Token Terminal: In-depth analysis of the operating principles and economic models of common Layer1

Token Terminal: Detailed analysis of the operating principles and economic models of common Layer1s.Author: Tokenterminal

We often feel the costs and benefits of using different blockchains in a straightforward manner, namely gas fees and incentives. But do you really understand their complete economic models? Where do gas and incentives come from, and where will they flow? How do markets perform under different economic model designs?

Token Terminal explores the economic models of major L1 and L2 blockchains based on PoW and PoS, as well as emerging models of protocols such as liquidity staking. Each blockchain’s economic model principle is broken down and exemplified in a very easy-to-understand way.

At the same time, by visualizing the daily fee changes of blockchains, we also analyzed the market performance of mainstream blockchains for investors to use the framework in the article to compare the economic performance, potential, and sustainability of blockchains.

- Token Terminal: In-depth analysis of the operating principles and economic models of common Layer1s

- Rollups as a service solution: Eclipse technology principle analysis

- Origin Protocol: Dual-token model, a new player in the DeFi track

Introduction

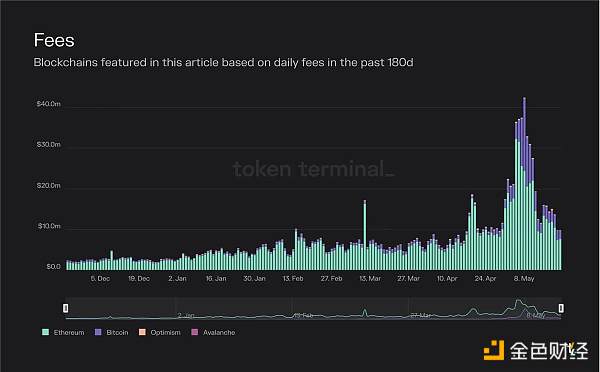

The figure below visualizes the daily fees of the blockchains mentioned in this article over the past 180 days.

Deep Tide Note: You can see that the total transaction fees of Ethereum and Bitcoin are still far ahead.

The key components that usually make up the blockchain economic structure are transaction fees, block rewards (incentives) for inflation, and fee destruction.

Transaction fees represent the market price of blockchain space.

Incentives are economic rewards that encourage people to take action (such as verifying transactions).

Fee destruction is a mechanism that removes a portion of each transaction fee from circulation.

Given the limited capacity of individual blockchains, we will see a world with multiple different blockchains – each optimized for different use cases – interoperating with each other. The blockchain market was initially dominated by Bitcoin, an extremely simple and limited contract execution environment. With the launch of Ethereum, it is (theoretically) possible to deploy any complex contracts or programs on the blockchain. Now, with the rise of scaling solutions, application-specific blockchain and cross-chain bridges, it is also possible to deploy any complex contracts in practice (scalability is no longer a restriction). In this article, we will break down the economic models of the most common types of blockchains.

L1 based on PoW

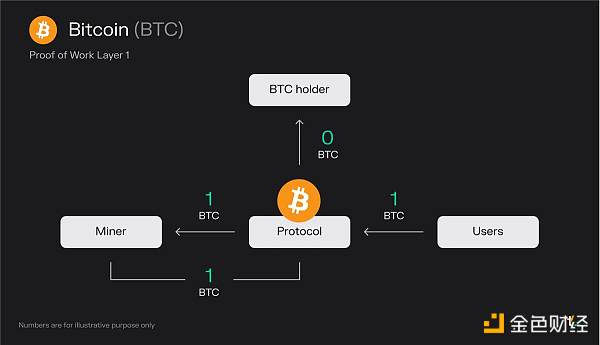

Principle Description:

-

Users pay a transaction fee of 1 BTC for a block

-

Miners receive all fees (1 BTC)

-

Miners obtain 1 BTC (newly issued BTC) from block rewards

Final Result:

-

Miners receive 2 BTC

Key Points:

-

The requirement to submit transactions on Bitcoin creates a market for block space. Users pay for block space to miners. Bulk subsidies further incentivize miners, and bulk subsidies are newly minted Bitcoins that increase the total supply of currency. Currently, all fees and block subsidies for Bitcoin belong to miners.

-

Bitcoin provides security through CPU capabilities. Bitcoin’s value proposition is to create a secure, transparent, and immutable global ledger that allows for value transfers that are trustless and irreversible. These values are maintained by security that originates from CPU usage. Each block requires a lot of CPU power to be verified on the network. Essentially, 1 CPU corresponds to 1 vote on the network. Therefore, as long as the majority of CPUs are in the hands of honest miners, the network is secure.

-

The economics of Bitcoin are determined by two variables: transaction fees and block subsidies. Transaction fees are determined based on the supply and demand of network block space. Block subsidies are inflationary rewards that increase the circulation of BTC. Currently, a block miner receives a reward of 6.25 BTC, which halves every four years. Eventually, Bitcoin will reach a maximum supply of 21 million (expected to occur around 2140), and block rewards will be composed solely of transaction fees. This means that it is crucial for users to adopt practices that keep the network economically sustainable.

L1 based on PoS

Principle Description:

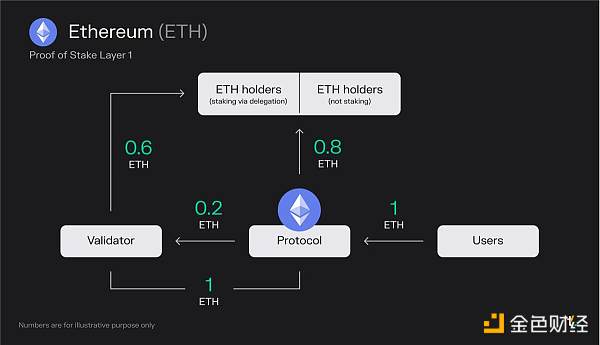

-

A user pays 1 ETH in transaction fees (including MEV) for a block

-

0.8 ETH is burnt -> “stock buyback” benefits all ETH holders equally

-

Validators earn 0.2 ETH from fees

-

Validators receive 1 ETH (newly minted ETH) from block rewards

-

As validators have already received half of the shares from the delegators, validators must share 50% of their income with these ETH holders

Final Result:

-

0.8 ETH is burned

-

Validators receive 0.6 ETH

-

ETH holders who delegated receive 0.6 ETH

Key points:

-

On Ethereum, approximately 85% of the total transaction fees are burned, effectively acting as a “stock buyback” that benefits all ETH holders equally. Meanwhile, validators earn the remaining fees and additional staking rewards, i.e., newly minted ETH. Ethereum has averaged about $15 million in fees per day over the past 30 days.

-

The fee-burning mechanism implemented through EIP-1559 in August 2021 turned ETH into a productive asset. Additionally, the transition from PoW to PoS reduced the new issuance rate of ETH. Since the Merge in September 2022, Ethereum no longer distributes block rewards to miners. This change led to a decrease of about 90% in the issuance of new ETH (the roughly 14k ETH/day block rewards were replaced by roughly 1.7k ETH/day staking rewards). This has caused ETH supply to experience deflation during periods of high usage.

-

Ethereum’s economic structure consists of three key components: total transaction fees, burned portion of transaction fees, and staking rewards. Transaction fees are determined based on the supply and demand of the network’s block space. Staking rewards are an inflationary reward that increases the total supply of ETH. Fee burning puts deflationary pressure on ETH, while a decrease in the circulating supply may increase the token’s value over time.

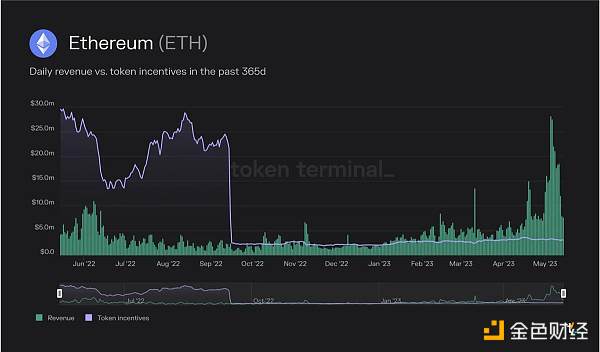

After the merge, ETH supply will remain in a deflationary state during periods of high usage. For example, in May of this year, the amount of ETH burned (revenue) was greater than the amount of ETH minted as staking rewards (token incentives).

The liquidity staking project allows users to stake their assets and maintain liquidity through derivative liquidity tokens (LSDs) that represent the underlying asset.

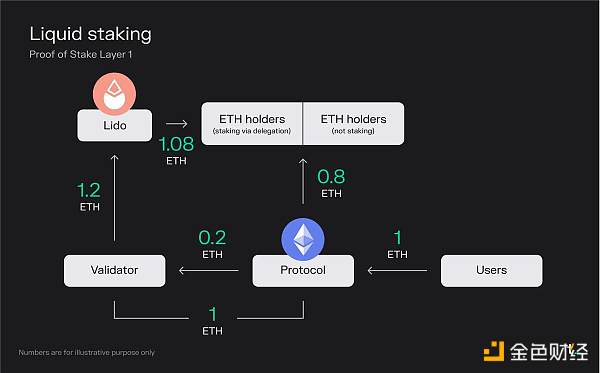

Principle statement:

-

A user pays 1 ETH in transaction fees (including MEV) for a block

-

0.8 ETH is burned -> “share buyback” lets all ETH holders benefit equally

-

Validators earn 0.2 ETH from fees

-

Validators receive 1 ETH (newly minted ETH) from block rewards

-

The validator has acquired full ownership from users who deposited ETH via the Lido liquidity staking protocol and shares 100% of the revenue with these ETH holders

-

Lido withdraws 10% (0.12 ETH) from the total staking rewards provided and distributes the remaining 90% (1.08 ETH) to ETH holders who staked through Lido

Final result:

-

0.8 ETH is burned

-

Validators receive 0 ETH

-

Lido receives 0.12 ETH (of which 50% is used to pay for node operation costs)

-

ETH holders who staked through delegation receive 1.08 ETH

Key takeaways:

-

The liquidity staking protocol enhances the user experience. Staking, which is essentially a technical and high-maintenance process, has been simplified by protocols like Lido. By allowing users to lock up their ETH and receive transferable utility tokens (stETH), Lido facilitates seamless staking while enabling users to earn rewards associated with validation activity. To provide this service, Lido charges a fee of 10% of total revenue. This fee is split evenly between node operators and the Lido DAO.

-

The technical and capital-intensive requirements of staking create opportunities for liquidity staking protocols. Traditional Ethereum staking requires users to maintain a node, commit a sizable amount of capital (32 ETH), and sacrifice token liquidity. In contrast, Lido distributes users’ tokens in bulk to validators, eliminating the 32 ETH barrier. By simplifying the user experience, providing liquidity, and democratizing staking, Lido and similar protocols are opening up a rapidly growing market space.

-

Democratization of staking allows for broader investor participation. Outside of layer 2, the liquidity staking market segment is one of the fastest growing market segments. The successful Shapella upgrade (April 12th) arguably reduced the risks associated with ETH as an investment and as a revenue-generating asset. As a result, the ETH staking ratio (staked assets/circulating market cap) is expected to grow and be on par with other PoS chains. Currently, ETH’s staking ratio is approximately 15%, relatively low compared to other PoS chains. For example, Solana and Avalanche currently have over 60% staking ratios. Given ETH’s high market cap, which is about $220 billion at the time of writing, we can expect billions of dollars in staked assets to grow in the coming quarters.

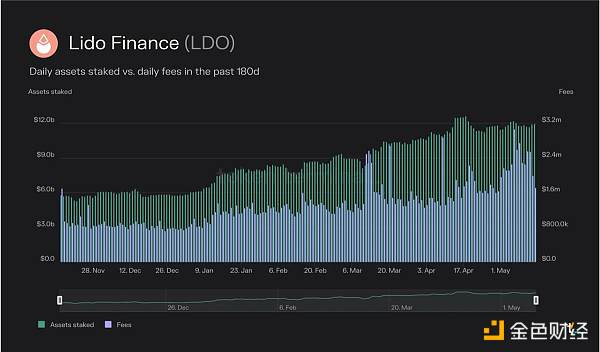

Lido has become the current market leader in the field of liquidity staking, with a total of $12 billion in staked assets. This number has grown 38% year-on-year and 105% in the past 180 days.

In the past 30 days, Lido generated $60.4 million in fees and earned 10% of that, or $6.04 million, in revenue. This revenue is split 50/50 between node operators and the Lido DAO.

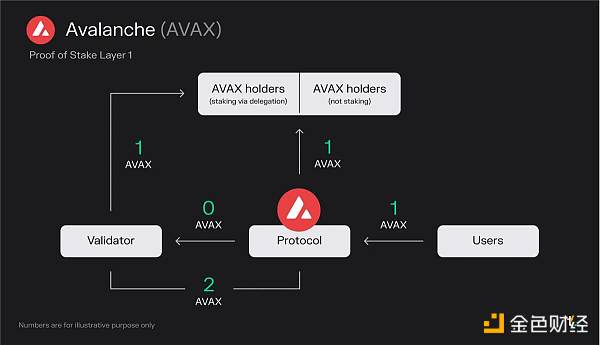

Avalanche is a blockchain (L1) that competes with Ethereum by prioritizing scalability and faster transaction speeds. It uses a novel consensus algorithm that provides strong security, fast transaction finality, and high throughput while maintaining decentralization.

Principles explained:

-

The user pays 1 AVAX for a block transaction fee

-

1 AVAX is destroyed –> “stock buyback” benefits all AVAX holders equally

-

Validators earn 0 AVAX from the fee

-

Validators receive 2 AVAX (newly issued AVAX) from block rewards

-

Since the validators have already received a portion of the stake from the delegators, they must share their revenue with those AVAX holders

Final results:

-

1 AVAX is destroyed

-

Validators receive 1 AVAX

-

AVAX holders who delegate staking will receive 1 AVAX

Key points:

-

On Avalanche, all transaction fees are destroyed, and the only source of revenue for validators is staking rewards. The burning mechanism serves as a “stock buyback” that benefits all AVAX holders equally. In the past 30 days, Avalanche has had an average daily fee of approximately $64,000.

-

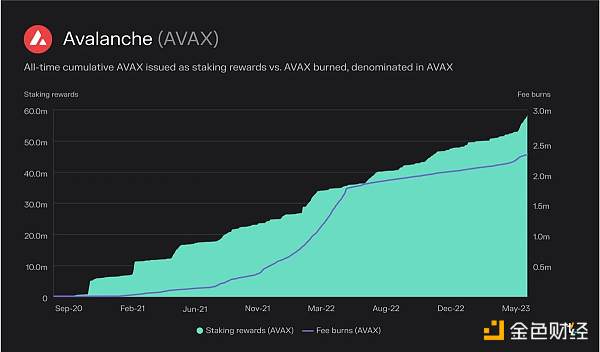

As a relatively new member of the blockchain space, Avalanche is issuing a large number of AVAX tokens to reward its validators. This approach is often used as a way to incentivize growth in the early stages of a platform. These rewards attract validators and stimulate growth and activity within the Avalanche ecosystem.

-

Avalanche’s economic model may change in the future. The fee and reward structure is not set in stone and can be adjusted based on future governance decisions. Currently, 50% of the total supply of AVAX tokens is allocated as staking rewards for validators. This distribution plan spans ten years, from 2020 to 2030. As the staking reward distribution eventually comes to an end, we may see some of the transaction fees redirected to validators in the future.

Since the network was launched in September 2020, approximately 2.3 million AVAX have been destroyed and approximately 57 million AVAX have been distributed as staking rewards.

PoS-based L2

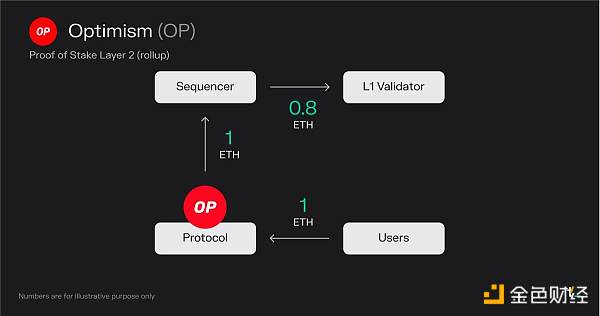

Optimism is a scaling solution (Optimistic Rollup) that aims to make Ethereum better by increasing its transaction speed and throughput. Optimism executes transactions on L2 and batches them to L1 for final confirmation. Depending on the transaction type, this results in approximately 5-20x gas reduction.

Explanation of the mechanism:

-

Users pay a transaction fee of 1 ETH for a block

-

All transaction fees (1 ETH) go to the sequencer, which is run by the Optimism Foundation

-

The sequencer pays a transaction fee of 0.8 ETH to submit transactions to L1 (Ethereum)

-

The sequencer (in this case, the Optimism Foundation) keeps 0.2 ETH as profit

Final result:

-

0 ETH is destroyed (not including destruction on Ethereum)

-

The sequencer receives 0.2 ETH

-

L1 validators receive 0.8 ETH

Key points:

-

L2 blockchain scaling applications. L2 blockchains allow widely used L1 applications such as Uniswap, Blur, and OpenSea to move their transaction activity from L1 to a separate chain that periodically settles its transactions back to L1. Currently, over 30% of Uniswap comes from L2.

-

L2 blockchain supports more optimized user experiences. As an L2, the application can optimize user experiences (transaction fees/MEV collection and rebates, on-chain privacy, etc.) for its use case (e.g., trading). These optimizations can be implemented while still maintaining transaction records on the more secure L1.

-

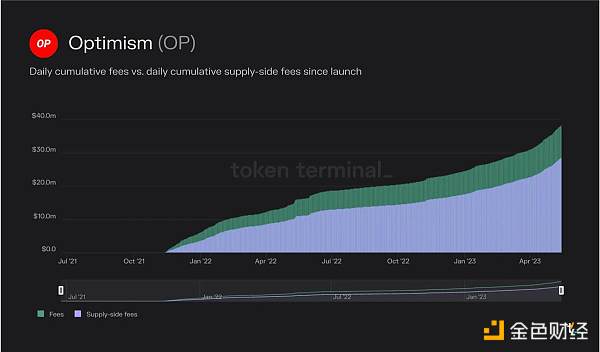

The economics of L2 blockchains are driven by two variables: fees charged by L2 and the cost of settling transactions to L1. The main business model of L2 blockchains is to generate revenue by reducing transaction fees paid by users. Profit margins are determined by the cost of settling transactions to L1. For example, users on Optimism have paid a total of $38.2 million in transaction fees since its launch. Of these fees, $28.5 million was used to pay gas fees for submitting transactions to Ethereum. Therefore, Optimism captured the difference, $9.7 million, as revenue. As competition intensifies, profit margins for L2 blockchains are expected to decrease. L2 blockchains that can optimize their gas expenditures on Ethereum through data compression and other techniques, further reducing the cost of L2, may gain market share in the future.

Since its launch on the network, users on Optimism have paid a total of $38.2 million in transaction fees. Of these fees, $28.5 million were used to pay for gas fees submitted to Ethereum.

Conclusion

Blockchain is redefining the infrastructure of economic activity by providing a decentralized, secure, and transparent transaction processing architecture. In rapidly evolving industries like cryptocurrency, we see these computational platforms innovating their economic models continuously. Despite the differences, investors can use the above framework to compare their economic performance, potential, and sustainability.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Why does Vitalik believe that zk-SNARK technology will be as important as blockchain in the next 10 years?

- Understanding SAFT and Web3 Token Financing from the Perspective of Three-Generation Token Models

- Relation Protocol announces its native token REL economic model

- With the rise of the APP Chains, what is its past life, present life and future?

- The ATOM 2.0 white paper is about to be released, can the value capture capability of Cosmos be improved?

- Technical Guide | Teach you how to build a commercial DAO without a bank

- LikeCoin wait 21 days to cancel the delegation? Talk about Cosmos's proof of bound equity BPoS