What can a blockchain mortgage do for the global recession?

There have been many discussions about the economic recession in the near future, and all the signs have gradually emerged: the securities market is faltering, the US economy is weak, the European banks are in a downward trend, Sino-US trade frictions continue, and the Fed cut interest rates for the first time since the last financial crisis. After another month, interest rate cuts have caused the interest rate in the repo market to soar.

Not long ago, the US Treasury announced a "housing reform plan", hoping to return the government-backed Fannie Mae and Freddie Mac to private hands. Fannie Mae and Freddie Mac are the two largest mortgage-backed companies and government-funded companies (gse) that were taken over by the government during the 2008 real estate crisis and have been operated by the government since then.

Today, our current economic environment has many similarities with the previous financial crisis, but there is also a significant difference. In the last crisis, a new technology emerged, which gave birth to new financial markets and economic rules. Now, the situation we face is: We are now living in a world of bitcoin and blockchain.

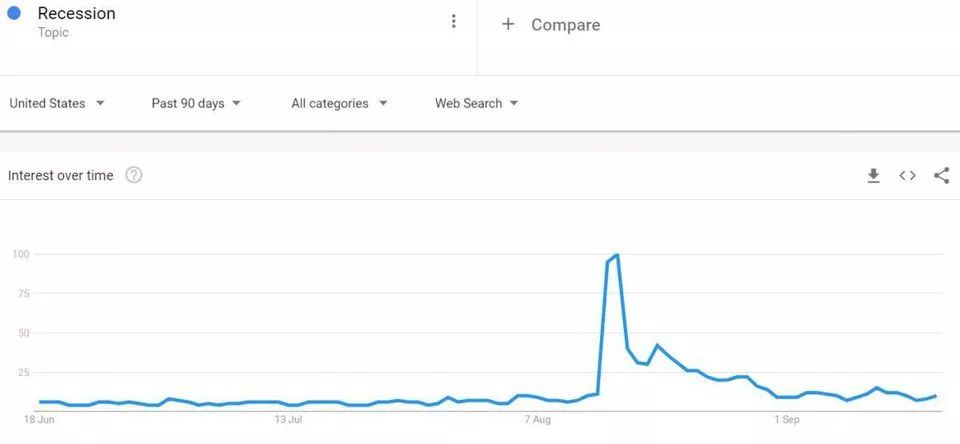

We live in a social media-driven society, and emotions seem to be transformed overnight. Even Google search shows that the search for the word “recession” will surge in August.

- DevCon's on-site connection was launched in November. What is the most anticipated feature of Dai mortgage?

- Multi-mortgage Dai will be officially launched on November 18th, what new features will be brought to the Maker agreement?

- Find the Fountain of Trust: Read the Principles, Types, Status and Development Direction of Prophecy

Google search trend

So, when dealing with opaque and inefficient mortgage issuance systems, do we choose to trust software or humans?

What are the benefits of using blockchain technology to issue digital mortgages or mortgage-backed securities?

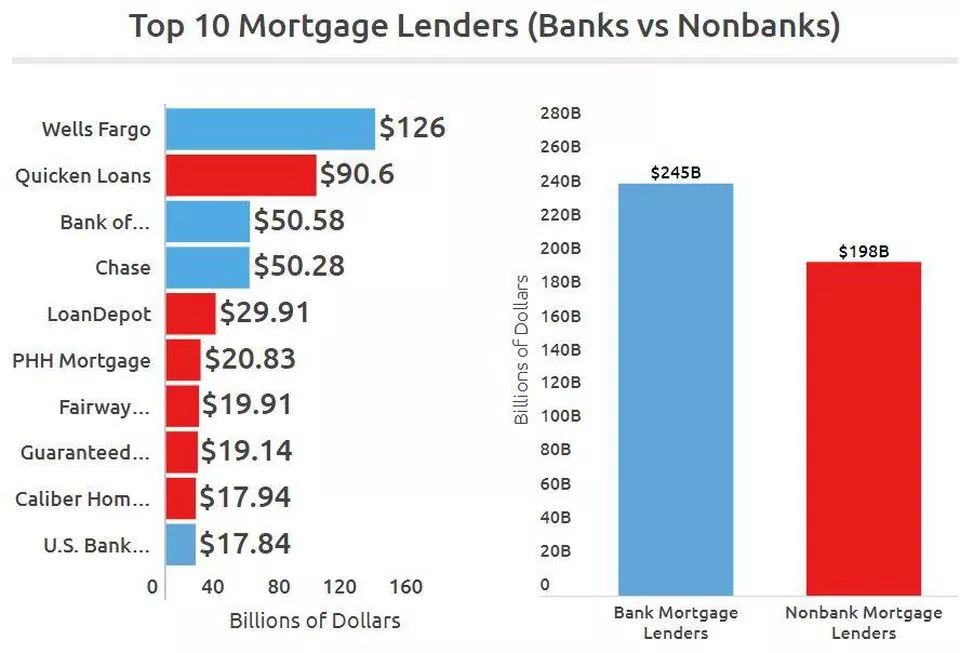

Bank and non-bank lending institutions

Bank and non-bank lending institutions

So, what are the current problems in the mortgage sector? First of all, this is a highly artificial and heavily paper-dependent thing, which usually takes 45 to 60 days. The average number of pages for mortgage application materials is approximately 500 pages and can be up to 2,000 pages. In addition, there are many intermediaries (brokers, appraisers, lawyers, underwriters, agents, and agencies) involved in this process. Each intermediary adds a total asset value to real estate transactions. 2% cost of the cost.

In such a large environment, new blockchains and smart contract systems can flourish. For example, we can make the trading process almost completely automated by smart contracts without the intervention of a lawyer. We already have platforms like OpenLaw and Clause that provide legally binding smart contracts and automate the entire process.

Another area that can be expanded is the 45 million Americans who do not have a credit score. For banks, this is an untapped market. The solution to this problem is to create a digital credit scoring system that calculates relevant ratings based on individual digital records and social signals. Using the blockchain as the underlying record storage technology will provide an immutable, credible record of the record. With the rise of digital identity platforms running on blockchains, it will help to verify the identity of applicants in real time.

The essence of distributed ledger technology (DLT) is to replicate copies of data on multiple chains based on set privacy conditions and data rules and personally identifiable information (PII) rules, and then all participation on the blockchain mortgage network Both parties can significantly reduce their common mortgage initiation risk and loan fraud risk.

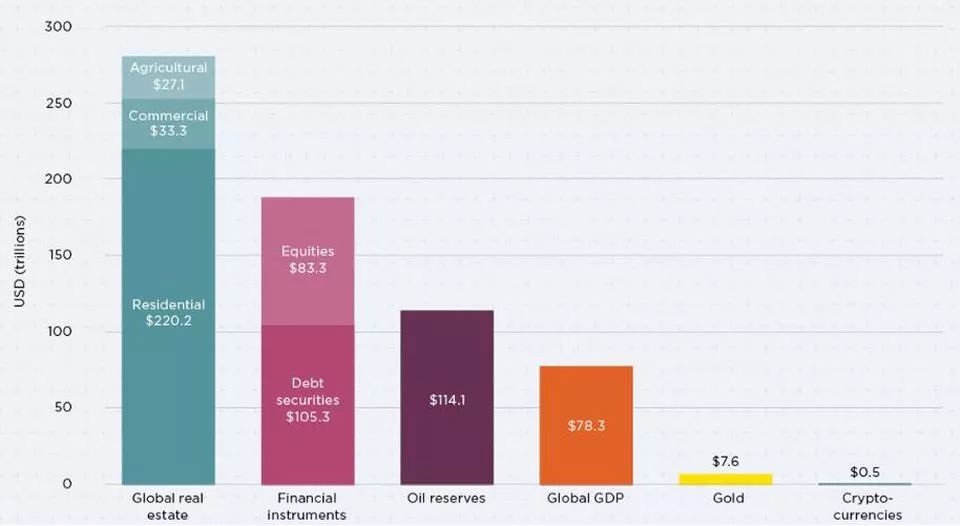

Real-world assets will be digitized. So far, we have seen a large number of financial assets, such as fiat currencies, stocks, bonds and stocks, being converted into their respective digital copies on the blockchain ledger. And we have seen a clear example of digital securities in the financial services arena, but the bigger opportunity is to digitize real estate. From this perspective, this is an opportunity for the digitization of real estate.

Global real estate market

When we mark our property on the blockchain, it increases the visibility and liquidity of the assets, which will be the first choice for the origin of digital mortgages.

Once we mark the real estate and digital mortgages that originate from the blockchain, the issue of mortgage-backed securities will seamlessly interface with the same ledger. One way to do this is for the lender to issue a security token to reduce the risk and earn some money. Another option is for the borrower to issue tokens to raise funds for the assets originally purchased.

The digital transformation brought by the blockchain and DLT will have an impact on the mortgage industry, but it may take some time to show up. We have seen that we are moving in this direction, but it will take years to wait until the heavyweights like the bank come in completely. But what is certain is that blockchain technology and smart contracts will save huge operating costs and open up new untapped markets.

Author: Biser Dimitrov

Translation: Jiang Yusheng

Source: Blockchain Outpost (Public Number)

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- ETF's annual developer conference Devcon four highlights

- What are the threats to Bitcoin?

- How can NuCypher bring privacy to Dapp by investing more than 10 million USD in more than 10 companies such as YC and Bitland?

- United Nations agencies set up cryptocurrency funds, Ethereum official donated 10,000 ETH for its support

- Telegram announces the Grams Wallet Terms of Service, and the encrypted wallet will be integrated into the messaging app.

- Lightning network giant ACINQ received $8 million in financing. Why did the 6-person team get favored by state-owned banks?

- In addition to speculating coins, we still have 10,000 ways to participate in the currency circle.