved the pain points of traditional industries (whether efficiency has increased, whether costs have decreased, whether processes have improved, etc.). It is difficult to develop false demand and the investment value of true demand. It depends on the future market size. Blockchain is not centered on technology, but is based on appropriate scenarios. The applicable scenario of the blockchain is closely related to its core characteristics, and it is necessary to find the entry point of the application field and the advantages of the blockchain technology. In addition, the blockchain is inherently of an alliance nature, and multiple parties participate in the goal of completing a unified trade. Therefore, if it is an alliance chain, you can refer to the number of members in the alliance chain.

Key targets: Hang Seng Electronics, Oriental Fortune, Flush, Yuxin Technology, Changliang Technology, Radio and Television Express, Runhe Software, Yijian Shares, Zhejiang University New, Jincai Interconnection, etc.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- How to choose the cryptography technology? Revisiting the Security Model of Engineering Capability Boundaries

- Ethereum 2.0 will release the latest version of the code specification v0.11.1, giving a green light to the multi-client test network release

- MakerDAO's first debt auction ends, Paradigm becomes biggest winner

- Xi Jinping: Using cutting-edge technologies such as blockchain energy to promote urban management innovation

- QKL123 market analysis | The Federal Reserve will move again, can it survive the constant stimulation? (0401)

- Bitcoin mining revenue has increased 20-fold in 6 years. Can miners continue to make profits after halving?

- Opinion | Professor of the Chinese People's Congress: China needs to promote the construction of a sovereign digital currency to build a fair and just new international political and economic order