Decentralized stable currency monetary policy and fiscal policy governance

Foreword: How to achieve a decentralized stable currency? How should monetary and fiscal policies be formulated and implemented? This paper presents a framework that attempts to eliminate the need for human involvement to achieve a programmatic decentralized stable currency. The author of this article, Evan Kereiakes, is translated by the "HQ" of the "Blue Fox Notes" community.

Summary

In the long run, good governance is one of the most decisive features of a healthy ecosystem (political, economic, social). As ecosystem participants continue to join and exit, they must adhere to a set of rules and ideals that exist through long-standing governance structures.

In the blockchain world, decentralized governance is crucial, but it is difficult to do it right. An appropriate incentive structure must be established to be able to change in a regulated manner. To achieve this, many blockchain ecosystems have begun to become more central, but over time, they will move toward more decentralization.

- The history of cryptography changes: the enlightenment of the two pits in Germany and the Enigma machine to the mining machine manufacturers

- Viewpoint | Digital currency will open the currency scenario for blockchain technology applications

- How to make a steady profit without losing, become the king of BTC escape?

This article addresses some of the monetary and fiscal policy governance specific to decentralized, price-stable cryptocurrencies, and suggests some ideas on how to automate the core components of the stable currency ecosystem, thereby reducing manpower. The need to invest.

Who is controlling the currency?

As the saying goes: "Cash is king", that is: "Who controls the cash flow who is the boss."

To determine if the stable currency ecosystem is decentralized, look at who controls the funds or collateral, and whether this responsibility has become more decentralized through governance? Monetary and fiscal policies can be said to be the most powerful leverage mechanism in the stable currency ecosystem, balancing the stability of mortgages and the growth drivers of fiscal spending.

As ownership of the governance process becomes more concentrated, control of monetary and fiscal decisions may be more central at the outset. In the early stages, centralization is justified because of the need to have fail-safe ownership in order to accelerate development and rapid system upgrades, leaving time for the dissemination and implementation of more important monetary and fiscal policies.

The nature of attribution or transfer should reflect the goal of the agreement, that is, to achieve autonomy or to open up to a broader network. The transition to decentralization may be gradual, as the founding organization's expertise in managing decentralized ecosystems must be given new vested interests.

Any fiscal or monetary decision may be affected by a governance vote, where X% of the verifiers or miners agree to a certain outcome of the network. This is a traditional approach to managing blockchains that is effective for some projects.

However, users and investors must believe in people, rather than believing in networks that are run by mathematics, which will lead to a deterioration in the future decision-making of the agreement and a more procedural origin of the decentralization movement. If insiders collude or control most tokens and vote for their own benefit, the voting results will be affected by the game. However, more autonomous decision making methods may be affected by unforeseen risks in system modeling.

So it's best to keep the simplicity of autonomy from the beginning, and gradually change from one governance to another as you learn more about system behavior. The focus of the rest of this paper is to provide a programmatic governance framework for monetary and fiscal policy decisions that stabilize the currency, rather than relying on human voting solutions.

Monetary policy governance

Provision for endogenous and exogenous asset reserve ratios

In order to maintain the value of a stable currency during economic austerity or shock, a countercyclical stabilization mechanism is needed. The two-coin stable currency mechanism, one of which is stable currency and the other is collateral, is the most promising design to achieve decentralized stability.

They rely on some form of endogenous stability (ie, endogenous income streams, such as coinage taxes, transaction fees, or mining incentives) whose value reflects the need to participate in a stable currency economy. Most decentralized stable coins rely more or less on some form of external stability, such as anchored underlying assets. Both forms of stability include provisions to support stable coins, and the total mortgage rate requirement is always greater than or equal to 100% of the stable currency supply.

If the exogenous reserve ratio is always at 100% of the stable currency economy, then no endogenous reserves are needed. However, this type of stable currency may be subject to centralization and review risks. However, during periods of severe decline in demand for stable currencies, the value of full endogenous reserves may spiral downwards, and these types of stable currencies have failed.

Therefore, the use of a hybrid approach is advocated here, that is, when the exogenous reserve ratio deviates from 100%, a decision point arises: what level of exogenous reserves is appropriate to ensure stability.

The underlying asset anchored by the Stabilizing Coin is the highest value exogenous correction mechanism that can be used to contract the economy at an anchor price or to supplement the endogenous reserve value. For most stable currencies, cash or cash equivalents are the underlying assets of this anchoring mechanism, and as the economy grows, there may be plenty of opportunities through the power of the coinage tax.

Other exogenous assets, including cryptocurrencies, can be used to achieve greater decentralization and minimize volatility and downside risks through appropriate portfolio management methods. In this analysis, it is assumed that the value change of each reserve asset does not depend on portfolio management decisions, but on other reasons, such as market behavior or expected changes.

Assets consisting of endogenous reserves are usually unstable, and their ratio to the money supply will fluctuate within a large range depending on the economic cycle or growth expectations. In extreme cases, the endogenous reserve will enter a recursive descending spiral that will fall in value when it is most demanded. In order to make up for this, the value of endogenous reserves can be discounted by appropriate expansion conditions to obtain more accurate real stability.

First, instead of using the market value of endogenous reserves, it is better to define a valid endogenous reserve value, which is expressed as “epsilon”, which is to offset the endogenous value by subtracting the value of risk (for example, 1% VaR in March). The downward movement of reserves. Second, use the external survival reserve ratio to discount the survival reserve ratio to adjust to this reality: the endogenous reserve brought by the lower exogenous reserve ratio bears more economic stability burden.

Index factors help to further discount the value of endogenous assets because they are not direct substitutes for exogenous assets. This factor also accelerates the supply of exogenous reserves in the event of an economic shock, which is an effective level of redundancy. The above adjustment yields the following equation, which is based on the effective endogenous reserve value and the exogenous reserve ratio, and the percentage of the coinage tax assigned to the exogenous reserve:

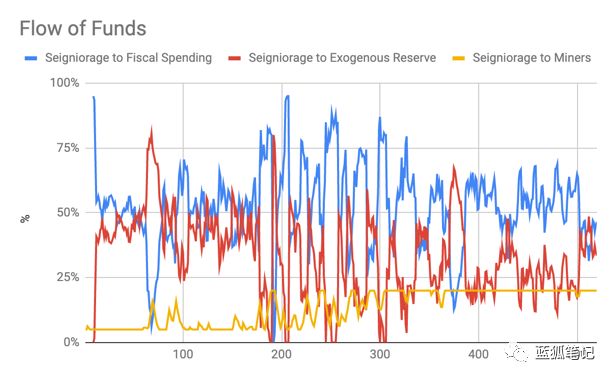

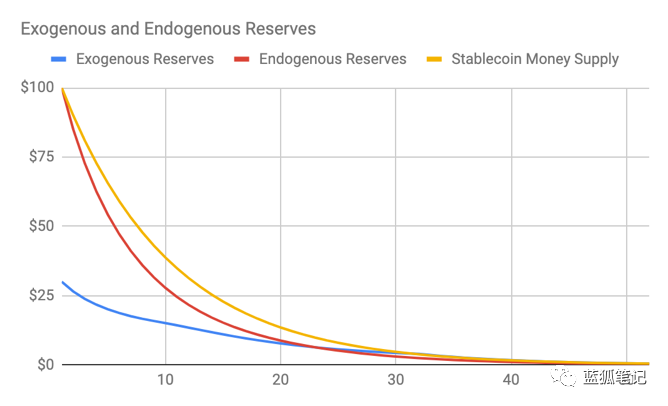

The chart below shows how the decentralized, programmed reserve supply equation works. The first image shows the output of the above equation. The coinage tax can only be used for financial expenses after the agreement stabilization fund (miners and exogenous reserves) is properly provisioned. Please note that miners or verifier rewards are not covered by this operation. Monetary and fiscal decisions will only work if the miners and verifiers are compensated for the fixed and variable costs of the blockchain.

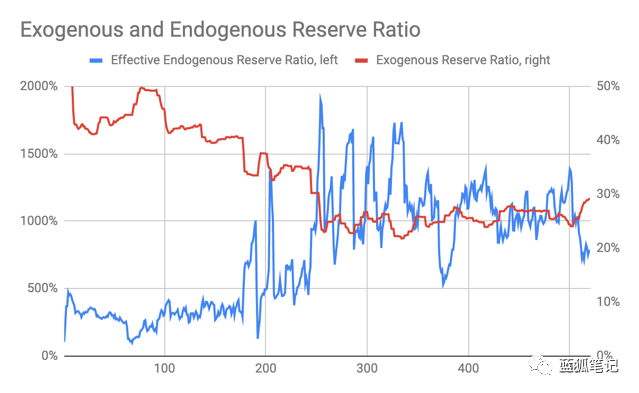

The second graph shows how the exogenous reserve ratio changes over time as a result of the coinage tax distribution function and the economic cycle. Please note that the endogenous reserve model shows very high volatility.

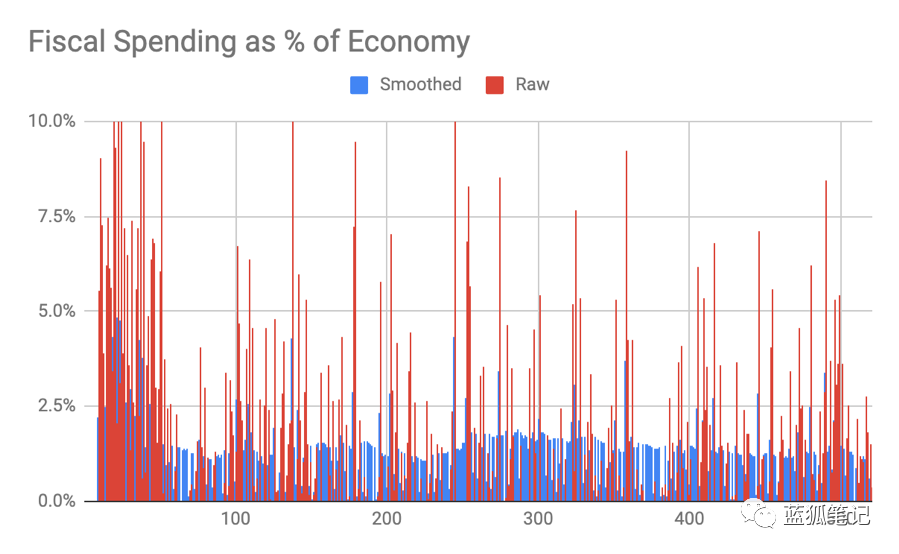

The third chart shows the balance of the coinage tax that can be used for fiscal expenditure. Since fiscal expenditures may fluctuate, a simple smoothing algorithm can be used to make fiscal expenditures consistent with the passage of time. Fiscal policy will be discussed in more detail later in this article.

Dry use of expected reserves (exogenous and endogenous)

Both endogenous and exogenous reserves operate while absorbing changes in demand for stable currencies. Reserves are scarce resources and must be properly managed in this service.

The endogenous reserve is an important tool for achieving stability and adoption in the form of decentralization, and is the first line of defense to maintain the anchorage of stable coins. Exogenous reserves represent a second (more advanced) stabilizing defense mechanism because, in theory, they are less relevant to the economic cycle and price cyclical changes of stable currencies.

The farther the exogenous reserve ratio is from 100%, the greater the potential risk of marginal impact of endogenous collateral sales decline. In order to maintain a stable anchor price during the economic contraction, who decides when to use the endogenous reserve, or the exogenous reserve, or both?

The countercyclical mechanisms by which each stable coin provides greater stability to endogenous reserves during the austerity process are different. During the period of reduced or contracted demand for stable coins, endogenous reserve prices have fallen, volatility has increased, and demand has decreased… This is a dangerous triangle where multiple forces work together to erode the stability of endogenous assets.

Then at some inflection point, the endogenous asset price enters the death spiral and never rebounds. Only two forces can avoid the emergence of a death spiral, one is the lower limit of demand (uncertain), and the other is exogenous assets (determined). This is why decentralized stable coins often maintain an exogenous reserve because it is sure to break the price spiral of endogenous reserves and is more effective than any other agreement mechanism.

Assuming that the reserve has been properly provisioned (as described in the previous section), the decision on when to use each collateral should be attributed to optimizing system resources. Therefore, endogenous reserves are the first line of defense, as long as they are "all in one".

This framework, if performed properly, is very costly for attackers to break anchors. Endogenous reserves are used to tighten the economy: 1) the higher the exogenous reserve ratio before being used as the last line of defense; 2) the stronger the independence of the economic operation from the exogenous assets – this is The ultimate goal. The formula for determining the level of exogenous reserves to be sold based on the Endogenous Reserve Ratio (NRR) is defined as follows:

The decision to use endogenous reserves or exogenous reserves is determined by whether the endogenous reserve consumption rate is greater or less than the stable currency supply deflation rate. If the endogenous reserve destruction rate is lower than the money supply deflation rate, then the endogenous reserve ratio will continue to be used to deflate the economy until the 100% external survival reserve ratio is reached. At this time, the system can be converted into an external survival fund. Reserve.

If the endogenous reserve destruction rate is greater than the money supply contraction rate, then the exogenous reserve can be used for economic deflation. But this does not mean that only exogenous reserves are used, as there are some problems with the same capacity as described earlier.

Conversely, the above equation illustrates how exogenous reserves should be used to supplement endogenous reserves. The “x” index is an input value that can be pre-set or programmatically set so that the exogenous reserve can be spent faster or slower than suggested by the model and can contain other input values, such as The starting or current exogenous reserve ratio.

In summary, if dNRR is negative, then the exogenous reserve is sold. The greater the decline in NRR, the more exogenous reserves will be sold to subsidize the stability of its endogenous reserves. Although there are many scenarios and special cases that cannot be described by a single simple formula, this is an effective framework for solving complex problems. If the stable currency economy turns back to expansion, then the algorithm described in the previous section will be used to automatically rebalance the reserve at a certain speed.

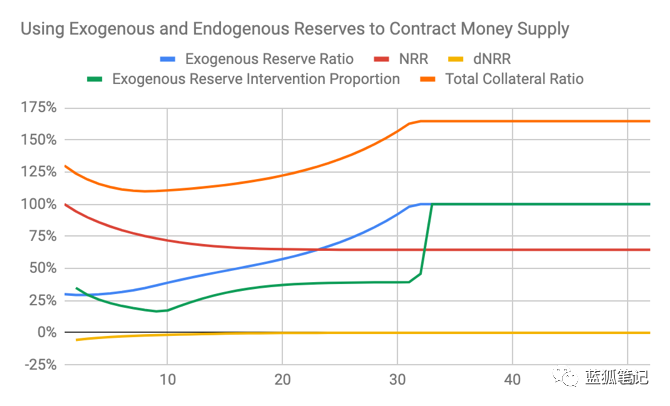

The following is the result of a stable currency intervention simulation using endogenous and exogenous reserves. Although this situation is very unfavorable, it is necessary because it ensures that the agreement can fully stabilize the economy by anchoring the stabilized currency price.

Fiscal policy governance

Fiscal policy is the engine of system resource allocation, just as the government guides resources to stimulate growth and benefit voters. Financial resources can be any form of agreement income, which can consist of a seigniorage tax, other income, taxes, transaction costs, and so on. The fiscal governance logic in this section applies only when the monetary reserve is fully supplied, as stability is a basic requirement.

The goal of a programmed decentralized fiscal policy is to promote the efficient allocation of financial resources while eliminating the need for voting or human input. Similarly, the inclusion of major decisions, such as fiscal expenditures, in governance voting will raise issues that arise from the inherent risks of centralizing the distribution of tokens and relying on people rather than algorithms.

In these cases, bad actors may try to bankrupt the fiscal reserves, so various additional precautions can be taken, all of which are long-term guarantees that the agreement becomes a prerequisite for fiscal expenditure. A vote based on streamlined and transparent authorization for “whitelisted” or “blacklisted” entities within the fiscal system is an effective enhancement.

These tasks can also be performed as boundaries, which are triggered automatically when suspicious activity occurs, thereby limiting fiscal expenditure. The "stability-as-a-service" scheme is a method of performing this operation programmatically. Further discussion of this and other ways to secure financial resources will save costs.

A programmatic framework is very effective for the federal fiscal expenditure model, where various decentralized service providers (companies) with unique values compete to achieve capital allocation optimization.

In this way, resources can be allocated more efficiently, and it means that the marginal propensity to consume and the fiscal expenditure multiplier of the stable currency are higher than the legal currency government. As mentioned earlier, fiscal expenditures can be smoothed by a simple algorithm to ensure that financial resources are available even during periods of little or no agreement revenue.

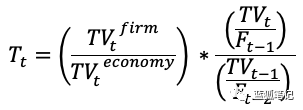

The following formula illustrates the change in the weight (w) of each company's financial resources in the economy based on the standardized transaction volume multiplier momentum (T) and the standardized money supply holding ratio (M), where (gamma) ) is a level of programmed leverage that divides the benefits of resources based on economic conditions and currency usage.

Regarding the decomposition of the (T) variable, the input values are: 1) the company's relative total transaction volume, 2) the fiscal expenditure multiplier (ie, the expenditure efficiency), the transaction volume (TV) divided by the fiscal expenditure (F), and 3) Multiplier momentum. In this example, (TV) stands for GDP.

The composition of the multiplier momentum re-adjusts the expenditure multiplier for each period to more evenly reflect the contribution of the early and late cycle firms. The weighted moving averages (TV) and (F) help to smooth out fluctuations over time, as both can sometimes fluctuate.

The money supply part of the equation takes into account the speed of circulation of the broader stable currency economy, the speed of money flow in each company, and then returns to companies with lower circulation rates because they contribute significantly to the coinage tax. A longer holding period to return will help stabilize the allocation of funds at different times and increase the return on companies with low circulation rates.

Standardizing the return on holdings by (TV) will eliminate the gains gained through manipulation and thus enforce honest behavior. Moving averages are also useful for the composition of money supply because they maintain a more consistent return by smoothing time volatility and enforcing long-term commitments.

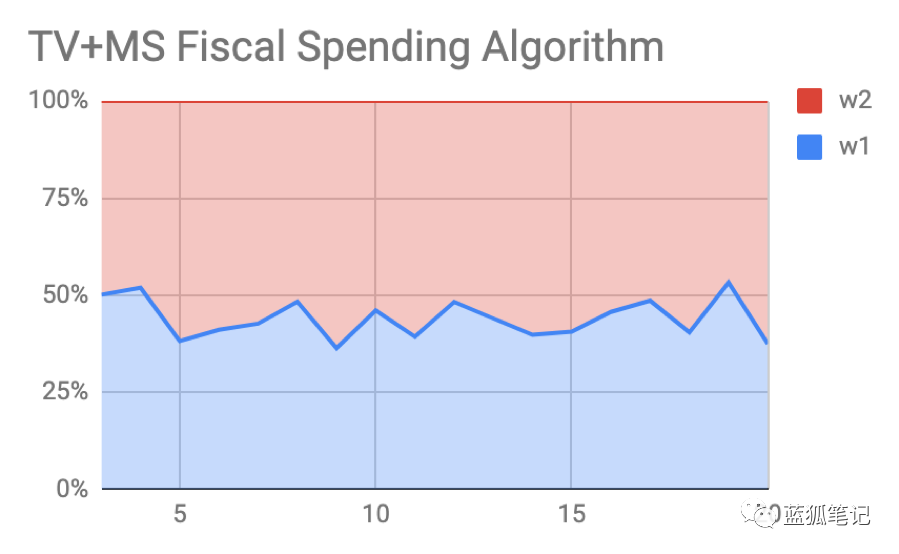

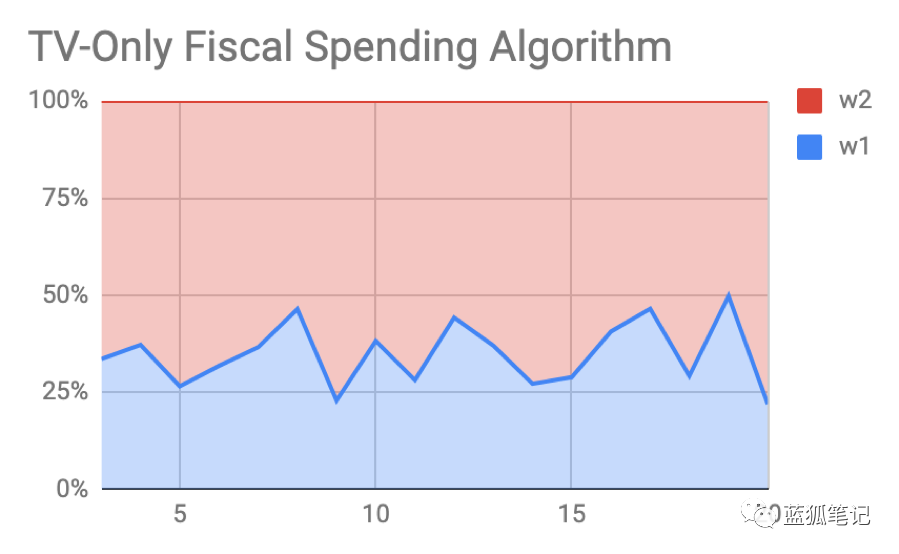

The following is a simulation of an economy with two companies, showing the volume of transactions (TV) and money supply (MS) as the result of the investment that determines the financial allocation. Company 1 owns half of the company's trading volume, so (TV 1) = (1/2) * (TV 2). But company 1 holds 4 weeks of funding (speed 1 = 13), and company 2 holds 2 weeks of funding (speed 2 = 26). Therefore, Company 1 generated a larger percentage of the coinage tax (1-V1/(V1+ V2)).

The (TV) input values in the model have some randomness. The model gamma value is 0.5, between 0 and 1, which is a reasonable choice for the simulation, but the lower gamma value helps to direct economic activity to the place where the rent is drawn through transaction costs, unless the agreement is also extracted through the detention period. The rent holding the funds.

——

Risk Warning : All articles in Blue Fox Notes can not be used as investment suggestions or recommendations . Investment is risky . Investment should consider individual risk tolerance . It is recommended to conduct in-depth inspections of the project and carefully make your own investment decisions.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Research Report | Preliminary Study on the Digital Currency of the People's Bank of China: Goals, Positioning, Mechanism and Impact

- QKL123 market analysis | Bitcoin continues to drop, will fall below $ 9,000? (0924)

- Winners such as Tencent, Fidelity and Lotte, Everledger finally won $20 million in Series A financing

- Jia Nan, Zhi Zhi Kong Jianping: It is only a matter of time before bitcoin breaks through 100,000 US dollars. The limit of computing power in 2020 is doubled.

- Analysis | Is the Black-Scholes model for pricing traditional financial derivatives also applicable to Bitcoin?

- Binding social media to send Bitcoin with one click, Bottle Pay received $2 million investment

- Babbitt Column | From Highlights to Fall: P2P Brings Revelation to Defi