Opinion | Synthetic tools will become the ladder to the future of DeFi and achieve the popularity of DeFi

Author: Joel John

Translation & Proofreading: Min Min & A Jian

Source: Ethereum enthusiasts

Editor's note: Original title was "Introduction | Asset Synthesis in DeFi: Synthetix"

- 36 transactions cleared the HEX investment address, 48,000 ETH were scattered and transferred. It is suspected that the scam project is finally hammered?

- DeFi weekly selection 丨 DeFi lockup value is approaching US $ 1 billion. Will the "ruler" Maker be overthrown in 2020?

- Bitcoin's eternal battle: fighting entropy, rising on the borders of order and chaos

Note: I have nothing to do with the Synthetix team. This article is not investment advice and should not be considered as investment advice. As of this writing, I only own $ 1.50 worth of assets on the Synthetix platform, which I bought previously to test the Mintr application.

The so-called synthetic asset is an asset that simulates the change in the price of a certain type of basic asset; in this way, people do not need to actually hold that type of basic asset, and only need to hold a synthetic asset, they can obtain risk returns. In some cases, people want to trade a financial instrument or hedge its price fluctuations, but they are not immediately available because of compliance issues. At this time, synthetic assets come in handy. The solution for the DeFi ecosystem is very simple. As long as you have a price predictor, pledges that can resist price fluctuations within a certain range, and liquidity gathered, it is possible to “issue” commodities, currencies, and cryptocurrencies without the involvement of banks. This article will explore the incentives for the Sythetix project and developments over the past year.

Synthesis tools-the basics

Today, synthesizer tools in the DeFi space need to have the following components

-

A sufficiently decentralized price predictor that can provide data to the system (off-chain price data) -

Collateral provided by secondary financial instruments (such as SNX tokens) to endorse the issuance of synthetic assets -

The price band in which synthetic assets are allowed to be bought and sold . (Without a price range, the pledge used to endorse the synthetic asset may not be able to withstand price fluctuations.)

As a simple example-let's imagine a scenario where 1 BTC worth $ 1,000 is used as collateral. The price of ETH is $ 100, and the system's pledge rate requirement is 500% (that is, your pledged value must be 5 times the value of your borrowed assets). You can borrow $ 200 worth of ether (or 2 ETH) by pledged 1 BTC. In the above example, after pledged 1 BTC, you can get 2 sETH (synthetic ETH) and trade in the liquid market.

Now, let's assume that Satoshi Nakamoto is using his huge amount of bitcoin to make the market and stabilize the price of bitcoin.

Then:

-

If the price of ETH drops to around $ 75, your "liability" will drop (from $ 200) to $ 150. You only need to repay $ 150 (instead of $ 200) to get back the 1 BTC pledged. In this case, if you pledge 1 BTC to sell sETH immediately when generating sETH, you can earn $ 50 (previously selling sETH to get $ 200, now spend $ 150 to buy back sETH and redeem BTC, this Made $ 50). -

If the price of ETH spikes to $ 150, your debt (from $ 200) rises to $ 300. If you want to redeem one of your BTC at this time, you must repay $ 300. In this case (if you sold sETH in the first place) as your debt increases, it is equivalent to losing a portion of your collateral ($ 100 worth of BTC). -

It should be noted that the fluctuation of ETH price may cause the actual pledge rate to be lower than the target pledge rate. In this case, the liquidation price range will move up and down.

The supply of sUSD is reduced when the loan is repaid, so this behavior is known as BURN

If you want to understand the concept, I highly recommend you experience Mintr on Synthetix. There is also a great article here to help you understand Synthetix's ecosystem.

Get started with Synthetix

Synthetix applies the above model to fiat currencies, digital assets (long and short) and physical commodities (gold). Its pledge rate is 750%. In other words, for every sUSD (combined USD) valued at $ 1, it is necessary to lock the SNX valued at $ 7.5 in the smart contract. There are two main types of participants in the Synthetix ecosystem, and their interaction is the key to creating value for the ecosystem.

Pledger-A person who earns money from the ecosystem by pledged SNX (Synthetix Token). Whenever a transaction occurs, Synthetix's pledger is rewarded for it. According to Synthetix's minimal white paper, rates range from 0.3% to 1%. So far, the transaction volume on Synthetix has reached approximately $ 720 million, and the system has issued a total of $ 3.1 million to pledgers. In addition, SNX has a built-in inflation system, which is similar to the bank deposit mechanism. It can also be said that the pledger is the bullish net long of SNX against the dollar. If the U.S. dollar appreciates relative to the underlying asset (i.e., the price of SNX is lower), then pledges need to be added.

Trader-a user who only enjoys the risky returns of assets such as BTC, foreign currency or physical commodities by holding synthetic assets, but does not participate in the centralized exchange ecosystem. It is arguable that there are traders who are just trying to evade compliance requirements, after all-on the Synthetix platform, I can exchange ETH for gold in a matter of minutes and vice versa.

If SNX appreciates, pledgers will benefit from it. If the assets bought by the trader (such as BTC, gold, etc.) appreciate, the trader will benefit from it. This means that if the price of SNX itself falls, the pledger will suffer losses because they need to pledge more SNX to avoid triggering the liquidation mechanism after the pledge rate is below 750%. Similarly, if the price of SNX rises relative to synthetic assets (for example, sETH), the pledger will benefit because the synthetic assets required to repay are reduced.

Another example !

-

The price of ETH is $ 100. You have $ 750 worth of SNX, and each SNX is worth $ 1. -

You pledged $ 750 worth of SNX (750 SNX) on the Mintr app and borrowed 1 sETH. -

Your liability in the system is $ 100. Suppose you sell the borrowed 1 sETH in the market for $ 100, and after the price drops, you buy back 1 ETH for $ 80, pay off the debt, get back the 750 SNX deposit, and earn It's $ 20. -

Assuming that the price of ETH is stable at $ 100, and the price of SNX drops from $ 1 to $ 0.5, you need to pledge another 750 SNX to prevent your SNX from being locked in the smart contract.

Note: Mintr can only generate sUSD at present.

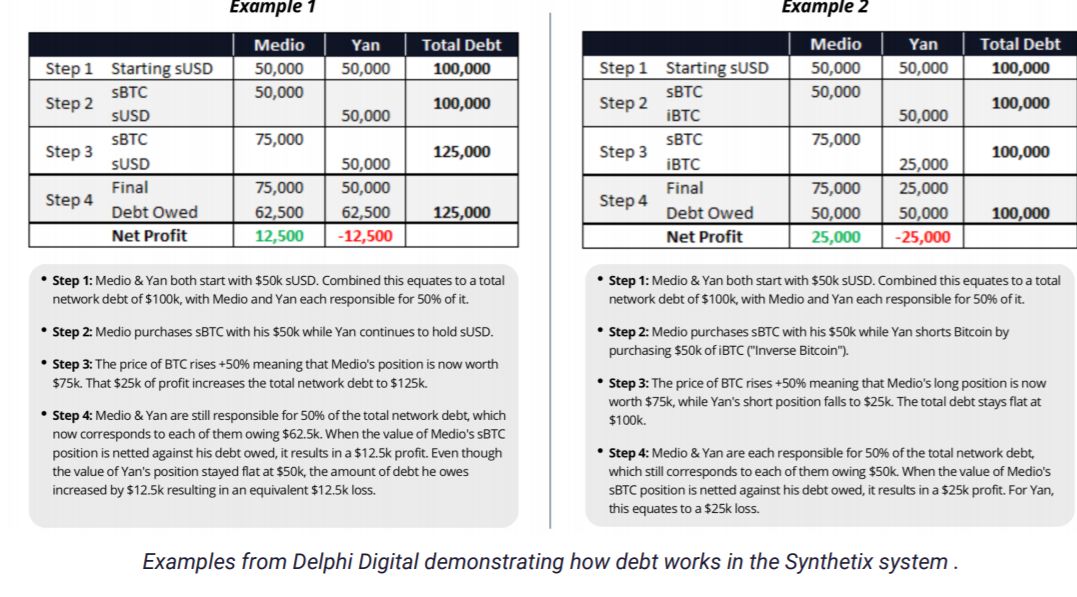

In determining the debt balance of the entire system, Synthetix used the "wide network balance sheet" approach, which was simplified in the minimal version of the white paper into the following infographic.

left:

-

Both Medio and Yan initially pledged sUSD worth 50,000 USD. Adding the two together, the total network debt is $ 100,000, and Medio and Yan each bear 50%. -

Medio purchased sBTC with sUSD worth 50,000 USD, and Yan continued to hold sUSD. -

After BTC's price rose by 50%, Medio's assets were worth $ 75,000. The extra $ 25,000 increased the entire network's liabilities to $ 125,000. -

Medio and Yan each account for 50% of the entire network's liabilities, which means that each of them has a debt of $ 62,500. Medio's sBTC not only pays off his debts, it also brings in $ 125,000 in revenue. Although Yan's sUSD is still worth $ 50,000, his debt has increased by $ 125,000.

-

Both Medio and Yan initially pledged sUSD worth 50,000 USD. Adding the two together, the total network debt is $ 100,000, and Medio and Yan each bear 50%. -

Medio bought sBTC with sUSD worth 50,000 USD, and Yan bought iBTC worth 50,000 USD to short BTC. -

After the price of BTC rose by 50%, Medio's assets were worth $ 75,000, while Yan's iBTC dropped to $ 25,000. The total debt of the entire network is $ 100,000. -

Medio and Yan each account for 50% of the entire network's liabilities, which means that each of them has a debt of $ 50,000. Medio's sBTC not only pays off his debts, it also brings in $ 25,000 in revenue. Yan would have to bear a loss of $ 25,000.

Synthetix does not require traders to participate in any form of pledge. You can exchange ETH to equivalent synthetic gold in a ratio of almost 1: 1 through Uniswap and Exchange.synthetix.io within 5 minutes. In other words, traders do not need to meet the 750% pledge rate requirement. Only those pledged ("debt" in the form of sUSD) need to meet the pledge rate requirements. Unlike MakerDAO, the SNX system currently has no clearing procedures. If the pledge rate drops below 750%, the SNX system will lock the tokens in the smart contract, and it can't be taken out until the pledge rate returns to 750%.

Synthetix data

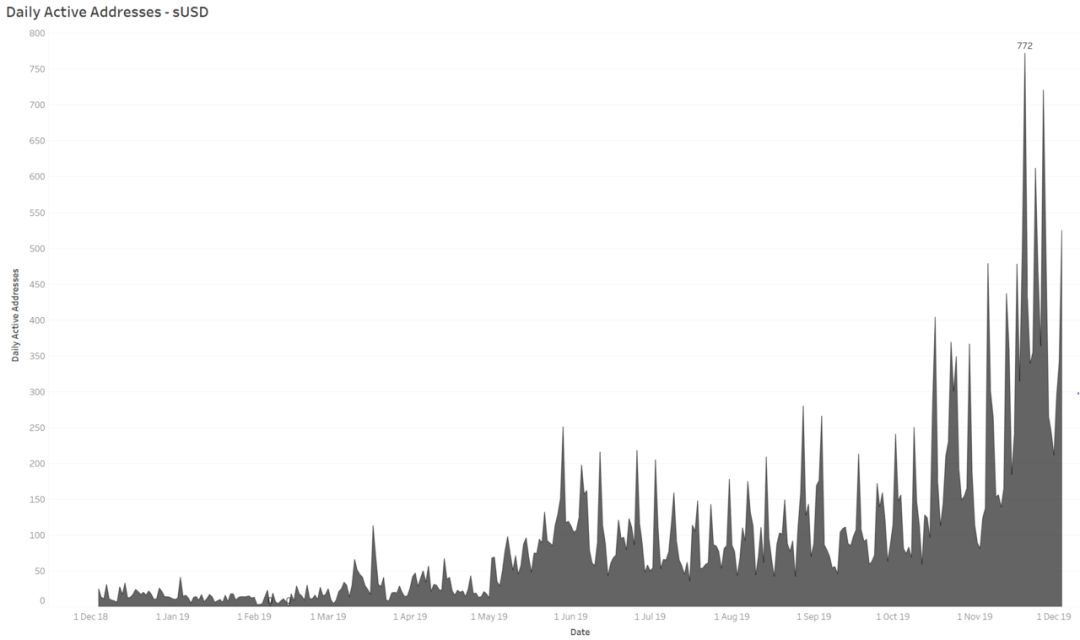

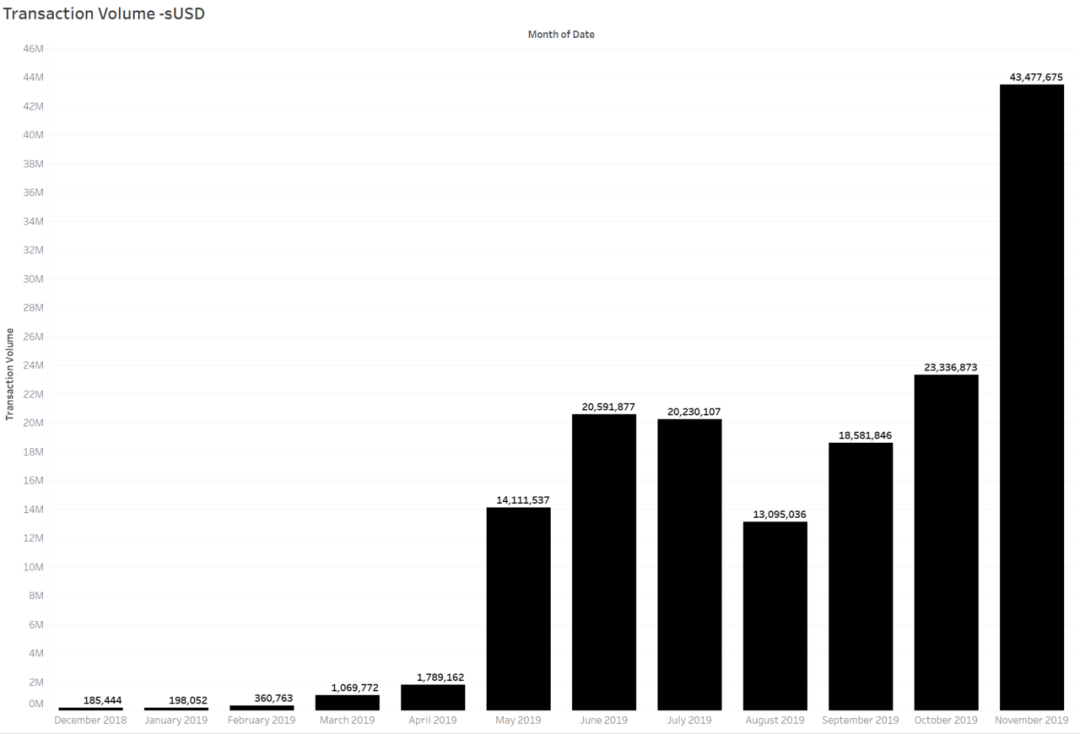

Note: This article uses only sUSD data for analysis. Given that there are other types of assets on Synthetix (sBTC, sDeFi, etc.), the actual data may be higher. Several data science teams are analyzing this data. After the data analysis is released, I will attach a hyperlink.

At present, the active user group of sUSD is about 1/50 of Tether, and 1/3 of Tether's rival MakerDAO in the decentralization field. However, given the increasingly fierce competition in the DeFi space, and there are still many huge competitors, it is not easy to have about 700 users on this synthetic dollar distribution platform. Based on these data, SNX did defeat more "traditional" DeFi projects like GUSD (DeFi project on the Gemini exchange).

In terms of trading volume, Synthetix is still in its infancy. Since the Synthetix system is used as a synthetic asset issuance platform, a reasonable valuation method based on valuation and active user groups is not suitable for the system. (So far) Synthetix did prove that one of my assumptions was wrong. I used to think that the DeFi network must have a basic asset, which can not only be used to issue synthetic fiat currency, but also have other valuable functions. For example, the value of Ethereum is not only on MakerDAO. Before the mechanism of pledged ETH to generate DAI appeared, Ethereum had valuable functions. I originally thought that this model was immutable. So far Synthetix has proven my point is wrong. For me, the remaining question is: if the price of the SNX token itself will not skyrocket, how large will it be.

Why Synthetix is so important

Synthetic tools will become the ladder to the future of DeFi and to achieve the popularity of DeFi. According to the current situation, stablecoins are one of the use cases that have adapted to the market, but to compete with traditional banks (or attract traditional banking funds), the ecosystem needs to build more complex financial products. Such financial products will involve foreign currencies, equity instruments, put / call options, futures and, ideally, insurance. Synthesis tools lay the foundation for today's increasingly complex DeFi ecosystem. In a previous article, I explored how banks can attract deposits and earn interest in a gig economy. By introducing synthetic tools into the product mix, individuals can “buy” physical commodities such as gold or go long / short Tesla and other companies' stocks. Can synthetic instruments compete with products offered by traditional financial technology? Maybe not. But these two are like Netflix running on a broadband cat with a speed of 256 kbps, and HBO running on a wired network in the early 21st century. We all know what has happened in the past 20 years.

Note: As of the writing of this article, SNX is mainly trading on decentralized exchanges, and a large amount of liquidity is mainly concentrated on a few off-market platforms. In terms of "degree of decentralization", this situation does constitute a risk. Having said that, this project is able to drive a network, avoid centralized exchanges, and guide the most liquid tokens on Uniswap, which have impressed us. As adoption rates increase, there are interesting signs for the future of the exchange. We will continue to explore upcoming contract transactions and crowdsourcing liquidity pools. (Finish)

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Perfecting Blockchain Cognition with Bitcoin's Middle Tier Knowledge

- Dry goods | Three technical analysis methods to play the Bitcoin market cycle

- Babbitt Column | Regulatory Sandbox Confirms Difficulties in Implementation, China Should Actively Deploy Industrial Sandbox

- Will the date of CME's launch of Bitcoin options be the end of altcoins?

- Analysis of Singapore's Payment Services Act: What is the difference between the regulatory policies imposed on different types of digital currencies

- EOSIO 2.0 is officially released, solving the biggest bottleneck of blockchain development, making EOS "faster, easier and more secure"

- 2020 Investor's Congress discussion: Market fluctuations, how to predict capital?