1/3 of the blockchain application is contracted by this trillion market

Text: Huang Xueyi

Production: Odaily Planet Daily (ID: o-daily)

"Baoding Hongan Packaging" is the supplier of Ruixing Coffee's "Little Blue Cup" packaging. However, in cooperation with large enterprises like Ruixing Coffee, the repayment period is long, and it takes more than half a year for the supplier to really get the money. This brings a lot of trouble to the operation of SMEs.

Earlier this year, Hongan Packaging entered the "Filuo Supply Chain Platform" based on the blockchain. Within an hour, the factoring company completed the risk control review and credit, and more than 1 million yuan was first credited to the company's account.

- Ethereum 2.0 is about to start the transition, these issues are worth paying attention to

- Ethereum will be upgraded this Saturday, and developers have agreed to delay the launch of the difficulty bomb

- Computing Power is King: Global Treasure Map

This enterprise is just one of the cases of blockchain transformation of supply chain finance.

In the "White Paper on Blockchain and Supply Chain Finance" released by the China Academy of Information and Communication Technology in October last year, of the 42 real-life financial blockchain cases, there were 16 supply chain finance cases, accounting for more than 1/3.

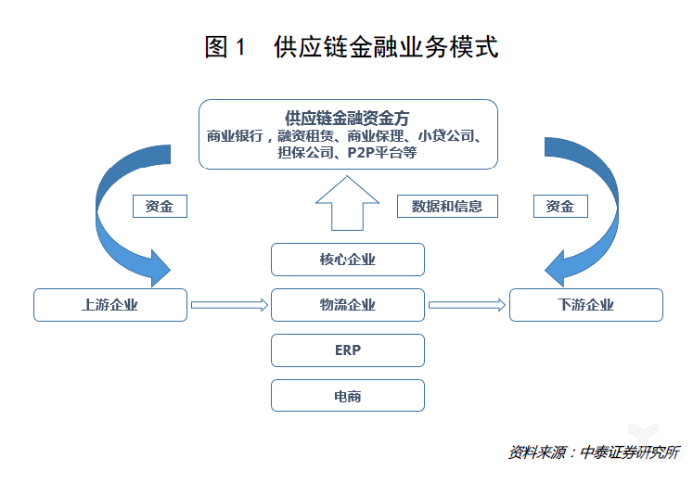

Blockchain mainly solves the "three dilemmas" of traditional supply chain finance-difficulty in SME loans, difficulty in risk control of financial institutions, and difficulty in supervision of relevant departments, thereby improving the penetration rate of supply chain finance in the B2B market (current penetration rate Less than 20%). Specifically, the blockchain makes it possible for the supply chain companies that originally had no data to communicate with each other to verify information, thereby reducing financing costs and improving the efficiency and market size of supply chain finance.

Because of this, blockchain + supply chain finance has been recognized by regulatory authorities.

In July this year, the CBRC issued documents to major banking and insurance institutions, encouraging the use of blockchain and other technologies to improve risk control and promote the supply chain financial services to the real economy.

In the trillion-dollar market of supply chain finance, blockchain is expected to land rapidly and commercialize, which will really help industrial innovation.

What is supply chain finance?

What is supply chain finance?

Most of the time we buy things and pay for them with one hand, but not between companies.

Large companies such as Foton Motors have more than 1,500 component suppliers and more than 2,000 dealers. This makes Foton Motors (the core company) have a lot of choices, and the supply / dealers are in a dependent (weak) position, which has led to the prevalence of credit sales by core companies.

For example, supplier A told Foton Motors that you and I signed a 10 million purchase contract, and I will give you a few months' billing period, and I will give you the parts to produce the car, sell it, and wait for the payment to be paid in full. amount.

As a result, the order was received, but there were disadvantages. For example, suppliers will have a tight cash flow due to a large number of accounts receivable. Once the funding chain breaks, they will need to use debt to survive and even face bankruptcy. At the same time, core companies will also face pressure to cash out payments in advance.

In order to solve this problem, the supply chain finance that promotes the financing of finance has emerged as the times require.

In simple terms, this business will provide loans to these supply chain companies based on accounts receivable / prepaid accounts and inventory. The loan amount (or financing amount) is usually 70% -80% of the accounts receivable itself. 30% -50% of the value.

As of 2018, the size of the domestic supply chain financial market reached 2 trillion yuan.

But there are still many hidden concerns behind this data. For example, the penetration rate of the supply chain financial market in the B2B market is less than 20%; in 2018, domestic receivables financing needs exceeded 13 trillion yuan, but the actual loaned funds were only 1 trillion yuan, and mainly by large banks Tier 1 suppliers serving very large core enterprises, and small and micro enterprises in the long tail of the supply chain have a financing gap of nearly 12 trillion yuan.

Investigating the reasons, there are three existing problems in supply chain finance: difficulty in loans to SMEs, difficulty in risk control of financial institutions, and difficulty in supervision of relevant departments. One of the concentrated manifestations is the constant supply chain financial scam.

Frequent supply chain financial fraud

Frequent supply chain financial fraud

On July 5 this year, the news that Luo Jing, the actual controller of Chengxing International Holdings (02662.HK), was sentenced to prison, unveiled the "Chengxing Department" tens of billions of dollars in supply chain finance "scam".

According to reports, Chengxing is an upstream supplier to large enterprises such as Suning, JD.com, and China Mobile. Also, due to the credit of these companies, it has exerted greater cash flow pressure on Chengxing, and Chengxing then packaged the receivables of the above companies into related The products were issued on various financial platforms and raised 10 billion yuan.

However, after the incident, JD.com announced that Chengxing was suspected of forging and JD.com's business contract fraud; Suning also denied the authenticity of accounts receivable.

Which part of the fraud has yet to be investigated, but this has sounded the alarm for the industry. How to improve the authenticity of the three streams of supply chain capital flow, logistics, and business flow (the circulation of commodity value) has become a demand of financial institutions.

Multi-party verification seems to be a "positive solution". However, there is still no unified business information system among enterprises. The supply chain management system SCM, enterprise resource management system ERP, and financial system used by various entities are different, and it is difficult to interface.

In addition, supply chain finance also exists. Core enterprise credit can only be passed to the first-tier supplier, while the second-tier supplier behind the first-tier supplier is difficult to obtain high-quality loans because there are no accounts receivable bills issued by the core enterprise. In the end, corporate loans are difficult. The root cause of this problem is that the current liquidity of the bills is poor and inseparable, and can only be transferred between core enterprises and first-tier suppliers.

It can be seen that unless business innovation and technological innovation are carried out, the “trilemma” of supply chain finance will be difficult to resolve.

How does the blockchain solve it?

How does the blockchain solve it?

Maybe someone asks, can't the above problems be solved by Internet technology alone?

It's hard. There is at least one barrier here.

The inter-enterprise system built by traditional technology cannot guarantee that the data will not be tampered with, while meeting the rigid needs of enterprises to protect core data privacy. This requires data storage to have strong anti-interception and anti-crack capabilities.

The blockchain technology integrated with cryptography can just solve these problems. The most basic "configuration" is that the supply chain system builds a blockchain + supply chain finance alliance. The alliance participants include core companies, suppliers, financial institutions, and if necessary, can also join the supply chain platform founders and relevant supervision. mechanism.

With this set of infrastructure, as in the above example, after receiving a loan application from Chengxing, the financial institution immediately applied to the relevant parties on the chain to verify the authenticity of the contract, and whether the contract has been verified multiple times (multiple loans). Then, Jingdong, Suning and other companies honestly reported that financial institutions would not fall into the trap.

At the same time, with the help of the blockchain, the payables of core enterprises can have corresponding vouchers and be split by the first-tier suppliers and delivered to the second-, third-, …- level suppliers on the same chain to help them with financing. And core companies can also use this to understand whether the entire chain is operating normally, relieve emergency payment pressure, and improve the security of the entire supply chain finance process.

In addition, blockchain-based supply chain financial solutions can also improve settlement efficiency. The settlement between various links in the traditional supply chain cannot be reconciled in real time and completed automatically. Smart contracts in the blockchain can automatically clear and settle after triggering certain conditions, reducing manual operations. Financial institutions such as banks can reduce costs and improve efficiency in terms of trade data acquisition and verification.

IResearch predicts that by 2023, the blockchain can bring about an increase of approximately 3.6 trillion yuan in market size to the supply chain financial market, allowing the overall market size of the supply chain finance to exceed 6 trillion yuan (penetration rate increased to 48%). ; Reduce the overall operating cost of the supply chain financial market by 0.48%, corresponding to a profit increase of approximately 29.7 billion yuan.

Excerpted from "Blockchain and Supply Chain Finance White Paper" (on October 31 last year, the China Academy of Information and Communications Technology, Tencent Financial Technology, Shenzhen Unicom led the three parties, and organized a number of units to jointly release white paper")

Who are the big players in the vertical?

Who are the big players in the vertical?

It is precisely to see this vast space. In the past two years, more and more industrial supply chains have chosen the blockchain + supply chain financial platform.

According to iResearch, there are four main types of participants:

- Blockchain technology (or solution) service providers, such as QuChain Technology (which has the Feilo supply chain platform mentioned above) and Wanxiang Blockchain;

- (Financial) technology companies, such as Ant Financial, Tencent;

- Financial institutions, such as the four major state-owned banks;

- Core / warehouse companies, such as Suning, Foxconn, Foton Motor, etc.

From the perspective of public data, blockchain + supply chain finance has achieved good results.

From the perspective of public data, blockchain + supply chain finance has achieved good results.

For example, the China Enterprise Cloud Chain, co-sponsored by ICBC, Postal Savings Bank, and 11 central enterprises, has covered 48,000 enterprises since its establishment in 2017. The amount of rights on the chain has reached 100 billion yuan and factoring financing is 57 billion yuan. The accumulated transaction amounted to 300 billion yuan.

As of the end of 2018, Tencent Micro-enterprise, which has been operating for less than one year, has linked to 12 cooperative banks, served 71 core companies and nearly 3,000 suppliers, covering real estate, energy, automotive, pharmaceutical and other fields, covering first- and second-tier suppliers. The financing amount is nearly 30 billion yuan, which can reduce interest rates by 2 to 8 points compared with traditional bank loans.

In December 2018, the IEEE, Ant Financial Services, and other companies co-sponsored the compilation of "Blockchain Standards in Supply Chain Finance." This is IEEE's first financial industry blockchain standard, which defines a blockchain-based general framework for supply chain finance, a role model, typical business processes, technical requirements, and security requirements.

Of course, blockchain is not a panacea.

In the visible 3 to 5 years, it is still difficult to use the blockchain to help physical (inventory) financing. A major problem in inventory financing is the inability to effectively monitor the movement of goods into and out of the warehouse. Among the current possible solutions, in addition to the blockchain, it is also necessary to cooperate with IoT technologies such as RFID, AGV, and video analysis to ensure the control of cargo rights and improve the success rate of loans.

Secondly, the cost of the transformation and construction of the existing platform by the blockchain business also requires a period of adaptation. According to iResearch statistics, if an ordinary enterprise wants to join a blockchain supply chain financial platform initiated by a blockchain technology service provider or fintech company, it usually needs to pay 500,000 + annual service fee.

The difficulty of landing is not only a technical and commercial issue, but it also needs to be accompanied by regulations. IResearch believes that relevant regulatory agencies need to proceed to standardize technical and business supervision from the perspective of blockchain technology development trends, data protection, financial risks, etc .; strengthen the review and audit of smart contracts; carry out relevant legal research and legislative work to achieve The business of blockchain + supply chain finance can be checked and can be followed.

References

"Analysis of Land Supply Strategy and Development Trend of Blockchain Supply Chain Finance", iResearch, August 2019

"Distributed Capital Research Report: Blockchain + Supply Chain Finance", June 2018

"Blockchain +" Made in China ": How Blockchain Improves the Vitality and Efficiency of Supply Chain Finance", Blockchain Base Camp

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Popular Science | Crypto War, Blockchain Technology

- Is a cryptocurrency scam a new bottle of old wine? Tyler Winklevoss teaches you how to see through at a glance

- Why did Ethereum delay the "glacial period" three times? The new hard fork is coming again!

- QKL123 Blockchain List | Domestic media enthusiasm declines, some mining machines lose money (201911)

- Read Monero's Fair Mining Algorithm RandomX

- Seven years after its birth, the number of r / Bitcoin subscribers on Reddit exceeds 1.2 million

- Getting Started with Blockchain | What is DAO?