Binance Research Emerging Stablecoins and an Overview of Market Competition

Binance Research on Stablecoins and Market CompetitionAuthor: JieXuanChua, Source: BinanceResearch; Translation: Yvonne, MarsBit

1. Key Points

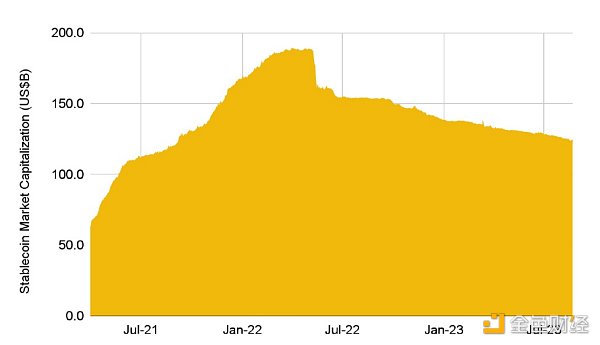

Stablecoins play a critical role in the crypto ecosystem, widely used in trading, lending, asset management, and many other functions. The market capitalization of stablecoins is $124.4 billion, accounting for 8.5% of the total cryptocurrency market value, which demonstrates their importance in this field.

Although centralized, fiat-backed stablecoins dominate this field and may continue to do so in the foreseeable future, competition has intensified in recent months with the entry of new participants.

- LianGuai Morning News | SEC decides to postpone the registration of 7 Bitcoin ETFs including BlackRock

- Binance Research Report Emergence of New Types of Stablecoins, Overview of Market Competition Pattern

- Review of the Cryptocurrency Market Summer Trends Mixed Bullish and Bearish News, Doubts about the Sustainability of the Rise.

Debt collateralized position (CDP) stablecoins, stablecoins backed by liquidity provider tokens (LST), and other centralized stablecoins have emerged as interest in stablecoins continues to rise, with each project trying to gain market share.

In this report, we study the mechanisms and adoption of some recently launched stablecoins, including Aave’s GHO, Curve’s crvUSD, Lybra’s eUSD, Raft’s R, LianGuaiyLianGuail’s PYUSD, and First Digital’s FDUSD.

Considering the market liquidity, we also list some recent developments and observations, including MakerDAO increasing the DAI savings rate, integrating real-world assets, and more projects adopting LST.

2. Market Landscape

Stablecoins play a critical role in the crypto ecosystem, widely used in trading, lending, asset management, and many other functions. By being pegged to external assets, most commonly the US dollar, stablecoins have lower volatility than other cryptocurrencies, making them a popular medium of exchange and unit of account.

The importance of stablecoins is undeniable, especially considering that they are the cornerstone of many decentralized finance (DeFi) protocols, serving as a source of liquidity in transactions and enabling stablecoin loans in the lending market.

Although the stablecoin market has significantly contracted since the peak before the TerraUSD crash in May 2022, stablecoins continue to play a foundational role in the crypto ecosystem. The total market capitalization of stablecoins is currently $124.4 billion, accounting for approximately 8.5% of the total cryptocurrency market value, which demonstrates the importance of stablecoins.

Figure 1: The current market capitalization of stablecoins is $124.4 billion

Data Source: DeFi Llama, as of August 22, 2023

2.1 Centralized Stablecoins Dominate

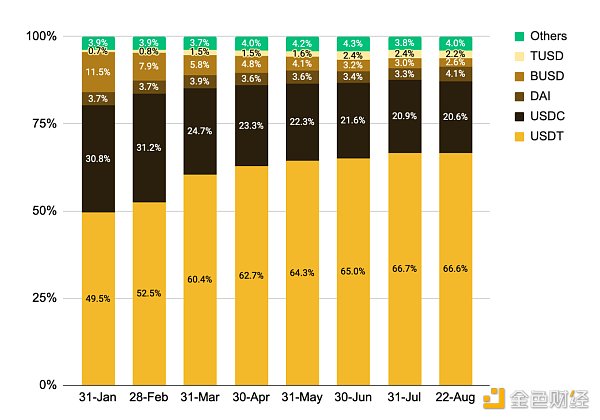

Top centralized stablecoins such as USDT, USDC, BUSD, and TUSD account for approximately 92% of the stablecoin market share. It is worth noting that Tether’s USDT has been steadily growing and has become the undisputed market leader with over 66% of the market share. Despite experiencing a slight decoupling event in June 2023 when USDT experienced a 0.4% mild decoupling, it once accounted for over 70% of the Curve 3pool.

The dominance of USDT comes at the expense of other stablecoins, whose market share has been steadily declining. USDC failed to regain traction after the decoupling event in March 2023, and BUSD’s market share has been steadily declining since its issuance was halted in February.

Figure 2: Centralized stablecoins account for approximately 92% of the market share

Data source: DeFi Llama, as of August 22, 2023

3. Emerging Stablecoins

While centralized stablecoins dominate this space and may continue to do so in the foreseeable future, competition has intensified in recent months with the entry of new participants into the market. In particular, we have seen the emergence of new collateralized debt position (CDP) stablecoins, stablecoins backed by liquidity collateral tokens (LST), and centralized stablecoins launched by a well-known Web2 company. The launch of these projects comes at a time when interest in stablecoins is steadily rising and projects are vying to establish a foothold in this field.

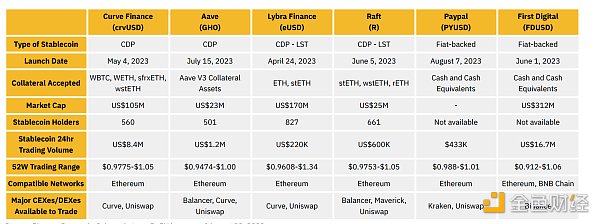

Figure 3: Summary of stablecoins launched in recent months

Data source: Binance Research, Coinmarketcap, DeFi Llama, as of August 23, 2023

3.1 CDP Stablecoins

CDP stablecoins refer to loan protocols based on smart contracts, where users collateralize assets (such as ETH) and receive loans denominated in stablecoins as rewards. This was first introduced by the MakerDAO team and is how DAI stablecoin operates. Such a mechanism allows users to unlock their liquidity without selling their crypto assets. Once the stablecoin loan is repaid, the collateral is released back to the user.

crvUSD launched by Curve

A few months ago, in May of this year, Curve Finance introduced the stablecoin crvUSD. As one of the leading decentralized exchanges and the seventh-largest DeFi protocol, Curve’s entry into the stablecoin market brought another heavyweight to the competitive landscape.

crvUSD is pegged to the US dollar and is minted by depositing collateral and opening loans on Curve.

The simplified process of obtaining and repaying crvUSD loans includes the following steps:

1. Provide collateral;

2. Borrow crvUSD;

3. Repay crvUSD and accrued interest.

One unique aspect of crvUSD is its liquidation mechanism called the Loan Liquidation AMM Algorithm (LLAMMA). In a typical liquidation process, a borrower’s collateral is liquidated immediately when it breaches a threshold, whereas LLAMMA employs a “soft liquidation” approach. During this process, a borrower’s collateral is dispersed across a range of liquidation prices, allowing liquidation to occur continuously as the collateral value decreases, rather than instantaneously.

In addition, crvUSD utilizes a smart contract called “Peg Keepers” to create and absorb debt, with the aim of enabling stablecoins to trade near their peg. When crvUSD trades above $1, peg holders can mint crvUSD and deposit it into the stablecoin swap pool. If crvUSD trades below $1, it will be withdrawn from the stablecoin swap pool and destroyed.

Adoption and Activity

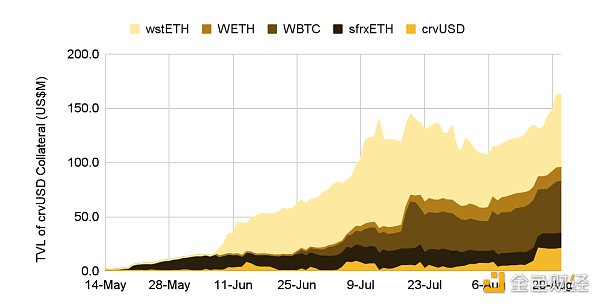

With the support of new collateral types, the adoption rate of crvUSD has grown exponentially in June. On June 8, wstETH was added as collateral; WBTC was added on June 18; and WETH was added on June 20. Currently, wstETH and WBTC have the largest shares in the collateral, accounting for 44% and 32% respectively.

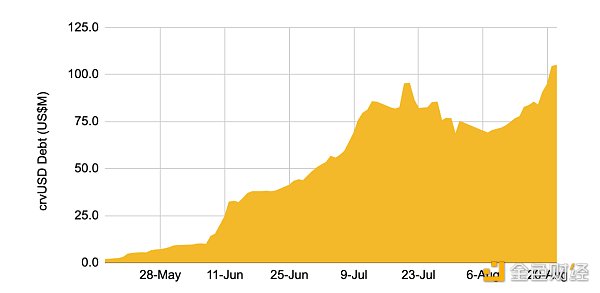

By the end of July, the activity volume decreased possibly due to the reversion vulnerability, but after that, metrics such as crvUSD debt and TVL recovered and reached new highs of $104.8 million and $162.4 million respectively.

Figure 4: Continuous increase in crvUSD debt

Source: Dune Analytics (@Marcov), as of August 23, 2023

Source: Dune Analytics (@Marcov), as of August 23, 2023

Figure 5: TVL of crvUSD collateral also reaches a new high

Source: Dune Analytics (@Marcov), as of August 23, 2023

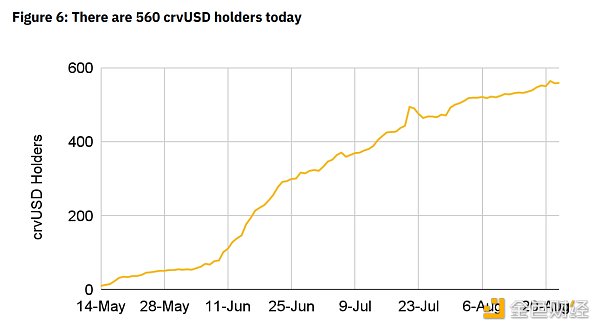

As debt and TVL grow, the number of crvUSD holders has also increased over time, with currently 560 crvUSD holders. This means that the average crvUSD debt per holder is approximately $187,000. Considering the relatively small holder base compared to the overall debt, this indicates that crvUSD is mainly used by larger participants or advanced DeFi players.

Figure 6: Currently, there are 560 crvUSD holders

Source: Dune Analytics (@Marcov), as of August 23, 2023

Outlook and Risks

crvUSD differentiates itself from other stablecoins in the market through its unique LLAMMA model, which can attract users seeking a smoother liquidation process. From the protocol’s perspective, crvUSD adds to Curve’s product suite and may have a positive flywheel effect on protocol activity. Specifically, the mechanism of LLAMMA requires constant rebalancing of collateral, which can attract more liquidity providers, increase trading volume in the Curve pool, and generate fees for the protocol and veCRV (voting escrowed CRV) holders.

On the other hand, holders of crvUSD debt should be aware that once their positions enter a soft liquidation mode, they cannot withdraw or increase collateral. Holders can only repay the loan with crvUSD or liquidate it themselves. Additionally, there is still a risk of instant liquidation and potential significant losses if the price of collateral sharply declines within a short period of time in the LLAMMA model (although greatly reduced).

GHO Launched by Aave

As the largest lending protocol with a total locked value of $4.5 billion (“TVL”), Aave’s entry into the stablecoin field is noteworthy. GHO is a decentralized stablecoin backed by overcollateralization. Borrowers and suppliers can use the assets they provide to Aave V3 as collateral to mint GHO.

The simplified process for obtaining and repaying GHO loans includes the following steps:

1. Provide collateral;

2. Borrow GHO;

3. Repay GHO and accumulated interest;

4. The repaid interest will be redirected to the DAO, contributing to the DAO’s funds.

Aave DAO manages GHO by setting the allowed supply, determining interest rates, mining limits, and approving “facilitators.” “Facilitators” are entities that can burn or mint GHO under predetermined conditions set by the DAO.

One unique aspect of GHO is that the collateral deposited in the Aave V3 protocol remains productive, continuously generating yield. This helps lower the borrowing costs for GHO loan users.

Adoption and Activity

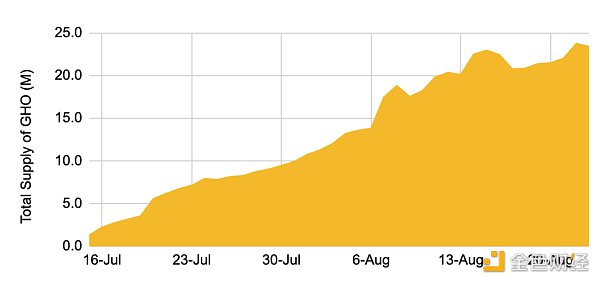

GHO’s adoption has been steadily growing. Just over a month after its launch, the circulating supply of GHO has exceeded 23.4 million. This makes GHO the 34th largest stablecoin based on circulating supply.

Figure 7: Total Supply of GHO at 23.4 million

Data Source: Dune Analytics (@aave_comLianGuainies), as of August 23, 2023

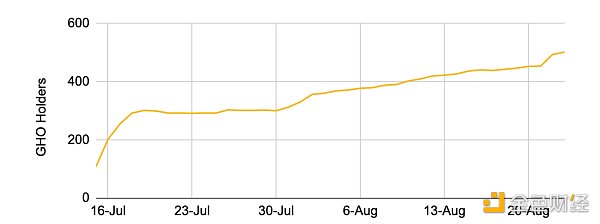

Currently, there are 501 GHO holders. Considering there are over 86,000 unique users on Aave V3, this implies a user penetration rate slightly below 6%. This indicates significant growth potential even when targeting the existing user base.

Figure 8: 501 GHO Holders

Data Source: Dune Analytics (@aave_comLianGuainies), as of August 23, 2023

Outlook and Risks

Overall, the launch of GHO has received extensive community support and is the next strategic step for a top-tier lending protocol. Aave DAO benefits from the additional revenue stream created by GHO; stkAAVE holders can enjoy a discount on GHO borrowing rates, and Aave can further expand its influence by expanding its ecosystem.

However, considering the competitive pressure in the stablecoin field, scaling up and disrupting the existing market dynamics are undoubtedly challenging. What may work in favor of GHO is its existing network effects, user base, and brand value. In particular, the market capitalization of GHO is only a small fraction of Aave’s TVL ($23 million vs. $4.5 billion), which represents growth potential considering the untapped user base.

It is worth noting that currently, GHO rates are determined by governance rather than market-driven mechanisms, which are more neutral and consider organic demand and supply. The borrowing cost is currently fixed at 1.51%, lower than other stablecoins on Aave, with borrowing costs as high as 3.50%. According to Stani Kulechov, CEO of Aave, the reason for the low interest rate is to encourage “borrowers to convert to Aave native assets for growth and utility at a lower cost and to encourage liquidity.”

Since its launch a month ago, the trading price of GHO has mostly been lower than the pegged exchange rate. It has proposed a “GHO Stability Module” that allows users to convert between GHO and stablecoins accepted by governance at a predetermined rate. If implemented, this would provide some guarantee for GHO holders and allow market forces to intervene in case of significant deviations from the pegged mechanism.

3.2 Stablecoins based on LST

The successful transition of Ethereum to Proof of Stake (PoS) and the introduction of staked ETH withdrawals have facilitated the rapid growth of liquidity-staking tokens (LSTs) such as stETH, rETH, WBETH, etc. In addition to the growing interest in LST and LSTfi, we have also witnessed the emergence of stablecoins supported by LST.

LST-backed stablecoins are overcollateralized with liquid staking tokens, allowing holders to earn intrinsic returns while preserving the key attributes of stablecoins.

Please note that the following LST-backed stablecoins also adopt the CDP model, but we choose to highlight the emergence of LST-backed stablecoins in a separate section of this report.

eUSD launched by Lybra

Lybra is a DeFi protocol that facilitates the minting of its interest-bearing stablecoin eUSD. Users can mint eUSD by depositing ETH or stETH as collateral. The protocol plans to support more LSTs in the future.

eUSD is pegged to the US dollar, and its uniqueness lies in its interest-bearing nature. eUSD holders can expect to earn approximately 7-8% (3) annual percentage yield (APY). This provides an opportunity for investors seeking stable income streams while maintaining exposure to potential crypto collateral.

The simplified process of obtaining and repaying eUSD loans includes the following steps:

1. Deposit ETH or stETH as collateral;

2. Mint or borrow eUSD against collateral;

3. Hold eUSD to earn interest or use it in other DeFi protocols;

4. Repay eUSD debt at any time as long as the collateralization ratio is above 150%.

So, how does eUSD generate returns for holders by simply holding it? This is achieved through the collateralization of LST. When users mint eUSD, Lybra converts the underlying LST’s staking rewards back into eUSD and proportionally distributes them to eUSD holders. Specifically, 98.5% of the staking rewards generated by the LST collateral are converted to eUSD and distributed to eUSD holders in proportion. The remaining 1.5% flows to holders of custodied LBR (esLBR).

The stability of eUSD is supported by the following factors:

Overcollateralization: Each eUSD is backed by at least $1.5 worth of stETH as collateral.

Liquidation mechanism: If a user’s collateralization ratio falls below the safe collateralization ratio, any user can voluntarily become a liquidator and purchase the liquidated portion of the staked ETH collateral.

Arbitrage opportunities: Users can profit from deviations in eUSD price from its peg and help restore the eUSD price to its expected value.

Adoption and Activity

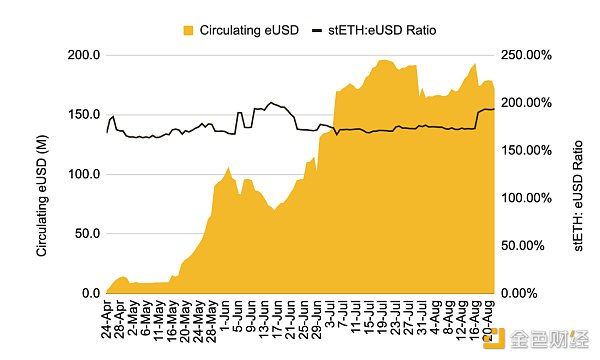

In the initial stages of launch, particularly in May and June, the circulating supply of eUSD experienced significant growth. This could be attributed to early adopters’ contributions and increased interest in LSTfi during that period. Since early July, the current circulating supply has been fluctuating within a range, with 170 million eUSD currently in circulation.

The collateralization ratio represented by the stETH to eUSD ratio has also remained relatively healthy at around 190%. In other words, each eUSD is overcollateralized and backed by approximately $1.9 worth of stETH.

Figure 9: 170 million eUSD in circulation

Data source: Dune Analytics (@defmochi), as of August 23, 2023

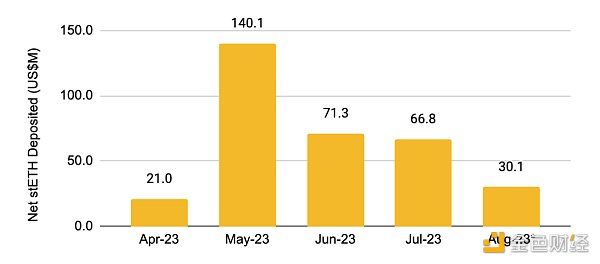

The protocol saw a peak in monthly net deposits in May 2023, with $140.1 million worth of stETH being deposited as eUSD collateral, setting a new monthly high. Since then, monthly net deposits have slowed down, averaging over $70 million in June and July.

Figure 10: Monthly net deposits peaked in May 2023

Data source: Dune Analytics (@defmochi), as of August 23, 2023. *Note: August data is not for the full month

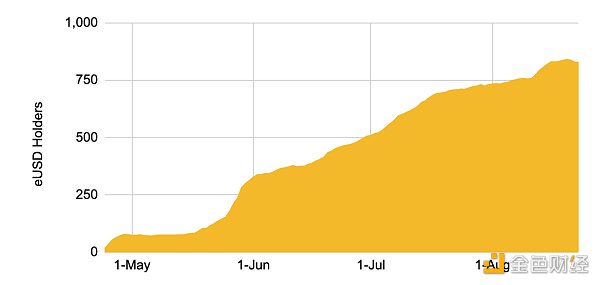

The holdings metric paints a positive picture. The number of eUSD holders has steadily increased since its launch and currently stands at 827 eUSD holders. On average, each eUSD holder owns over $206,000 worth of eUSD, indicating wider adoption among advanced DeFi players.

Figure 11: 827 eUSD holders

Data source: Dune Analytics (@lybra-finance), as of August 23, 2023

Prospects and Risks

As an interest-bearing stablecoin, eUSD may attract income-seeking investors as they can earn a baseline level of returns by holding the stablecoin. This is different from other non-LST-backed stablecoins where holders need to take additional measures to participate in the DeFi market (e.g., staking or lending) to earn returns.

The growth of ETH collateralization provides momentum for the field and Lybra’s development. As the amount of ETH held as collateral increases, the addressable market size also increases accordingly. In other words, it is crucial to better integrate eUSD into the DeFi ecosystem and accept more forms of LST collateral beyond stETH to drive further adoption of eUSD.

Holders should note that the eUSD yield depends on the investment returns obtained from the underlying LST collateral. Therefore, the yield will fluctuate with the volatility of ETH investment returns and may directly impact the attractiveness of holding eUSD.

R introduced by Raft

Raft allows users to generate their stablecoin R by depositing LST as collateral. R is an overcollateralized stablecoin backed by LST, designed to be pegged to the US dollar. Currently, stETH and rETH are supported as LST collateral for minting R. R holders can use R in the crypto ecosystem while earning staking rewards.

The simplified procedure for obtaining and repaying R loans includes the following steps:

1. Deposit stETH or rETH;

2. Mint R with a collateralization ratio of at least 120%;

3. Repay R debt to obtain underlying LST.

To maintain the peg, R adopts a combination of “hard peg” and “soft peg” mechanisms.

Hard peg: Arbitrage opportunities play a role in maintaining the anchor exchange rate. When R exceeds $1.2, users can deposit $1.2 worth of LST, mint 1 R, and sell it on the market for profit. When R falls below $1, redemption helps maintain peg stability. This feature has been disabled, and details of the anchoring mechanism module will be announced soon. (4)

Soft peg: This refers to the design of stablecoins that incentivize users to take action based on expectations of maintaining the peg. For example, when R is below $1, borrowers are incentivized to repay their positions, reducing the supply of R on the market and driving the price back to the peg.

Adoption and Activity

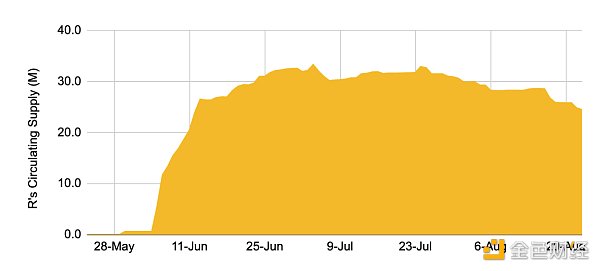

R’s circulating supply grew rapidly in the initial release phase, surpassing 20 million in less than a week after the official mainnet launch on June 5, 2023. This was contributed by a small group of less than 100 holders, with an average of over 200,000 R per wallet. Since then, R’s circulating supply has remained relatively stable with a slight decrease, hovering around the 24 million mark as the average holding per wallet decreases.

Figure 12: R in circulation has 24.5 million coins

Source: Dune Analytics (@dcfLianGuaiscal), as of August 23, 2023

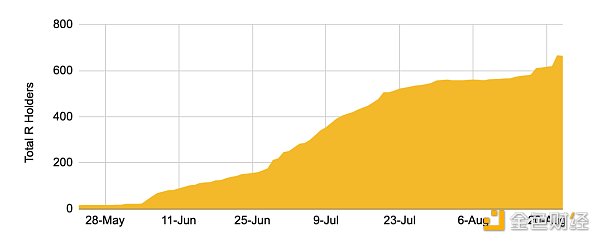

Nevertheless, the growing user base indicates expanding demand among a wider user population, which is a positive signal. The increasing number of holders is crucial for supporting the circulating supply of R and keeping it at a higher level, even as large whales reduce their average R holdings.

Figure 13: The number of R holders continues to increase and has reached 661 people

Data source: Dune Analytics (@dcfLianGuaiscal), as of August 23, 2023

Prospects and Risks

Like other LSTfi projects, R benefits from the tailwind of liquidity staking tokens’ growth. By allowing LST holders to use their LST as collateral to mint R, holders can continue to receive investment returns while freely using R in other protocols in the DeFi ecosystem.

One key point to note is that R is in the midst of a transition; the redemption function has been disabled, and it is seeking to launch an anchoring module. Meanwhile, users should be aware that the anchoring stability of R relies on other mechanisms, such as soft anchoring. Several proposals have recently been made to address the issue of R’s current trading price being slightly below the peg. Specifically, a one-sided DAI liquidity incentive plan and an R savings module have been proposed.

3.3 Centralized Stablecoins

Centralized stablecoins, as the name suggests, are stablecoins issued by centralized entities. These stablecoins are typically backed by fiat currencies held in off-chain bank accounts. Leading stablecoins in the market, such as USDT and USDC, are prime examples of centralized stablecoins.

PYUSD launched by LianGuaiyLianGuail

As one of the most well-known companies in the Web2 field, LianGuaiyLianGuail has launched its own native stablecoin, which is particularly noteworthy. In addition to providing credibility to the crypto ecosystem, entering the stablecoin market for LianGuaiyLianGuail could bring in new users given the wide consumer base of stablecoins.

PYUSD is a stablecoin fully backed by deposits in USD, US Treasury bonds, and similar cash equivalents. It is issued by LianGuaixos Trust Company and is an ERC-20 token. Eligible US LianGuaiyLianGuail balance accounts can use PYUSD.

Use cases for PYUSD:

Transfer LianGuaiyLianGuail USD between LianGuaiyLianGuail and compatible external wallets;

Use PYUSD for peer-to-peer payments;

Select LianGuaiyLianGuail USD at checkout and pay for purchases with LianGuaiyLianGuail USD;

Convert any cryptocurrency supported by LianGuaiyLianGuail into LianGuaiyLianGuail USD.

Prospects and Risks

The wide coverage of PayPal is a competitive advantage for stablecoins. As of the end of the second quarter of 2023(6), PayPal had over 431 million active accounts worldwide. However, PYUSD is currently only available to eligible US accounts, and the corresponding number of active accounts is relatively small. LianGuaiyLianGuail’s foothold in the payment field can contribute to the distribution and adoption of PYUSD. Additionally, LianGuaiyLianGuail can benefit the entire crypto ecosystem by making the process of using stablecoins more seamless for non-crypto users.

Concerns related to centralized risks have always existed due to LianGuaixos’ ability to suspend PYUSD authorization and transfer functions in any possible scenario. This means that LianGuaixos will have the ability to freeze or confiscate assets from individual wallets. Please note that these risks typically apply to any centralized stablecoin (such as USDT, USDC, etc.) as centralized entities may need to invoke certain functions to comply with regulatory requirements in certain situations, although the frequency of such occurrences should be relatively low.

Overall, concerns over centralization, combined with a lack of differentiation compared to other centralized stablecoins, make it difficult for PYUSD to gain adoption from native crypto users who don’t have a real incentive to switch to PYUSD. However, LianGuaiyLianGuail’s wide coverage can help attract non-crypto native users and allow PYUSD to carve out a niche market in this field.

FDUSD, launched by First Digital

FDUSD, the First Digital Dollar (“FDUSD”), is issued by FD121 Limited, a subsidiary of First Digital Limited, a custodian company based in Hong Kong, under the brand name First Digital Labs. This stablecoin was first launched in June 2023 and is fully backed by cash and cash equivalents.

FDUSD can be used on the Ethereum and BNB chains, with plans to support more blockchains in the future.

Recent Developments

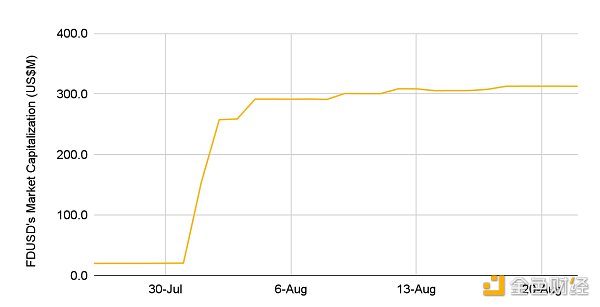

In early August, Binance announced that users would enjoy zero maker and taker fees for BTC/FDUSD spot and margin trading pairs for a limited time, resulting in a surge in the market value of FDUSD.

Specifically, the market value of FDUSD has increased by more than tenfold, from around $20 million in early August to over $312 million currently. The daily trading volume has also significantly increased from around a few hundred thousand dollars before the announcement to over $15 million now.

Figure 14: Market value surge of FDUSD in August

Data source: Coinmarketcap, Binance Research, as of August 23, 2023

Outlook and Risks

Listing on Binance and the zero trading fees for certain FDUSD trading pairs have contributed to the growth of FDUSD. However, it remains to be seen whether FDUSD can sustain this growth trajectory when the zero fee incentives are gradually phased out. It is important to observe broader market adoption, such as integration with other centralized exchanges or increased usage in DeFi.

Like any new stablecoin, the stability of FDUSD, pegged to the US dollar, will be tested over time to understand its volatility. As a collateralized stablecoin, the security and liquidity of its reserves are crucial for the stability of FDUSD. Users may find it helpful to refer to FDUSD’s attestation reports for indications of the composition and health of the collateral reserves. Other risks include operational risk, regulatory risk, and counterparty risk, which are detailed in the FDUSD whitepaper.

4. Market Development

4.1 Incentivizing DAI Adoption

MakerDAO launched the Enhanced DAI Savings Rate (“EDSR”) on August 7, 2023.

This mechanism temporarily increases the DAI Savings Rate (“DSR”) available to users through a multiplier. The multiplier is determined by the utilization rate of the DAI Savings Rate contract, which is the amount of DAI in the savings contract relative to the total supply of DAI.

The DSR was initially increased from 3.19% to 8% to stimulate DAI growth by increasing demand. This incentivizes holders to deposit DAI into the DSR contract, reducing circulating supply. DAI effectively becomes the highest-yielding stablecoin, enhancing its competitiveness.

Recently, a new proposal was passed to reduce DSR from 8% to 5% in order to “ensure that regular DAI holders benefit from EDSR, rather than disproportionately benefiting ETH whales.” Specifically, many large participants benefited from “arbitrage borrowing” by borrowing DAI at a rate of 3.19% and earning an 8% EDSR yield.

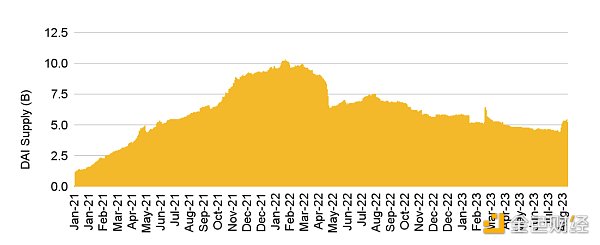

Just before the launch of EDSR, the supply of DAI in August fell below 4.5 billion for the first time since May 2021. This is a significant decrease compared to the peak of 10.3 billion in February 2022. However, with the increasing demand for DAI, the launch of EDSR has played an important role in reversing the situation. Although still far from the peak of the bull market, DAI supply has increased by about 16% from the bottom and currently stands at around 5.2 million DAI.

Figure 15: DAI supply has declined in the past year, but has recently rebounded slightly

Data source: Makerburn, as of August 20, 2023

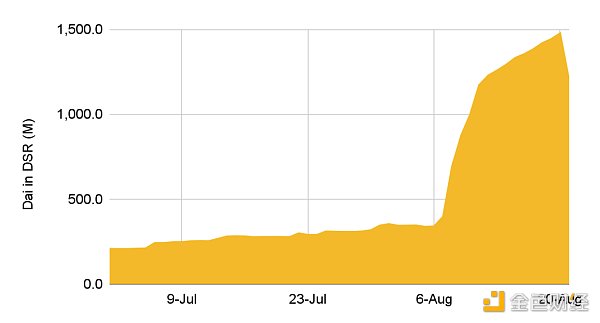

The most significant impact is the growth of DAI in DSR, which has increased from less than 400 million to approximately 1.2 million, nearly tripling. The recent decline in the past few days is due to the withdrawal of users from the DSR contract after the reduction of DSR from 8% to 5%.

Figure 16: Surge of DAI in DSR after the launch of EDSR

Data source: Makerburn, as of August 20, 2023

Compared to US Treasury bonds, the increase in DSR provides an attractive on-chain alternative, which helps boost demand for DAI and increase the adoption of Maker’s lending protocol. On the other hand, it is worth noting that the increase in DSR has a direct financial impact on MakerDAO. This can be seen as the customer acquisition cost of the protocol. Based on the current estimates and parameters, DSR is expected to cost MakerDAO $56.3 million per year.

Considering that DSR will be adjusted based on utilization, it will be interesting to see how the utilization changes when interest rates normalize. Our speculation is that DSR may maintain a rate at least consistent with the yield of other stablecoins to remain competitive.

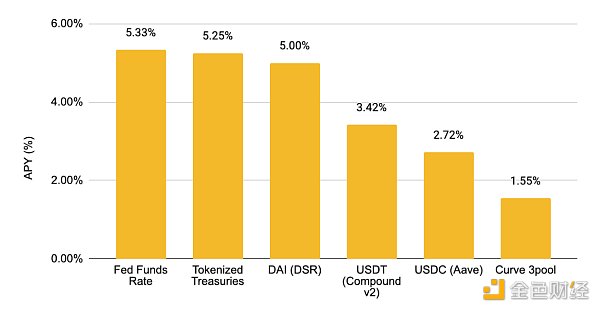

4.2 Integrating Real-World Assets

In the context of rising interest rates, US Treasury bond yields have steadily increased and have already comfortably surpassed DeFi yields. In order to remain competitive and take advantage of the returns in the traditional financial (“TradFi”) market, stablecoin issuers have allocated a portion of their reserves to invest in TradFi instruments. This can be observed from the audited reports of centralized issuers such as Tether and Circle, as well as MakerDAO’s balance sheet.

It is worth noting that MakerDAO has always been at the forefront of tokenizing real-world assets (“RWAs”), and its funds benefit from the rise in asset class yields. Currently, MakerDAO’s RWA exposure exceeds $2.4 billion, accounting for 58% of its revenue. Considering that DeFi yields are far below TradFi yields, it is not surprising to see more stablecoin protocols exploring the integration of RWAs to increase their financial income and potentially pass it on to stablecoin holders to increase the attractiveness of their stablecoins.

Figure 17: TradFi returns exceed DeFi stablecoin returns

Data source: Federal Reserve Bank of New York, rwa.xyz, SLianGuairk, Compound, Aave, Curve, Binance Research, as of August 22, 2023

4.3 LST Adoption

With the growth of the LST market, we have witnessed the diversity and scale of the LSTfi ecosystem. More projects have already entered or are about to enter the market to take advantage of the industry’s growth. In this regard, in addition to those mentioned in the previous section, we have seen an increase in the number of stablecoins supported by LST that have been launched or are about to enter the market.

Examples include:

GRAI by Gravita: The Gravita protocol is a lending protocol that allows users to mint GRAI, a super-collateralized debt token guaranteed by LST and its stable pool (10).

mkUSD by Prisma: Prisma enables users to mint a stablecoin called mkUSD, which is fully collateralized by liquid staked tokens (11).

USDe on Ethereum: Ethereum allows users to deposit USD, ETH, or LST as collateral to create USDe (12).

It is worth noting that we have also witnessed mature DeFi projects related to stablecoins, leveraging the growth of LST by diversifying the risk exposure of collateral, including LST.

These include:

Curve: Curve’s crvUSD stablecoin can be minted by using Frax’s strxeth or Lido’s wstETH as collateral. Currently, wstETH accounts for the largest share in the collateral of crvUSD, at 44%.

MakerDAO: LST collateral in the form of wstETH (wrapped staked ETH by Lido) has significantly increased in MakerDAO’s vaults, from less than 12% of MakerDAO collateral to over 40% currently (13).

Frax Finance: Frax Finance, the issuer behind the Frax stablecoin, has direct exposure to LST through its liquid staking solution. Frax (frxETH) is a stablecoin loosely pegged to ETH (14).

Frax Finance is the issuer behind the Frax stablecoin and has direct exposure to LST through its liquidity staking solution. LST is directly involved. Frax Ether (frxETH) is a stablecoin loosely pegged to ETH.

5. Conclusion

Stablecoins play a crucial role in the crypto ecosystem by providing price stability, enabling seamless transactions, and bridging the gap between TradFi and the crypto world by offering users familiar stable value. As the crypto ecosystem matures, the importance and relevance of stablecoins may continue to grow.

Although the competitive landscape is currently dominated by centralized, fiat-backed stablecoins such as USDT and USDC, the demand for decentralized alternatives means that the competition is far from over. In the past few months, new stablecoins have emerged, each with its own unique characteristics, indicating that project teams are still interested in building in this area and challenging the existing market.

Considering the scale, resources, and liquidity currently possessed by leading stablecoins, achieving market leadership is not an easy task. However, we look forward to a more diverse competitive landscape and new entrants also benefiting from it.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Bitcoin Spot ETF Application Inventory When will it be approved?

- Interpreting the lending platform Fuji Money unlocking the financial potential of Bitcoin Layer2

- Messari Founder Most Bullish on Cryptocurrency Job Market

- Bitcoin Smart Contract Evolution RGB-Driven Web3 Revolution

- Changtui The NFT market will recover, and we will usher in another epic, anti-gravity NFT bull market.

- Grayscale won, but not completely SEC can still reject BTC ETF

- Interview with Circle CEO by Fortune What role does stablecoin play in the cryptocurrency market?