Analysis | What is the relationship between the development of DeFi and the supply and demand of ETH?

Decentralized finance (DeFi) has shown rapid growth in a wide range of digital currency ecosystems, representing one of the most important use cases for the Ethereum network.

In the past year, several well-known DeFi platforms have been launched and have generated a lot of market interest. Although each DeFi platform has its own characteristics, and in many cases has different business models and provides different financial services, most platforms have one thing in common, even if the native currency ETH of the Ethereum network is used as these platforms. Collateral on .

As the demand for DeFi services grows, so does the ETH demand for these DeFi platforms . In view of the increasing demand for ETH from these DeFi, we attempt to quantify the supply and demand dynamics of ETH in the next few years. Primarily, we will attempt to predict the relationship between DeFi and ETH supply and demand dynamics based on a conservative scenario.

In the past few months, as more funds have flowed into the Ethereum sector, ETH prices have ushered in a small increase since they bottomed out in 2018. In recent weeks, in the turmoil of the market, with the decline in the price of many altcoins, the price of ETH has also dropped.

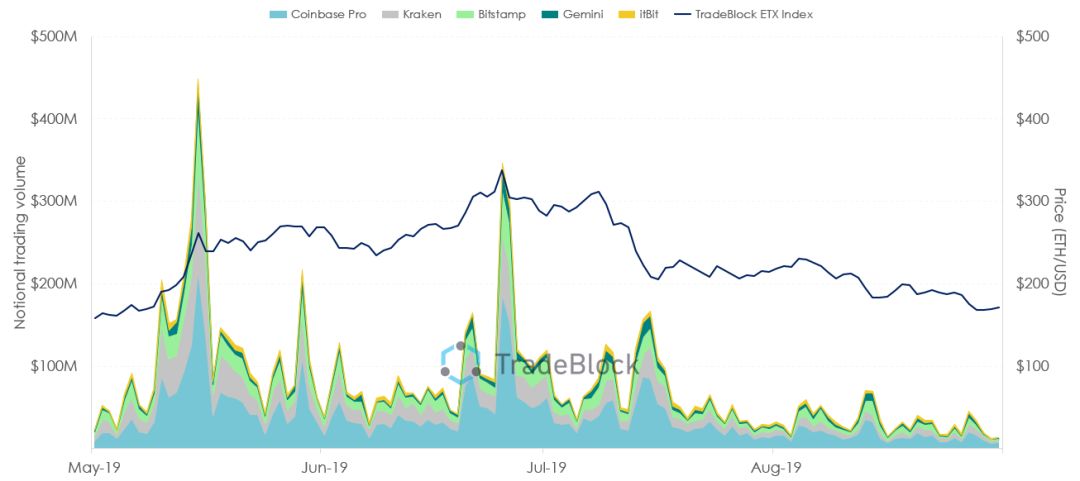

In the chart below, we plot the ETH price trend (black line) over the past few months and the ETH volume changes in several major US exchanges:

Figure 1: Trends in ETH prices and their trading volume on several US exchanges, source: TradeBlock Professional

DeFi service background information

The DeFi platform provides financial services similar to traditional centralized businesses, but the DeFi platform exists in an ecosystem that does not require trust, so the reliance on intermediaries is greatly reduced . The DeFi platform incorporates smart contract functionality into trading activities that typically require users to pledge digital assets to ensure that users are well engaged. Similar to traditional financial companies, the DeFi platform provides debt-backed products (such as loans/bonds/derivatives/mortgage, etc.); however, these products are secured by digital currencies (rather than other assets) . Since the decentralized platform does not rely on third-party intermediaries to ensure trust between the parties, these DeFi platforms typically rely on collateral (digital currency) stored in smart contracts to ensure that users will be in compliance with the terms of the contract. Payments.

While many decentralized platforms offer different types of mortgages, most of the collateral locked in smart contracts is ETH .

DeFi platform's growing demand for ETH

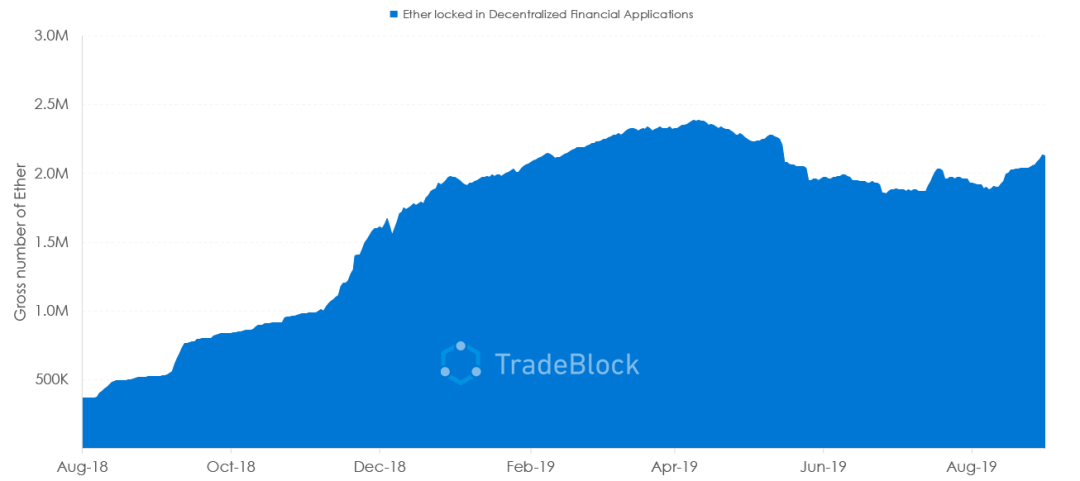

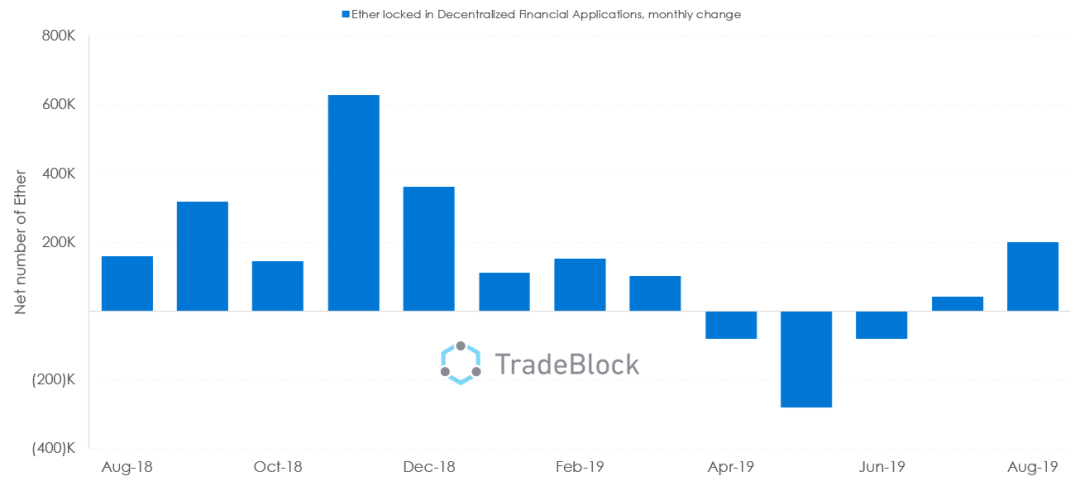

Since the inception of many DeFi platforms, the demand for ETH as a collateral has increased significantly. In the image below, we plotted the trend of the number of ETHs locked in the DeFi platform as collateral over the past year. The chart below shows that the number of ETHs mortgaged on all DeFi platforms fell to the highest level earlier this year and declined in the second quarter of this year, but has rebounded in the third quarter.Figure 2: ETH aggregate trend graph for DeFi platform mortgage, data source: DeFi PluseCompared to the same period last year, the new ETH collateral in the DeFi platform has a monthly growth rate of approximately 17% . The chart below shows the change in the number of ETH collaterals that are net inflows into the DeFi platform (ie, the amount of ETH added to the DeFi minus the net amount of the reduction).Figure 3: ETH collateral for monthly net inflows from the DeFi platform, data source: DeFi Pluse In the past year, the average monthly net inflow of ETH collateral to the DeFi platform exceeded 125,000 ETH , equivalent to an average daily net inflow ofETHsexceeding 4,000 ETH . As can be seen from the above chart, the recent increase in the monthly inflow of ETH collateral has slowed down. The daily average ETH collateral net inflow in July 2019 was 1,300 ETH .

Expected daily demand for ETH collateral in the future

In order to estimate the demand for future ETH collateral, we need to make some assumptions. We will adopt a conservative approach to analyze a possible scenario, assuming that as the DeFi platform and market mature, the growth rate of ETH collateral demand will decline . Based on this assumption, we expect a monthly average growth rate of 5% in the future compared to the 17% average monthly growth rate of ETH collateral in the past year. In other words, considering the accelerated growth of new ETH collateral on these DeFi platforms over the past year, and signs of a slowdown in recent growth, assume that the ETH collateral will be available as the market penetration of the DeFi platform approaches saturation point. The growth rate will probably all slow down .

In addition, with the advent of multi-collateral guarantee contracts, some DeFi platforms are expected to accept collateral other than ETH (such as the multi-mortgage Dai implemented by MakerDAO).These collaterals from other digital currencies will likely reduce ETH's demand as collateral .

In anticipation of future demand, we will forecast based on the average daily demand of 1,300 ETH in July 2019. Assuming an average monthly growth rate of ETH collateral in the DeFi platform is around 5% , then in the next year, this means that the average daily demand for ETH collateral will be around 3,000 ETH .

Estimated future ETH's daily increase

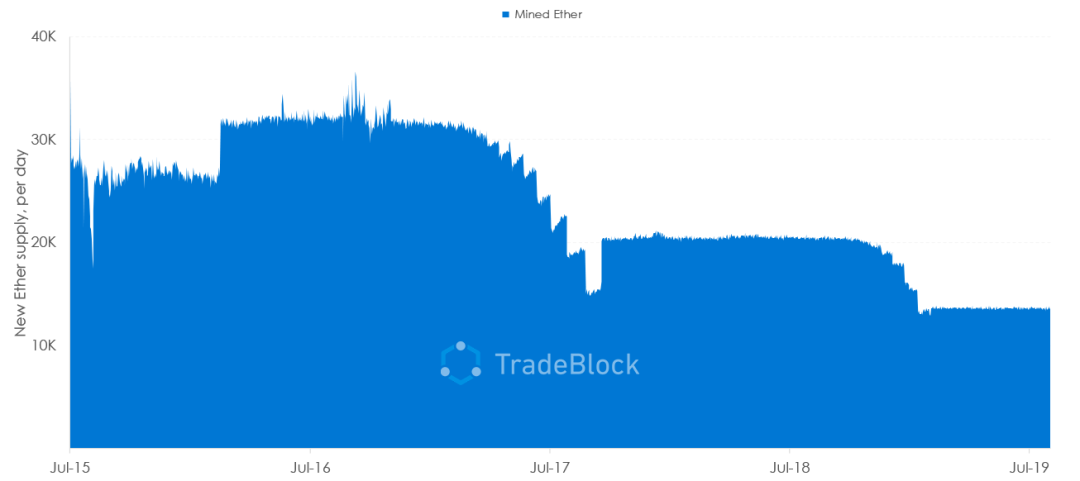

The current annual inflation rate of ETH (ie, the rate of increase) is about 4.65% . The hard fork upgrade of Constantinople earlier this year reduced the ETH inflation rate in the Ethereum network, and the reward for each block was reduced from 3 ETH to 2 ETH. In the image below, we plotted the daily supply trends for ETH since 2015.Figure 4: ETH day new trend chart since 2015, data source: TradeBlock Professional The Ethereum network is expected to open another network upgrade in early 2020 – Serenity (Ethernet 2.0), when we are expected to witness a reduction in the ETH issuance rate.Ethereum developers expect that after the successful implementation of Serenity (approximately 2021), the annual growth rate of ETH will fall to between 0.25% and 0.2% . There is no fixed plan for the issuance and supply of ETH, and with the transition of the Ethereum network to the PoS consensus, the future ETH issuance rate is not certain . In our scenario, we assume that the annual increase in ETH will be reduced to a conservative estimate of 1% from February 2020 . However, it should be noted that the delay in the development of the Serenity roadmap may result in considerable changes in the rate of this estimate.

DeFi's ETH demand will probably exceed the ETH's increase

Assuming that ETH's annual growth rate drops to 1% from February 2020, this means that by November 2020, the daily added ETH supply will be around 3,000 ETH . Considering the above we mentioned that in the next year, the average daily demand for ETH collateral in the DeFi platform will also be around 3,000 ETH , which means the daily demand for ETH as collateral in the DeFi platform. Will be close to the daily increase in ETH . In other words, if the demand for ETH collateral in the DeFi platform is higher, or the annual increase rate of ETH is more reduced, then by November 2020, the demand for ETH collateral on the DeFi platform will exceed the ETH day. The amount of increase.

However, it is also important to note that if the price of ETH rises sharply due to speculation or other reasons, this will reduce the number of ETHs that need to be locked on the DeFi platform (ie, the number of ETH collaterals will decrease).

Therefore, if ETH prices rise sharply and demand for DeFi services grows faster than ETH prices, the daily demand for ETH collateral used in DeFi platforms will fall.

In fact, the daily demand for ETH collateral in DeFi platforms typically declines as prices rise sharply, and the demand for ETH collateral increases as prices fall, as shown in the chart below.

This is because ETH collateral for each DeFi platform will increase in the case of a sharp drop in prices; when the price increases, the number of ETH collateral will decrease, and market participants may remove some ETH collateral from the DeFi platform. . See below:

Figure 5: Correlation between ETH daily demand and ETH price in DeFi platform

Conclusion

We hope that this report will shed light on how DeFi services can have a tangible impact on ETH demand. Our conservative forecasts indicate that by November 2020, the demand for ETH for DeFi services will likely exceed the new ETH. In addition, there may be other decentralized applications (dApps) that increase the demand for ETH collateral, such as dApps in games or healthcare. However, it is also important to note that if the supply of ETH does not decrease significantly in the future as we expected, this will likely result in a supply of ETH that greatly exceeds the demand for DeFi or other dApps.

Source: Unitimes

Author | TradeBlock

Edit | Summer

We will continue to update Blocking; if you have any questions or suggestions, please contact us!