Research Report | The Innovative Path for Institutional Investors – How to Participate and Invest in Blockchain Assets

The authors:

Yuan Jin Institute Jiang Jinze

Distributed capital Jiang Xin

consultant:

- In the five directions of the Central Political Bureau's application of blockchain chain, which companies are doing?

- 70% of ETH holders are losing money, and the road to returning is long. Will you insist on seeing more?

- Viewpoints | How to make a choice for blockchain investment on the new road of change?

Distributed Capital Shen Bo, Sun Ming, Yu Wenbo, Yao Jingyi

If you need cooperation, please contact the author.

(E-mail: [email protected], WeChat: 439902916)

Summary:

1. Under the background of the three phases of the macro environment entering long-term low interest rates, low economic growth, and high uncertainty, high-quality assets are crowded and scarce. The rise of the new blockchain digital assets represented by Bitcoin has brought new ideas to the traditional combination configuration.

2. The value capture scenarios of digital assets can be divided into: value storage, practical value, trading medium, and speculative value.

3. A survey of 150 universities in Europe and the United States showed that 94% of respondents had configured encrypted digital currency related assets. University endowment funds have been actively deployed as an alternative to encrypting digital currencies.

4. Bitcoin returns are highly correlated with mainstream asset classes, whether in long or short periods. And its yield distribution is positive and "fat right tail", showing a very high return-risk ratio.

5. Based on Markowitz's modern portfolio theory, adding Bitcoin to a traditional portfolio can not only maximize returns within a given range of volatility, but also minimize risk given the expected return target.

6. The proceeds from investing in digital assets are not only derived from “capital gains” but also “interest income” and “reinvested income”.

7. For institutional investors, there are other indirect methods for digital asset position allocation, such as investing in digital asset mining, investing in digital asset derivatives, and investing in blockchain company equity.

table of Contents

1. Classification of digital assets and sources of ultimate value

2. Using encrypted digital currency as an alternative asset

3. Verify the statistical characteristics of the bitcoin's rate of return

4. Adding bitcoin to the historical backtest of the portfolio

5. Looking for the "golden ratio" of digital asset allocation

6. Sources of income other than capital gains

7. The correct way to open the door to digital assets

The application of blockchain technology has been extended to digital finance, Internet of Things, intelligent manufacturing, supply chain management, digital asset trading and other fields.

The blockchain network has changed the traditional production and accounting links. The digital assets in the chain and the blockchain network are symbiotic. In many application scenarios, the whole blockchain ecosystem is circulating blood, carrying value circulation and incentives. The important function of this paper is to start with the analysis of the characteristics of digital assets based on bitcoin, and answer the following questions from the perspective of institutional investors' asset allocation.

● What is the usage scenario?

● Where does the value capture come from?

● What is the meaning of configuration in a complex portfolio?

● How should the organization enter the market in the current regulatory environment?

In particular, as the global economy enters a slow growth cycle, the consensus is getting stronger and stronger. Low interest rates and even negative interest rates are coming back or becoming the norm. Political uncertainties in developed regions such as the United States and Europe are rising, accompanied by high crowding and scarcity of high-quality assets. Traditional investment Managers face unprecedented pressures and challenges.

The last global economic recession occurred 11 years ago, and the crisis originated from the systematic collapse of the financial system. Accompanied by the collapse of the old financial order. A bitcoin of emerging assets created by non-financial institutions was born. The market value of development in more than ten years has exceeded 140 billion US dollars (October 2019), roughly equivalent to the GDP of Kuwait, Hungary, Ukraine and other countries. It has become a kind of With the emerging market assets with considerable market depth and consensus, understanding the characteristics of "bitcoin" will become a compulsory course for asset managers.

This paper demonstrates that the correlation between Bitcoin and traditional large-scale assets is extremely low, and the return-risk ratio is almost the same as the asset category, which provides a rare opportunity for portfolio diversification.

1. Classification of digital assets and sources of ultimate value

There is no definition of a unified authority on the classification of digital assets. There are many disputes among regulators, academics, and practitioners. For example, many practitioners believe that Bitcoin or Monroe can be used as currency, but the supervision of major countries. Almost no one admits this. Or whether some of the utility tokens are securities, the debate between the regulators and the project side has never stopped. Regardless of how the specific cases should be classified and integrated, the main categorical attributes at present include:

● Private currency, a transaction intermediary that has no sovereign endorsement but mutual recognition by counterparties

● A unit of account that can be used to measure the value of a good or service

● Virtual assets /commodities, a digital resource that can be measured by legal currency and expected to bring economic benefits or economic utility, can be used as value storage

● Securities-type tokens, the essence of which is the electronic proof of securities , which can be stocks or debts.

If the classification of digital assets is mainly the issue of regulatory rules or academic issues, but more importantly, the inability to clearly observe and measure the value capture of digital assets is the main reason why many institutional investors are discouraged in this field.

This is not surprising. Even though the first modern stock was born in 1602, the widely accepted and uncomplicated cash flow discounted (DCF) valuation method was widely used after the 1960s. use.

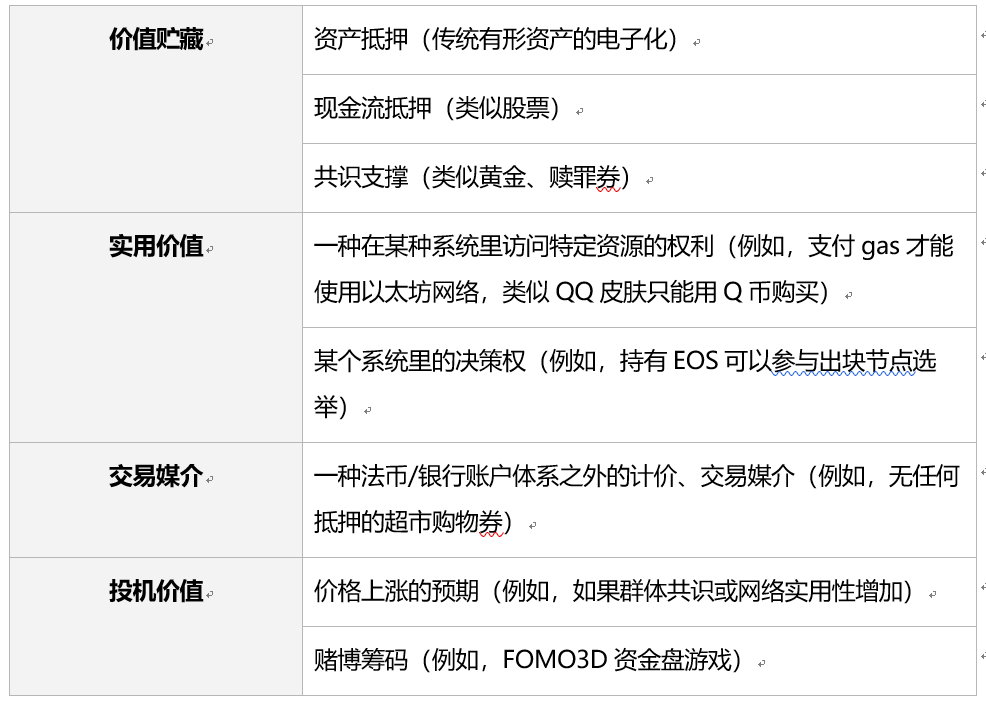

Given that many digital assets have multiple attributes, traditional valuation methods are difficult to apply. We can conclude that the core value capture of digital assets has the following four categories: eight sources:

Table 1: Classification of source values of digital assets

Either of these approaches can meet specific needs and create value, giving the ultimate source of value for digital assets/virtual currencies/digital passes.

In the store of value classification, the essence of digital assets of asset collateral and cash flow collateral is the digitization of traditional debt and equity assets. The valuation can be slightly modified in the corresponding traditional valuation model:

- Increase premium: Blockchain technology can bring advantages over traditional assets, including reducing the risk of counterparty in asset delivery and reducing the premium brought by financial settlement costs;

- Less discount: The increased risk of blockchain technology, such as the security of smart contracts, special attack methods (such as 51% attacks) and other discounts.

In addition, there are cases in which the cost of assets is used to value digital assets, similar to the valuation reference method often used in commodities such as crude oil and gold. However, the problem is that the cost of a lot of proof ( PoW) digital currency is with the participants. Cost changes are difficult to have long-term reference meanings when they change dynamically.

For the Utility value part, one method that can be used for reference is the theory of quantity of money, namely:

Total economic utility of a blockchain network = price level * quantity of service total = token price * token circulation * token flow rate (number of times of being changed in one year)

The transformation equation can be obtained:

Token price = total network economic utility / (token circulation * token flow rate)

The theoretical valuation method of money quantity is currently more acceptable to the market, but the core problem of this valuation method is that we must first estimate the economic value of the total utility of the network (relative analogy) and calculate the relatively accurate token. The flow rate may have a large error with the actual situation of the network, and may need to be corrected by other absolute estimation methods (such as NVT and its variants, Metcalfe network value method).

For the value of the Medium of Exchange, an analogous valuation method can be used, such as assuming or counting how many transfers or trades in the world use digital currency, and then pushing back the demand.

The pricing of digital assets under the category of speculative value is more complicated. It is analyzed on the assumptions of rational investors, or from the perspective of behavioral finance. There has never been a unified voice in traditional financial markets.

The specific valuation method is not the focus of this report, and like the traditional financial market, some parameters taken when calculating the asset price are largely based on the expected assumptions for the future. We will only give two specific examples in this report. The case is to intuitively feel why the value of digital assets is not just a “consensus” that cannot be seen or touched , but a real “money”.

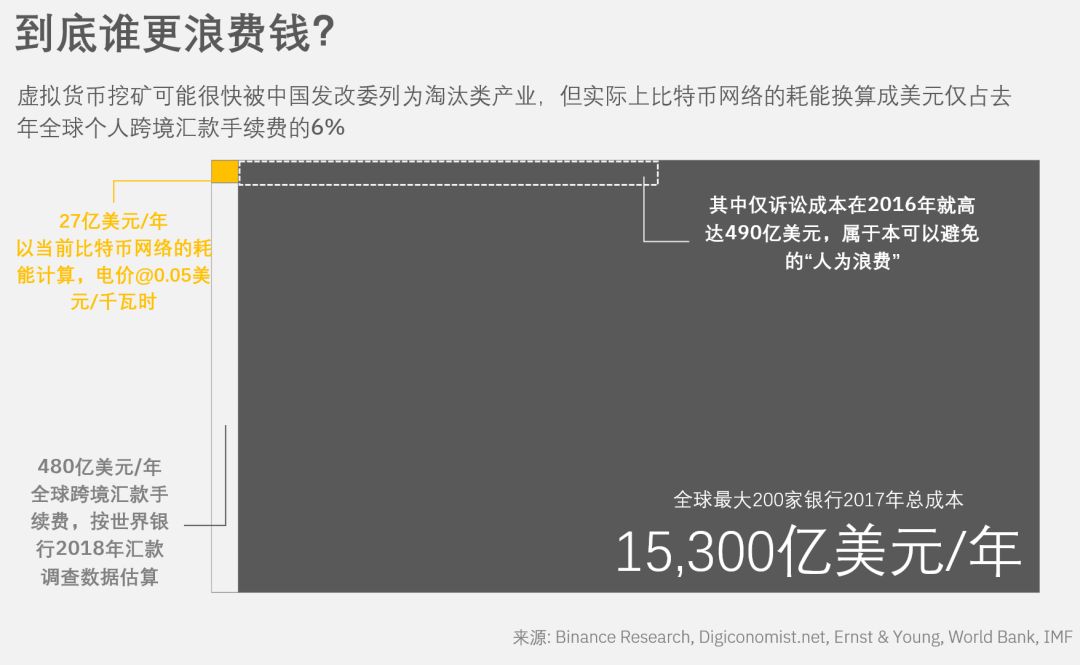

Case 1: Value capture as a trading medium

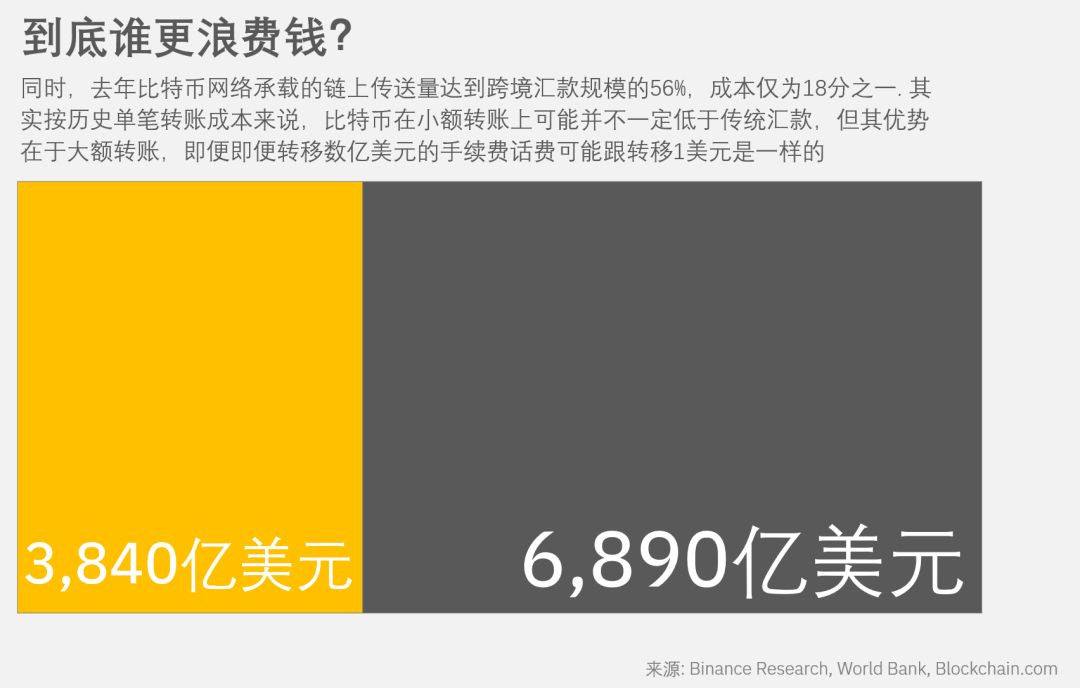

In 2018, the Bitcoin network carried a $348 billion chain transfer. The World Bank estimates that the total amount of global cross-border remittances in 2018 was $689 billion. Correspondingly, in order to maintain the operation of the Bitcoin network, the mining power consumption in 2018 is about 2.7 billion US dollars, and the global cross-border transfer fee is 48 billion US dollars.

That is, the Bitcoin network uses only one-eighth of the cost, carrying 56% of the global cross-border remittance volume, reducing costs, improving efficiency, and creating value. The same logic can be extended to other blockchain networks, such as Ethereum, Bitcoin cash or stellar coins, whose network maintenance costs will be lower than Bitcoin, possibly only tens or even tens of thousands.

Above we briefly explore the ultimate source of value for most digital assets/digital currencies. Based on this value, we will analyze why financial institutions should allocate encrypted digital assets from the perspective of financial market investment practices.

2. Using encrypted digital currency as an alternative asset

2.1 Definition

Alternative Investment refers to the type of investment other than stocks, fixed income or currencies traded on the traditional open market.

“Alternative” is a neutral term that simply distinguishes it from traditional assets such as stocks and bonds. Real estate and commodities, even art, are so-called "alternative investments."

As with traditional investments, alternative investments should provide a reasonable return at an acceptable level of risk.

A common example is gold. Since the Bretton Woods system was decoupled from the US dollar half a century ago, gold has little practical use except as an ornament and a few industrial scenes. But this does not prevent gold from being an asset allocation.

2.2 Advantages of alternative assets

Because alternative assets are less relevant to traditional portfolio investment products, investors can diversify their investment risks through alternative assets.

Scientifically increasing the allocation of alternative assets can cope with the impact of low interest rates or high volatility environments (if a crisis) that we may face for a long time now and in the future, and it is possible to obtain higher returns than traditional stock and bond portfolios.

2.3 Famous case

The Yale Endowment Fund, which is nearly $30 billion in size, is a household name in the world of alternative investments. In the past ten years, the fund's average annual return rate was 7.4%, much higher than the average return rate of 5.5% of university pension funds, and also higher than the average return rate of global hedge funds in the same period of HFR statistics of 3.38%.

According to public data , nearly 60% of the fund 's assets in FY 2019 were invested in alternative investments such as venture capital, hedge funds and leveraged buyouts.

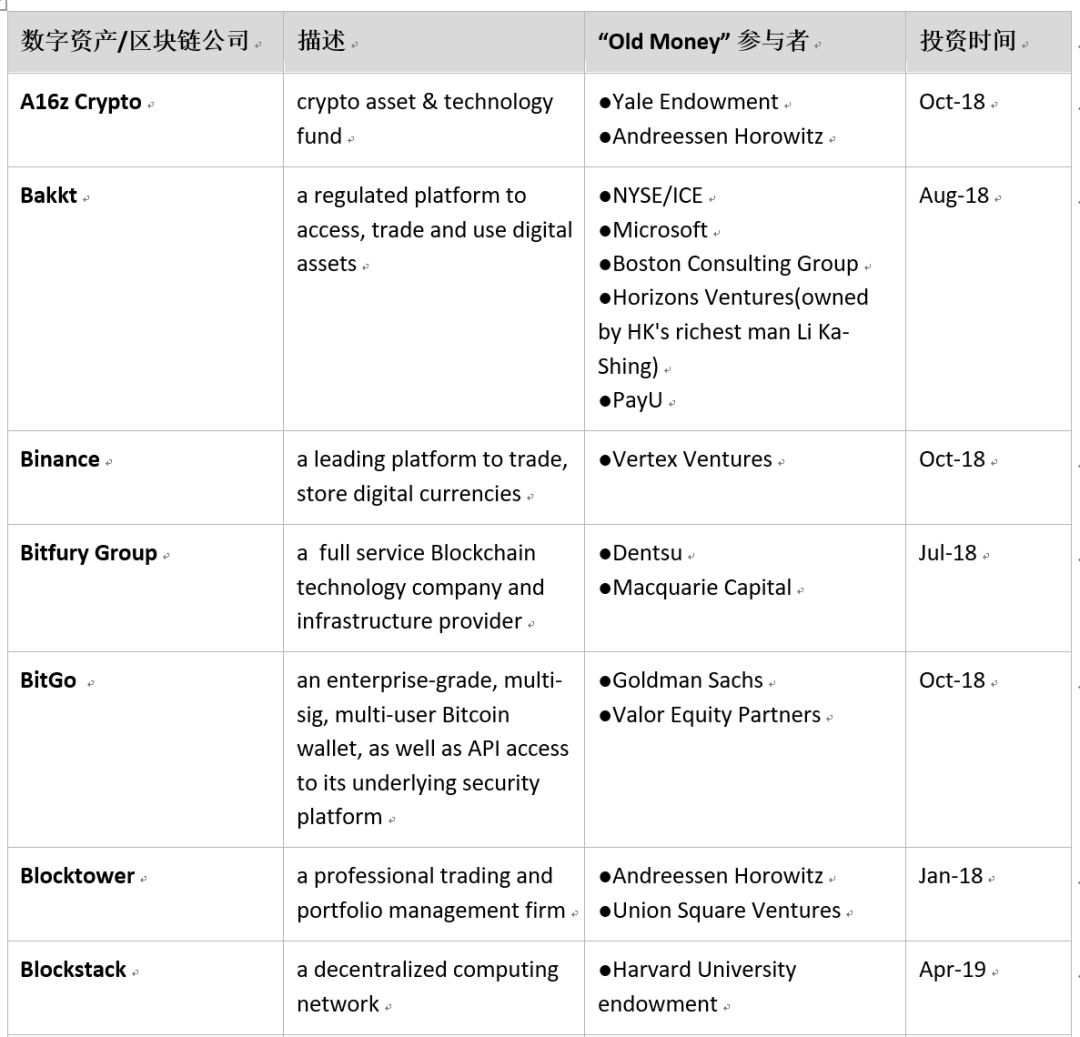

A high proportion of alternative configurations clearly contributes to its superior performance. Last year, Yale Endowment invested in A16z and became the first “Ivy League University” to enter the field of encrypted digital assets, which led to extensive discussions and then reinvested in the digital asset fund Paradigm.

As the mentor and leader of Gao Lei Capital Zhang Lei, David.F. Swensen, chief investment officer of Yale Endowment Fund, described the proceeds of decentralized investment as “free lunch” in his book. In an interview with CNBC in 2018, they bluntly received a gift from the emerging alternative asset “Free Lunch” in the form of an investment fund.

Figure 1: American university endowment fund alternative asset ratio is positively correlated with rate of return

Source: Frontier Investment Management

The Yale Endowment Fund is just one of many university donation funds that love to try something new. According to a joint survey by Global Custodian and TheTRADE Crypto, as of the fourth quarter of 2018, 94% of the 150 university funds surveyed conducted cryptocurrency-related investments in 2018. 54% of the universities directly invested in cryptocurrencies (through exchanges and OTC, etc.), and 46% invested through investment funds.

This result is very consistent with the characteristics of university endowment funds that are generally keen to actively deploy high-risk alternative assets. Of course, due to the fact that there is almost no LP redemption pressure in university endowments, this also leads to the fund's daring to hold low liquidity and high risk. One of the reasons for the asset.

Table 2: "old money" encryption investment 2018-19

3. Verify the statistical characteristics of the bitcoin's rate of return

– Before deciding how to invest, you need to understand the statistical characteristics of the return on digital assets.

3.1 Cross-asset correlation test – "maverick"

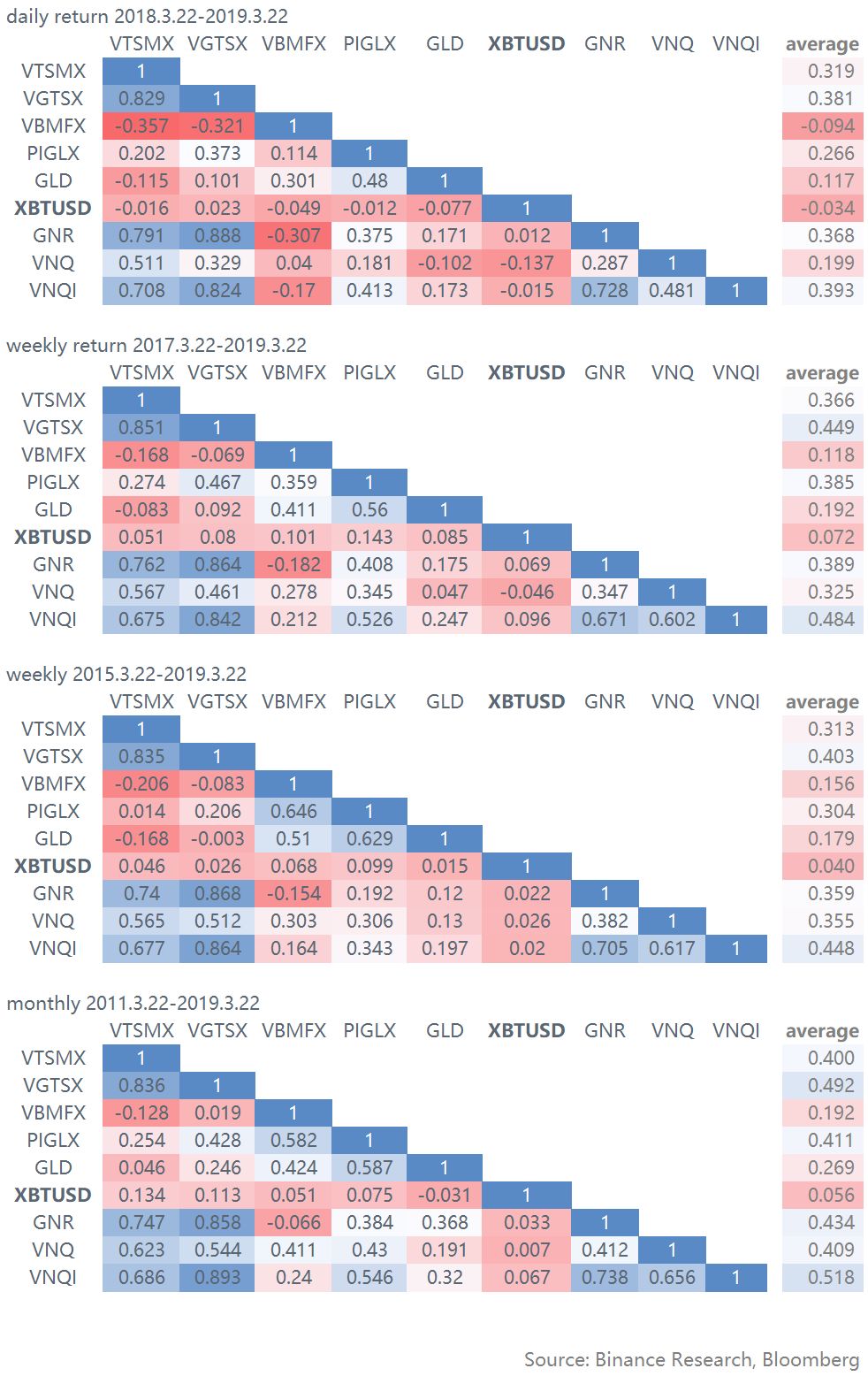

In order to ensure the long-term profitability of the portfolio, the portfolio configuration of asset management institutions is often diverse, from the perspective of cross-asset correlation, as seen in Figure 2 and Table 3 below, whether in long-term or short-cycle Within, the correlation between Bitcoin's return and mainstream major assets is extremely low (the absolute value of correlation is the lowest, meaning there is no obvious positive correlation or significant negative correlation). The reference objects we selected include US stock market, global stock market, and the United States. Bonds, international bonds, gold, US real estate, international real estate, natural resources.

In fact, due to the integration of global economic activities and the interdiction and mutual influence of international financial activities, the linkage of large-scale assets has become extremely fast and close, and the “maverick” assets like Bitcoin are actually quite scarce. This means that Bitcoin can play an active role in dispersing systemic risks in traditional financial markets.

Table 3: Cross-asset 2011-2019 Weekly/Monthly Yield Correlation Matrix

Source: Coin Research Institute, Distributed Capital, Bloomberg

3.2 Volatility test – the volatility has dropped significantly since 2014

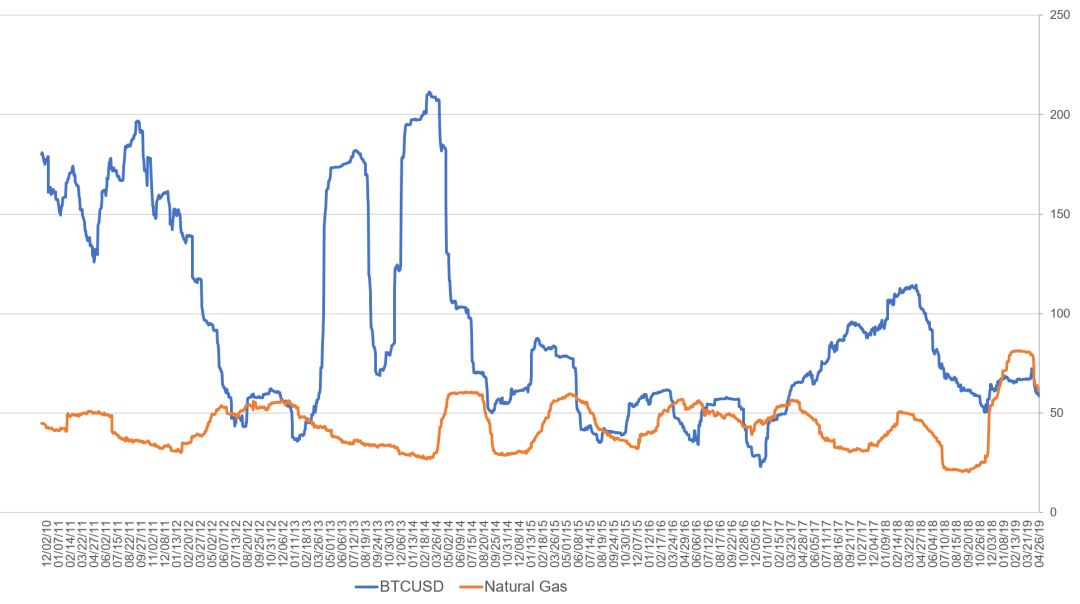

It is true that bitcoin is a highly volatile asset, but this does not mean that the volatility of traditional assets must be less than that of bitcoin.

As can be seen from the figure below, the annualized volatility of traditional assets and bitcoin is compared. Bitcoin's volatility is close to that of natural gas, and even lower than some stocks and currencies in emerging markets.

In fact, since 2014, the median volatility of Bitcoin has dropped significantly, reducing the risk of bitcoin configuration.

Figure 2: Trends in Bitcoin and Natural Gas Annualized Volatility

Figure 3: Comparison of annualized volatility of bitcoin and multi-assets

Source: Coin Research Institute, Distributed Capital

3.3 Distribution characteristics of yields—spikes, fat tails, and positive deviations

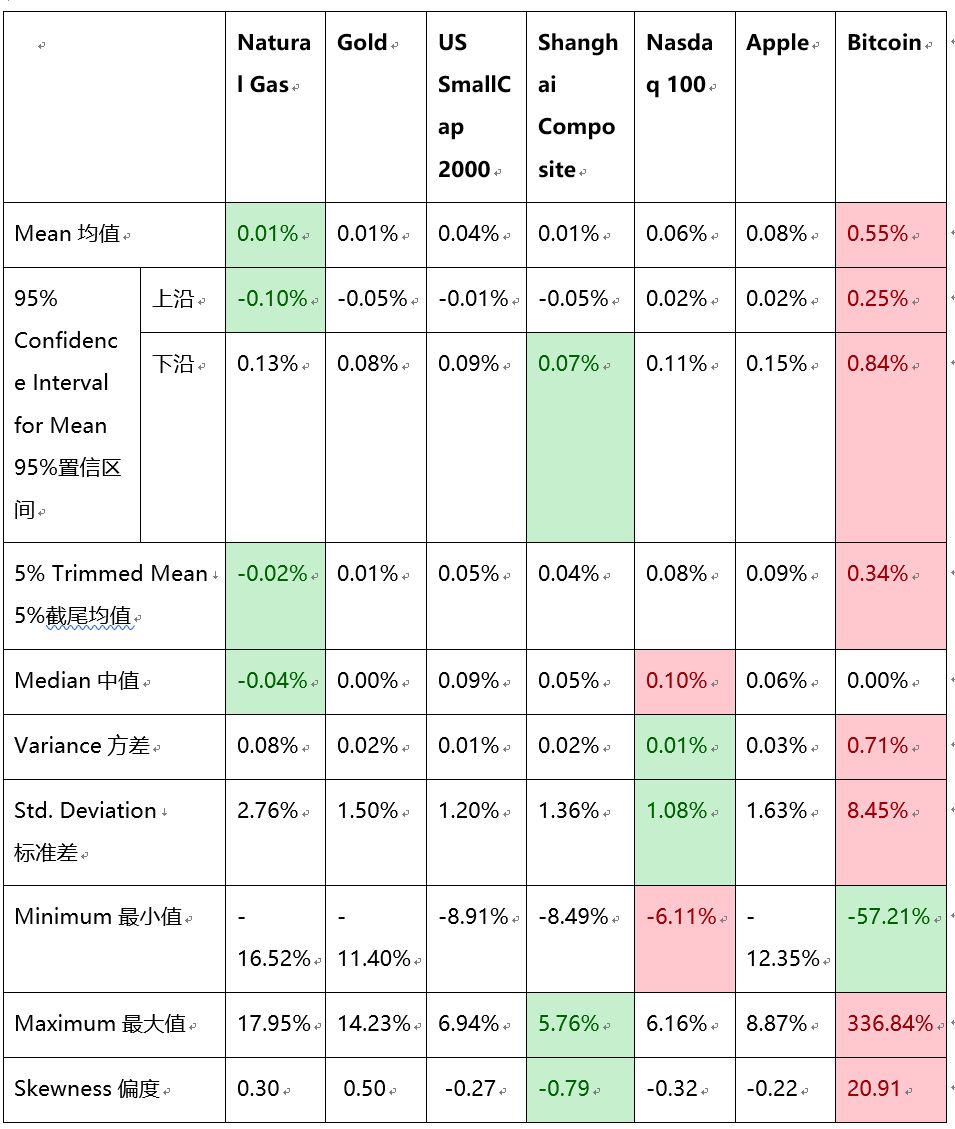

In Table 4, we selected historical average daily rate of return for several major types of assets for statistical characterization. Samples were taken from January 1, 2011 to April 26, 2019.

It can be clearly seen that Bitcoin's rate of return does not follow a normal distribution, showing the characteristics of positive skewness, fat tail, and spikes. These characteristics are similar to the stock market, but more "exaggerated" than the stock market.

Table 4: Multi-asset 2011.1.1~2019.4.26 Statistical characteristics per rate of return

Among them, “Skewness” means “skewness”, which means the deviation between the mean value of daily income and the median. The larger the number, the higher the probability of obtaining positive returns. The skewness of Bitcoin's yield is extremely high, showing the asymmetry of its yield distribution. In theory, an extremely positively biased asset like Bitcoin should be favored by investors.

In addition, "Kurtosis kurtosis" also shows that Bitcoin's yield is in the "fat spike" state, and the kurtosis is much larger than 3 (up to 488), meaning that the tail is thicker than the "normal distribution", which means that we The chances of experiencing “abnormal returns” are higher.

Investors usually avoid stocks with sharp spikes because high volatility means that investors are much more likely to experience tail risk than average returns.

It should be noted that the skewness and the characteristics of the so-called spike tails we mentioned earlier are compared with the "normal distribution" with a skewness of 0 and a kurtosis of zero. Usually in empirical analysis, the yield data is assumed to be normally distributed for ease of modeling and analysis. But in reality, the yield of few assets is in line with the normal distribution, especially the bitcoin we are discussing now.

Ignoring the tail risk under the assumption of normal distribution leads to the collapse of the Long Term Capital Management Corporation (LTCM), so it is also important to recognize that the fat tail is a risk control for the digital asset market.

However, because the tail risk of financial markets is “two-way”, for example, in a bull market, the higher the kurtosis, the greater the probability that the stock will receive a very high return. Conversely, in a bear market, the possibility of extreme losses will also increase. This may lead to inconsistent preferences of investors for kurtosis at different times.

Therefore, the good news is that although bitcoin has a high kurtosis, the yield is positively biased, that is, "fat tail" is more likely to appear in the positive income range , as shown in Figure 3, the historical yield distribution of bitcoin. It shows that although the probability of a "big fall" is higher than that of the stock market, the probability of a "big rise" is higher, and the increase is not low.

Tom Lee, founder of Fundstrate, a well-known digital currency analysis institution in the United States, has also made a similar description of these statistical characteristics of Bitcoin. The wording is more common – in most given years, most of the bitcoin price is only Appears in the ten largest trading days, and if you miss this short time, the yield will be negative.

Figure 4: Bitcoin earnings and the distribution of yields in the US and China stock markets

Source: Coin Research Institute, Distributed Capital

3.4 Sources and points of attention for peak fat tail characteristics

Edgar Peters (1991) believes that different investors react differently to market information. Although information is mostly linear to the market, different understandings of information and differences in investment time lead to information. Produce a different response, so the price does not reflect all the information at a certain moment, the price change is not independent, and the yield will also show more "spike" and "fat tail".

In other words, if the information in the market reaches each “rational person” linearly, but the investor ignores it before the trend is determined, and then reacts to all the ignored information in a cumulative manner, which may also lead to returns. The peak of the fat tail distribution. Or in another case, if the information distribution affecting the market is “spike”, then the securities returns will tend to be distributed like this. For example, the negative from the regulatory layer may appear to be in a cluster rather than linear.

In any case, the statistics in the previous section show that the flow of information in the cryptocurrency market seems to be less smooth, and investors' responses may be slower than traditional market participants, which is in line with our speculation on the structure of investors in the cryptocurrency market. Therefore, when investing in digital assets, the time period of waiting for “good fortune” or “good for cashing” may be longer than that of traditional assets, and the trading behavior of even-driven investors needs to be changed accordingly.

Figure 5: Comparison of investor structure – digital asset market (estimate) vs. stock market (data as of January 2019)

Source: Coin Institute , Cryptofundresearch.com, Bloomberg

In addition, the peak fat tail phenomenon makes a large amount of information pricing stay at the tail, and the weight of the "plain" event becomes smaller. Therefore, in asset allocation, especially in portfolios with low volatility tolerance, we should pay more attention to the disturbance of fat tail risk and the potential risk of potential duration mismatch than the traditional market .

4. Adding bitcoin to the historical backtest of the portfolio

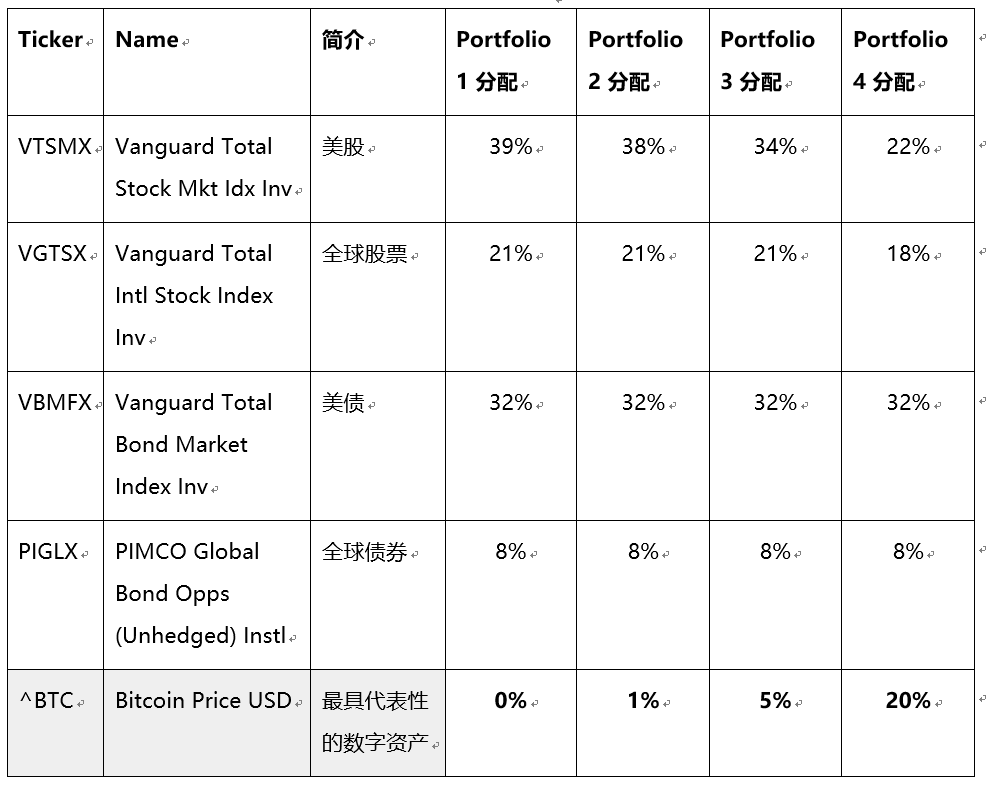

Is Bitcoin useful for portfolio management? Can it bring versatile benefits? We simulate three simple portfolios to observe.

The first is a classic 60% stock, 40% bond portfolio, the second is to add 1% bitcoin to the portfolio, the third portfolio is added to 5% of the bitcoin configuration, and the fourth is The most radical, 20% of the bitcoin in the portfolio. Intuitively, this is a combination of four risk increments.

Table 5: Simple Combination Simulation 0~20% Bitcoin Configuration Weights

The backtesting rules are as follows:

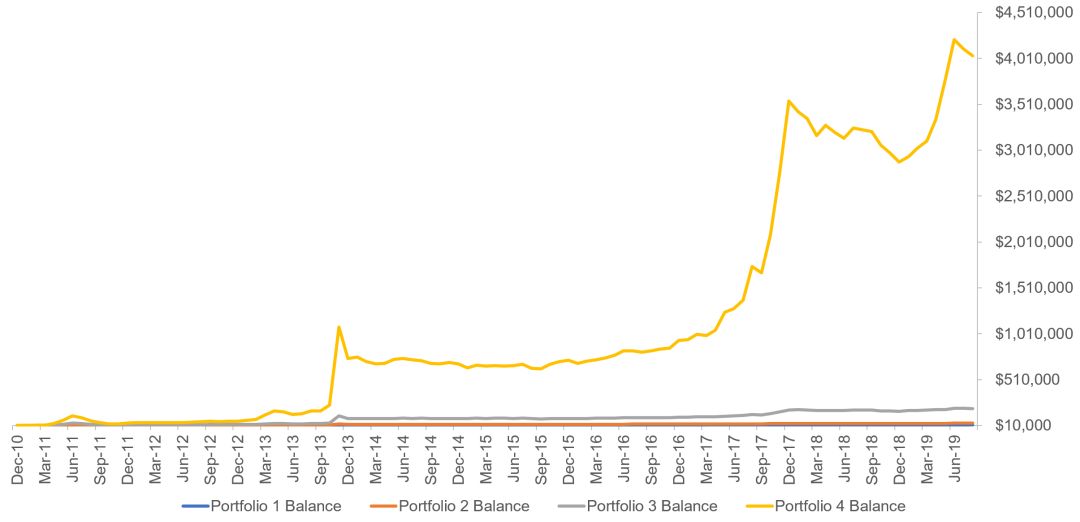

The results of the backtest are shown in the figure below. The combined asset size with only 20% bitcoin has been more than 400 times in the past 9 years, so that the net value curves of the other three combinations are not visible in the logarithmic coordinates.

Figure 6: Simple analog bitcoin weight 0~20% combined net change

Source: Coin Research Institute, Distributed Capital

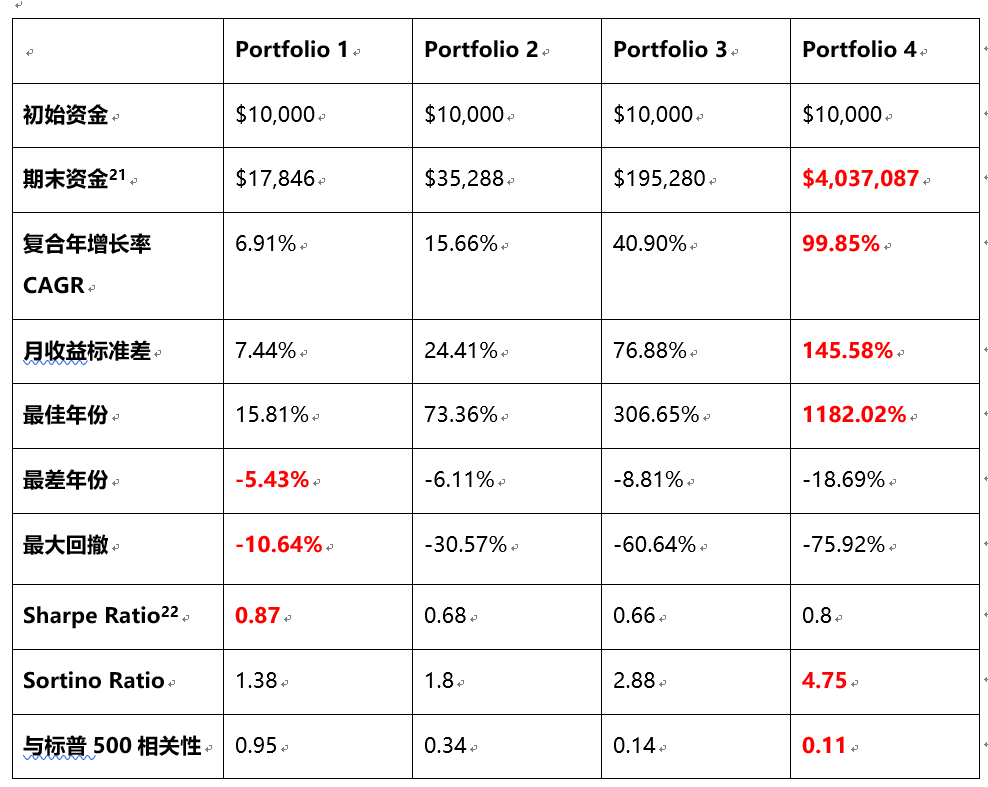

Table 6: Simple analog Bitcoin weight 0~20% combined back test result statistics (optimal result red bold display)

As can be seen from the statistical summary in Table 6, the combination of 20% bitcoin is configured with a compound annual growth rate of nearly 100% over the past 9 years. Even with only 1% of Bitcoin, the final balance of the portfolio is twice that of the traditional 60/40 portfolio.

However, just looking at the final net worth is not enough. As can be seen from Table 6, although the bitcoin portfolio has higher returns, the volatility has increased accordingly. See the Standard Deviation column, which describes the dispersion of monthly returns for several different portfolios.

Table 6 also contains several important pieces of information, including:

● Even with only 1% of Bitcoin, the monthly standard deviation of “Portfolio 2” has reached 24.41%, which is about 2 times that of the S&P 500 Index ETF. Conversely, although the 60/40 portfolio has the lowest return, it has the lowest volatility.

● Observe that the “maximum retracement” sub-item shows that the maximum retracement of the 60/40 combination is only 10.64%. In portfolio 4 (Portfolio 4), because of 20% bitcoin, its biggest monthly decline is close to 76%, which may be unacceptable to many people in real life.

● Of course, don't forget the two most important indicators – the Sharpe Ratio and the Sortino Ratio – which are classic indicators of risk-adjusted return on investment. The Sharpe ratio uses total volatility, while the Sortino ratio uses only volatility in the downside, which is more suitable for evaluating a more volatile portfolio. The higher the two indicators, the better.

It can be seen that due to the high overall volatility, the Sharpe ratio of a portfolio containing a small amount of Bitcoin is not as good as the US Single Index (SP500).

However, the Sortino ratio only calculates the ratio of downside risk to return. The higher the bitcoin portfolio, the higher the score, indicating that the risk of holding one bit of bitcoin for each unit can be more than one unit of compensation.

In summary, the addition of Bitcoin to the traditional 60/40 portfolio over the past eight years has the potential to significantly increase returns and risk-return rates. And Bitcoin's low correlation with major assets helps to spread the risks of traditional markets. In addition, historical tests have shown that bitcoin allocation can lead to extreme fluctuations in the portfolio, but because of the higher risk compensation, such fluctuations are “healthy”, or we can say that bitcoin yields are “asymmetric”.

In the next chapter, we will explore what proportion of bitcoin configuration will optimize a multi-asset portfolio.

5. Looking for the "golden ratio" of digital asset allocation

– Maybe there is no ultimate "optimal configuration" ratio, but we can optimize the portfolio through Bitcoin under specific target constraints.

Historical relevance tests have shown that Bitcoin is the vane of all digital assets, and this will not change in the foreseeable future. So to simplify the test method, we will use Bitcoin as the sole target of digital assets in the following asset configuration tests. In order to find the “golden ratio” of Bitcoin configuration, the concept of “Efficient Frontier” proposed by Markowitz (1952) will be introduced here, which lays the foundation for modern portfolio theory.

The theory holds that investors will make a balanced choice between expected returns and risks, while the combination on the “effective frontier” is the optimal portfolio of returns and risks.

Here, we will skip a detailed introduction to Markowitz or the Capital Asset Pricing Model (CAPM), using his theory directly to guide calculations and present results.

5.1 Understanding how gold improves a portfolio

To better understand the nature of Bitcoin, let us first look at how traditional portfolios use gold to optimize their risk-return ratios.

As above, we assume a simple “basic combination” of traditional 60/40 stock and bond investments as follows:

Then, we add the world's largest gold ETF, GDR (SPDR Gold Shares), as an alternative asset to the asset pool (not necessarily added to the portfolio). The sample test period is set from 2005 to 2019, and the initial capital is $10,000. The configuration with the highest Sharpe ratio is:

Since the risk-reward ratios of Vanguard Total International Stock Index Fund Investor Shares and PIMCO Global Bond Opportunities Fund (unhehedge) Institutional Class are not good enough, there will be no such securities in the “Highest Sharp Ratio Combination”, but the gold allocation ratio is 2.47%. So, what changes have gold brought to the portfolio? Please see the picture below:

Table 7: 2005~2019 performance of the basic combination and gold optimized combination (optimal result red bold display)

Table 7 shows that although the traditional 60/40 combination of the ending income and the compound annual growth rate is higher than the maximum Sharp rate combination, in fact, the basic portfolio can only obtain a return of 0.51 units for each unit of fluctuation risk , and add gold. After the ratio has been optimized by the maximum Sharpe rate target, the Sharpe rate has risen sharply to 1.07, meaning that a 1.07 unit return can be obtained for each unit of fluctuation risk. At the same time, the Sortino Ratio doubled from 0.86 to 1.78, indicating that the combination of gold has a higher compensation for downside risks.

5.2 Simply adding Bitcoin is of little significance

– optimal configuration needs to be established under constraints

Let us first look at two charts called “efficiency frontiers”. Figure 5 is a traditional portfolio of gold and the above four securities assets. Figure 6 contains all the assets in Figure 5 and bitcoin.

The abscissa axis is the standard deviation of the monthly yield of each asset, that is, the volatility, and the ordinate axis is the expected rate of return of each asset. The blue dotted curve is the “efficiency frontier”, which is the “boundary” of all possible combinations of the assets provided.

We tested in Section 4.2 that the “highest Sharpe ratio” portfolio that can be constructed from an asset pool containing gold and four securities assets includes 13.41% of global stocks, 84.11% of US bonds, and 2.47% of gold.

In fact, this "highest Sharpe ratio" combination is the straight line with the smallest slope in the coordinate system after it is connected to the risk-free rate. Because the slope of the line where the combination is located is smaller, the ratio of expected return/volatility is larger, which is the Sharpe rate. The bigger.

So as long as you find the risk-free rate (1 month US bond yield average, annualized 1.27%) and the efficiency cut-off curve, the "cut point" is the maximum Sharp rate combination. And we started the default 60/40 combination (provided portfolio in the figure below) with a Sharp rate of only 0.58, which is an "inefficient combination."

Figure 7: The “efficiency frontier” of a set of traditional assets

Source: Coin Research Institute, Distributed Capital

But as you can see from Figure 6 below, once Bitcoin is added to the pool of alternative assets, we can't find the so-called “tangential portfolio” because Bitcoin's historical volatility and rate of return are very high (3.26), we only There are two situations:

● You should not hold any bitcoin in the pursuit of the lowest risk configuration method

● Under the highest return or highest risk return rate, you should be 100% bitcoin

Figure 8: The “efficiency frontier” of a set of traditional assets + bitcoin

Source: Coin Research Institute, Distributed Capital

As shown in Figure 6, Bitcoin's historical average monthly rate of return from 2011 to 2019 is 708% annualized, with a volatility of 224%. Its Sharpe ratio is much higher than that of traditional assets reaching 3.16 (708%/224%), leading to tradition. Assets can only "collapse" in the lower left corner of the above coordinate system.

Table 8: Multi-asset risk return indicator statistics (2011/1~2019/9)

Figure 9: Sharpe Ratio and Sortino Ratio for Bitcoin and a set of traditional assets during 2015.1-2019.9

Source: Coin Research Institute, Distributed Capital

As you can see in Figure 7, the risk-to-reward ratio of Bitcoin has been comparable to that of Amazon.com in the past five years, far better than other major assets. But in any case, the simple conclusion of "Stud or not touch" is meaningless. In investment practice, most assets are unlikely to go 100% to configure digital assets, just as everyone understands the expected return on stocks. High, then we should 100% configure stocks or even leverage stocks?

So the combination we should look for should be the most "effective" balance between risk and return. A pre-variable that should be added here should be :

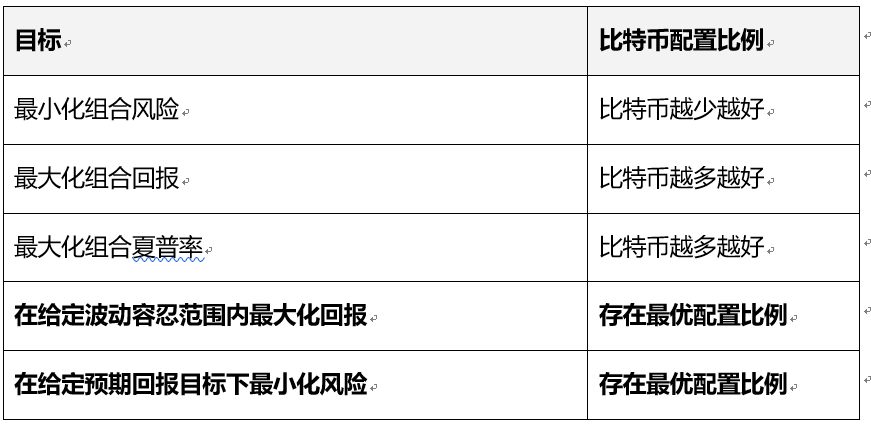

● How much risk are you willing to take? Based on this goal, we can calculate the bitcoin configuration ratio that maximizes the combined return under a given risk expectation.

● Or, what is the target rate of return you want to achieve? Based on this, we can calculate the bitcoin configuration ratio that minimizes the combined risk for a given expected return.

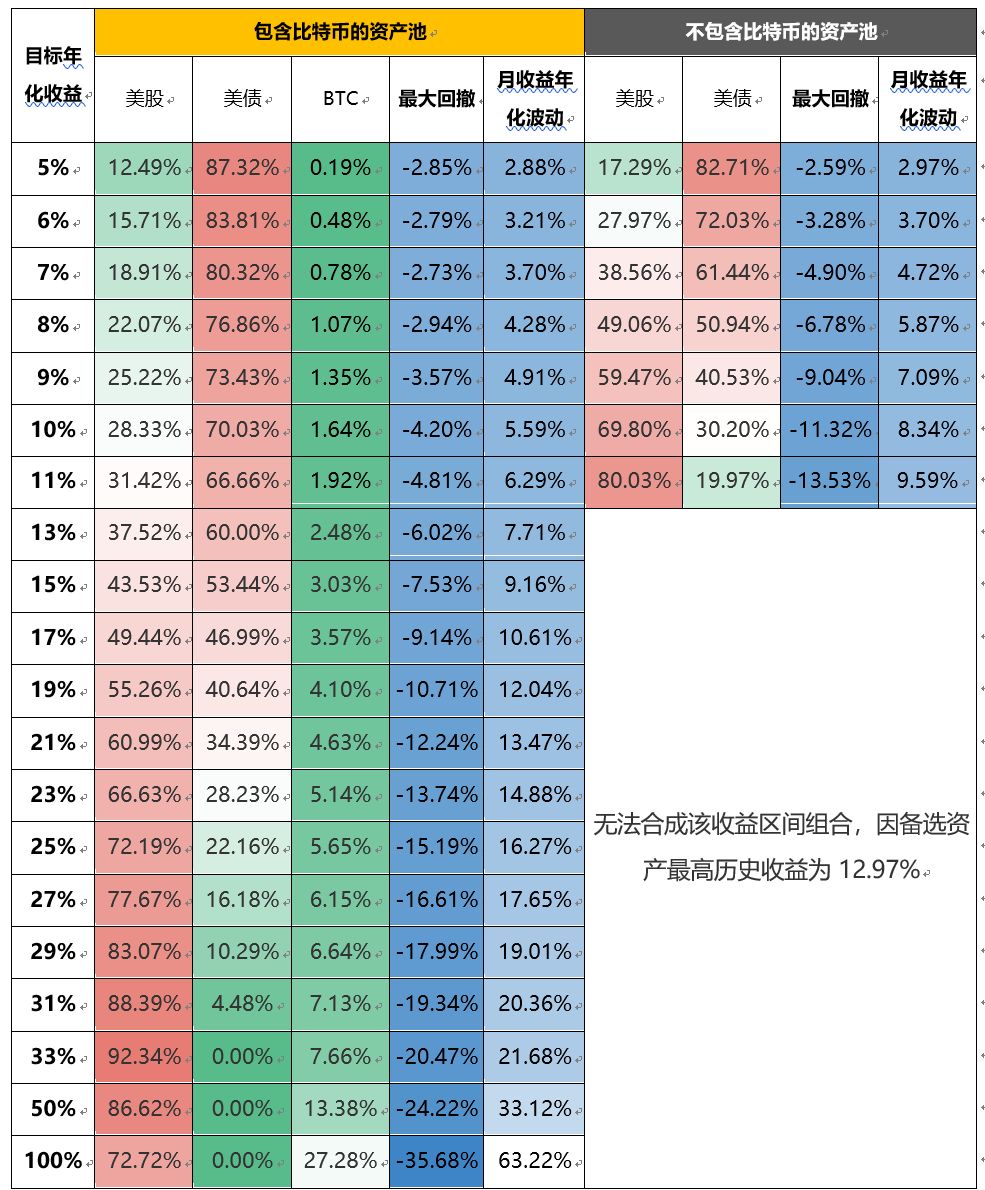

Table 9: Bitcoin configuration ratios for specific targets

5.3 Maximize combined returns within a given range of wave tolerance

— Bitcoin can increase the benefits of conservative portfolios without increasing risk

This applies to conservative funds seeking relatively stable returns, which are unable to accept large fluctuations in portfolio value, and some even write legal provisions on products.

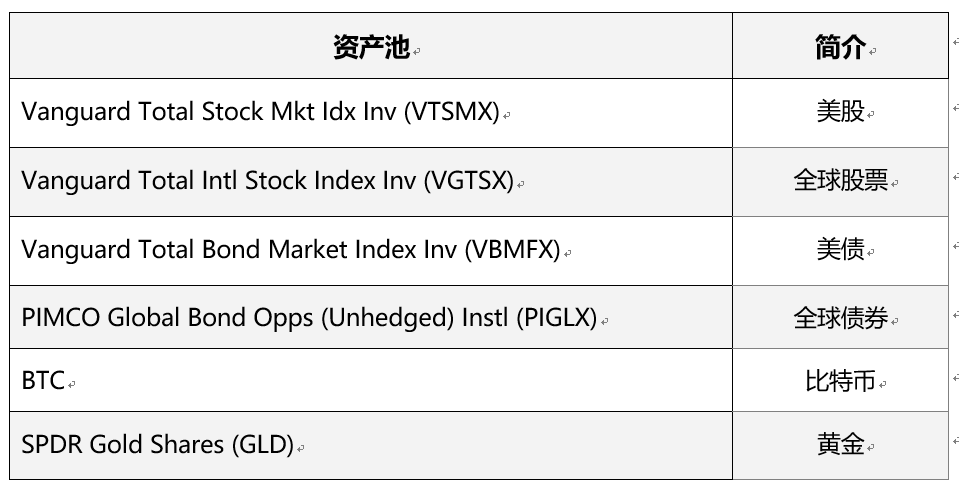

To facilitate the backtesting, we continue to assume that the asset pool includes only five ETFs in the display, including US stocks, US bonds, global stocks, global bonds, gold, and bitcoin, cash. Then based on the given volatility, we calculate a list of simulation results for a maximum benefit allocation ratio.

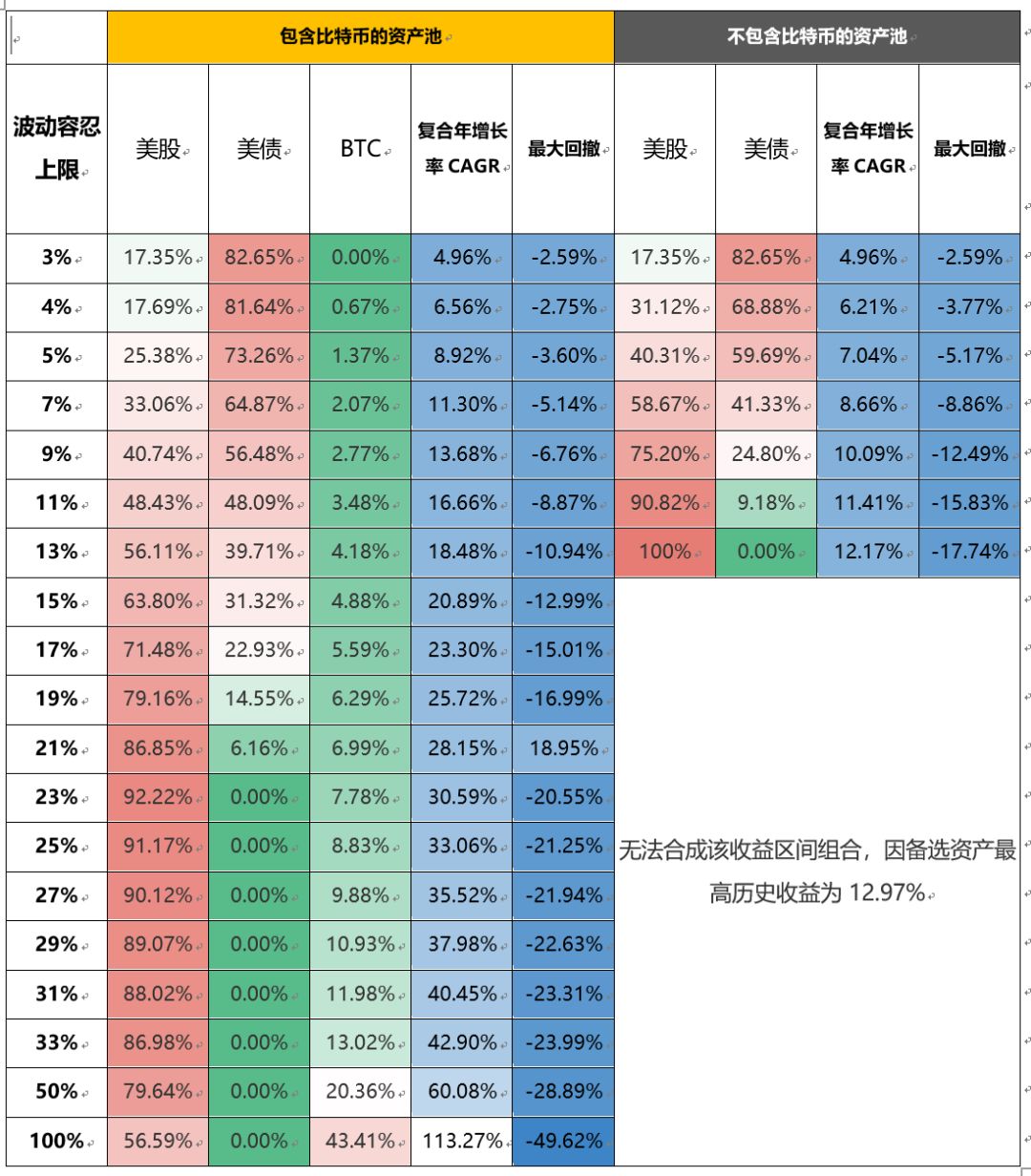

Table 10: List of optimal income allocation ratios under different wave tolerance objectives

Figure 10: Comparison of retracement and volatility with BTC combination versus BTC-free combination, under optimal risk allocation for a given target return

Source: Coin Research Institute, Distributed Capital

It can be seen from Table 10 that with the increase in risk appetite (the top left column is from top to bottom), in order to obtain the highest return, the allocation of traditional portfolios to traditional low-risk bonds is rapidly declining. But even if the target annualized volatility is only 5% or lower (meaning that risk appetite is extremely conservative), it is still a good choice to allocate about 1% of Bitcoin.

However, when the volatility tolerance falls below 3.5%, Bitcoin cannot be adopted by the combination due to higher fluctuations.

In addition, under the selected test period (2011-2019) and target volatility, there is no gold in the optimal configuration, which shows that many people's intuition that the "low risk preference combination needs to allocate gold" experience may not be correct. . The same optimal portfolio does not include global stocks and global bonds, indicating that the risk-to-reward ratio of these two types of assets has been poor over the past nine years.

5.4 Find the combination of minimum volatility given the expected return – Bitcoin can reduce the risk of combination

Next, we conduct another backtest to find the minimum volatility portfolio under the given expected return. Funds based on this type of allocation generally have clearer expectations for future expenditures and redemptions, such as insurance and fixed income. fund.

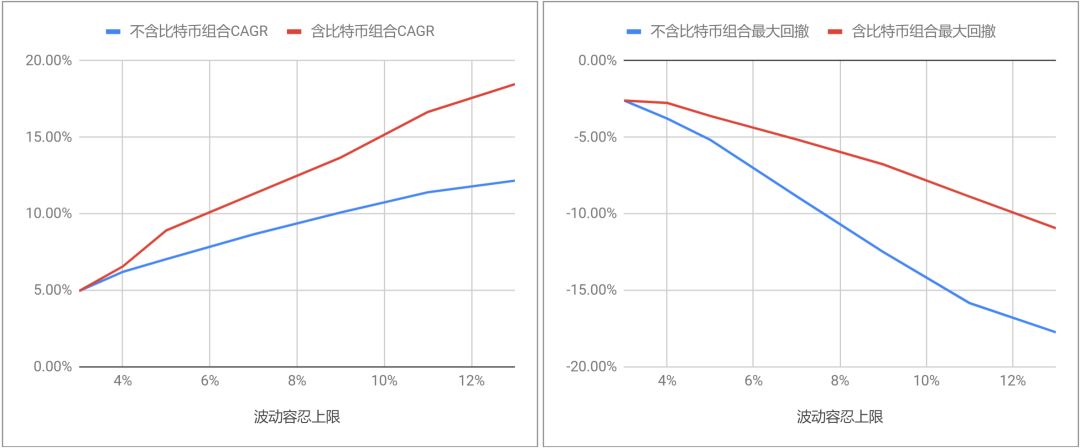

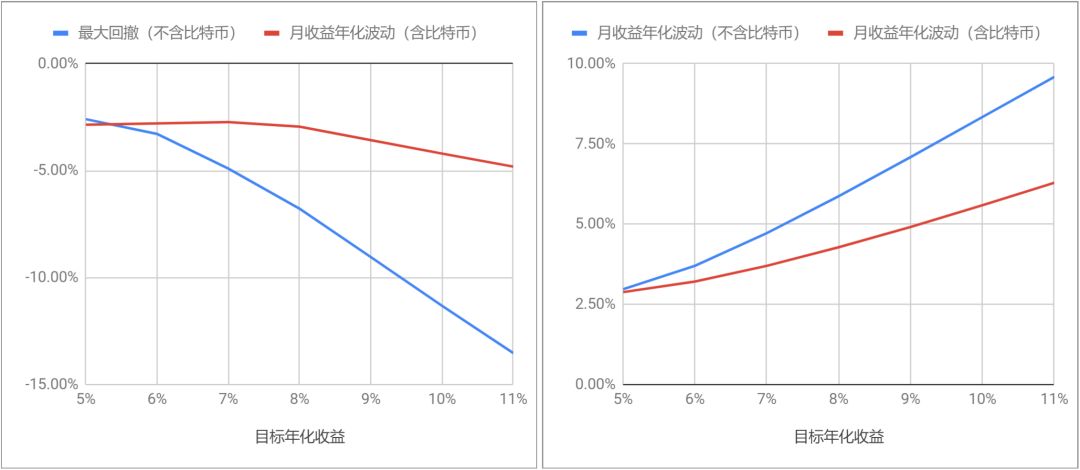

The results are shown in the table below. It can be seen that if we want to get an annualized rate of return of about 5-12% (reasonably expected), proper allocation of bitcoin can reduce the volatility of the portfolio. At all given expected returns, a small bitcoin portfolio has lower volatility and a smaller retracement than an "optimal portfolio" that only includes traditional assets:

Table 11: List of optimal fluctuation allocation ratios under different expected returns

Figure 11: Comparison of retracement and volatility with BTC combination versus BTC-free combination, optimal risk profile for a given target return

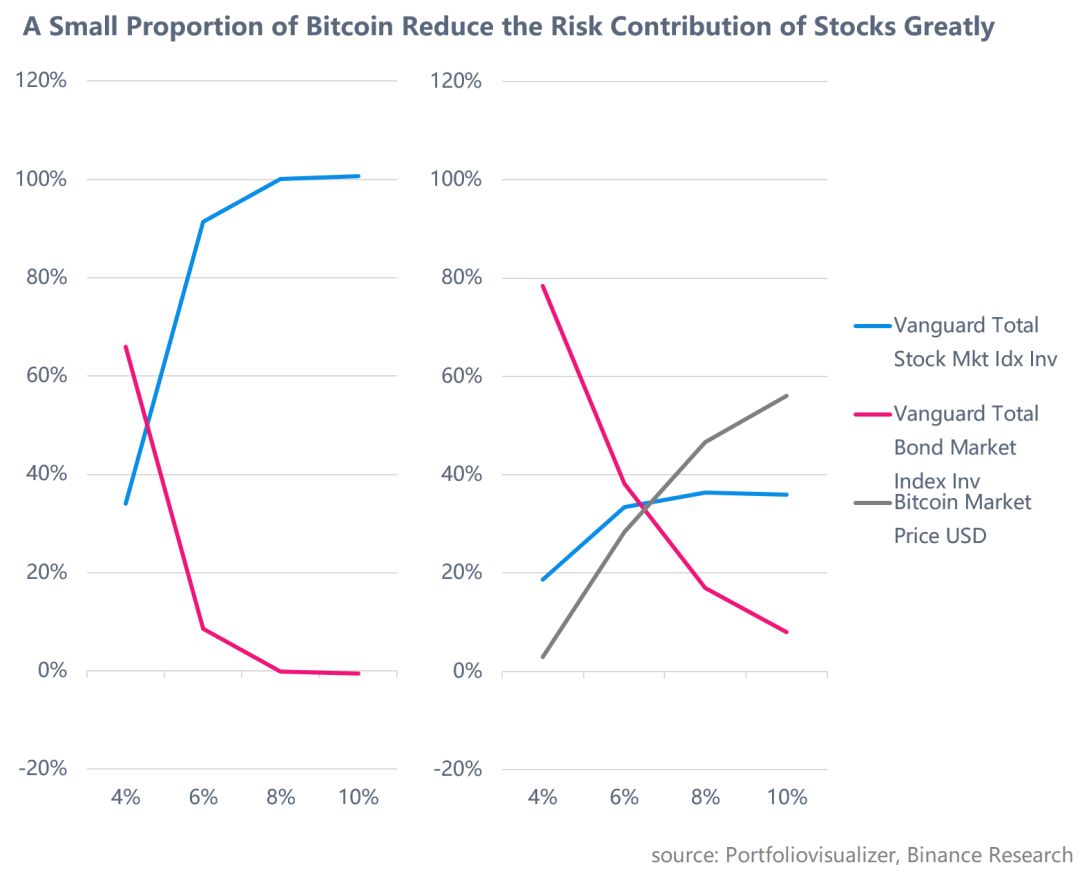

At first glance, this is counterintuitive. How can Bitcoin, as a highly unstable asset, reduce the volatility of its portfolio?

The answer remains, the characteristics of Bitcoin's ultra-high risk-reward ratio, which can increase the return on portfolios in a very low allocation ratio, so we can reduce the distribution of traditional high-risk assets (such as stocks) and then increase the traditional The allocation ratio of low-risk assets (such as national debt) uses the low volatility of bonds to stabilize the fluctuations of the entire portfolio.

Figure 12: Optimal Portfolio Risk Decomposition

That's why, as we saw from the optimal configuration table, the configuration ratio of the Vanguard Total Bond Market Index (ETF) calculated under the Bitcoin asset pool is higher than the traditional portfolio without Bitcoin. Much more.

Of course, when the target return is too high, for example, under the provided asset pool is greater than 12.97%, the traditional assets can not meet the target income, the simulated portfolio will have to passively assign weights on the bitcoin, the meaning of the results will be very limited.

Finally, it should be noted that, in the above configuration test, according to the data of the fixed history window , in the operation practice, the risk and return characteristics of each asset can also be checked according to the specified past time window to optimize the portfolio assets. Weights lead to more flexible adjustments.

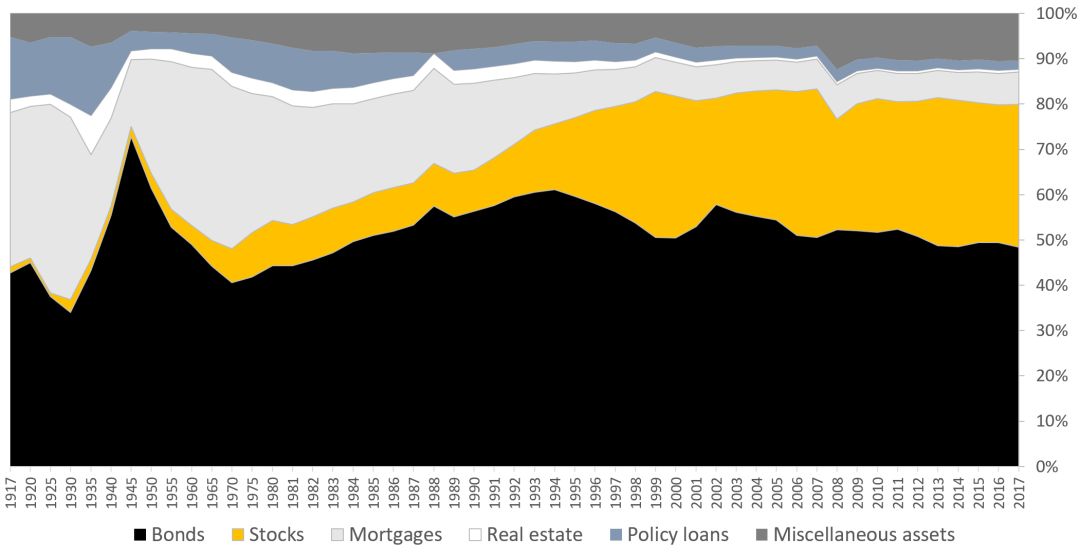

Figure 13: Proportion of distribution of asset allocations in US life insurance institutions

Source: Coin Research Institute, Distributed Capital, American Council of Life Insurers

This configuration idea has a very strong practical significance. Figure 13 shows that the proportion of US insurance assets allocated to stocks has increased over the past decades, which means that insurance companies are taking on higher and higher risks in exchange for gains. When macro risks break out, large proportions of stock assets may cause significant fluctuations in the portfolio, and the addition of a small amount of bitcoin as a new tool in the future may be expected to improve this phenomenon.

5.5 Add a simple timing strategy when combining configurations

Above we discussed the simple static configuration combination idea. However, although the mean-variance optimization model is beautiful and concise, the assumptions adopted are greatly simplified, and may not be flexible enough to meet the needs of real-world institutional investors, so the position adjustment is dynamically adjusted within a certain range. To avoid fluctuations in the market's concentrated decline, and actively pursue the maximization of returns without violating the contract with investors, it is highly respected by many secondary market funds.

In this report, we use two simple moving average strategy timing techniques to backtest the bitcoin configuration.

The moving average is to create an easily identifiable trend indicator with a flat closing price average to improve the clarity of the trading chart. Since these moving averages are dependent on past data, they are considered to be lag or trend tracking indicators. Nonetheless, these moving average indicators can still effectively eliminate noise and help determine market trends.

The following will test the performance of two moving average strategies, one is the price -average breakout strategy , and the other is the double-average strategy , which is essentially a simple trend-tracking strategy. That is, when the adjusted closing price is higher than the simple moving average, the model will invest 100% in the BTC, and when the adjusted closing price is lower than the moving average, the model will be converted into cash. The double-average strategy is the same principle, except that the closing price is replaced by a shorter moving average.

Because our goal is primarily to reduce risk, rather than frequent speculation, the following backtesting will use a relatively long-period moving average construction strategy.

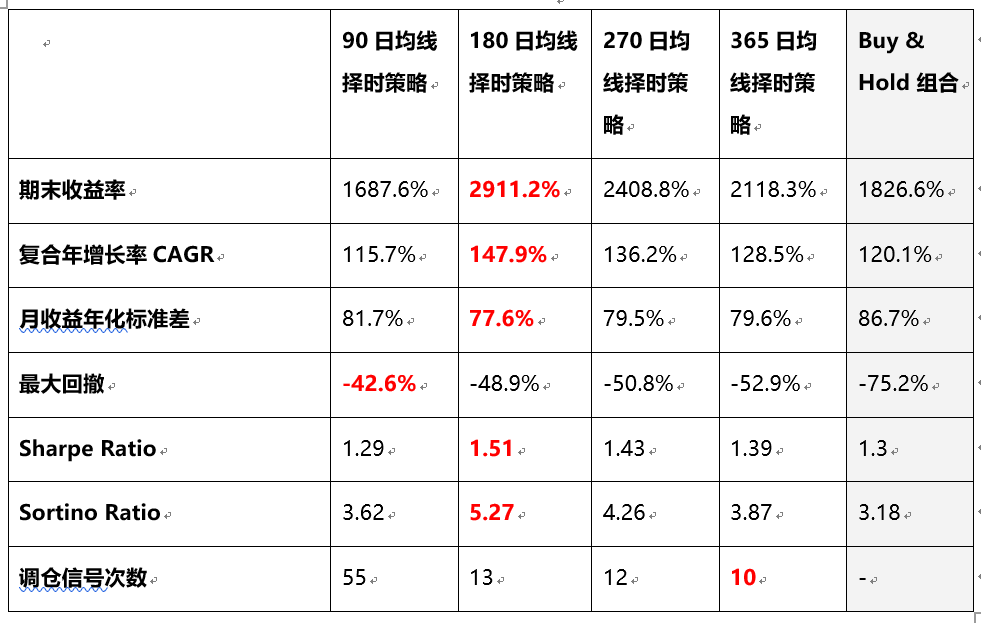

First, during the historical period from January 2016 to September 2019, 3 months, 6 months, 9 months, and 1 year were used as the moving average period, and the results of the time-tested back-test of the single asset of Bitcoin were displayed. The result of the 180-day moving average is better – higher yields, lower retracements, and lower volatility.

Table 12: Four-period single-mean strategy 2016.1~2019.9 backtest results (optimal result red bold display)

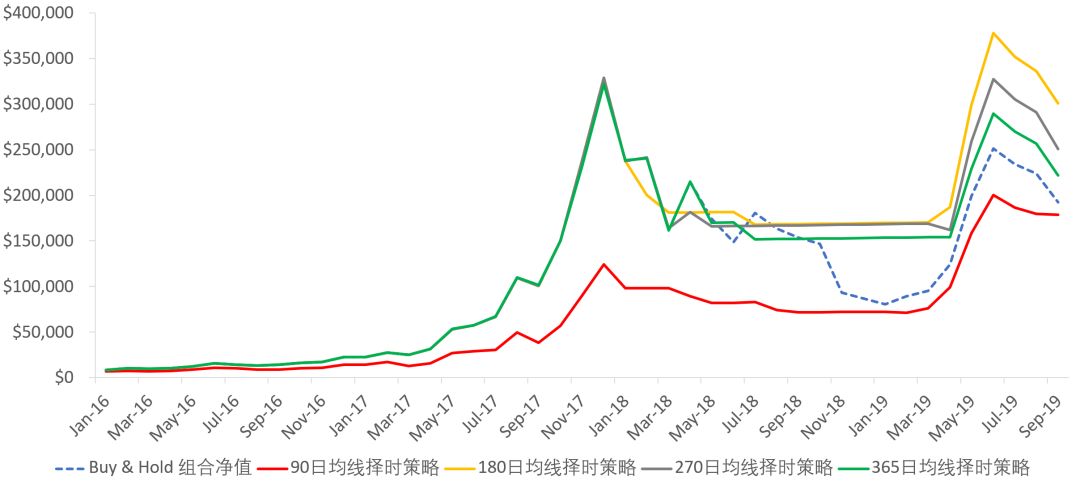

Figure 14: Assuming a net change in BTC investment with an initial net worth of $10,000 under different strategies

Source: Coin Research Institute, Distributed Capital

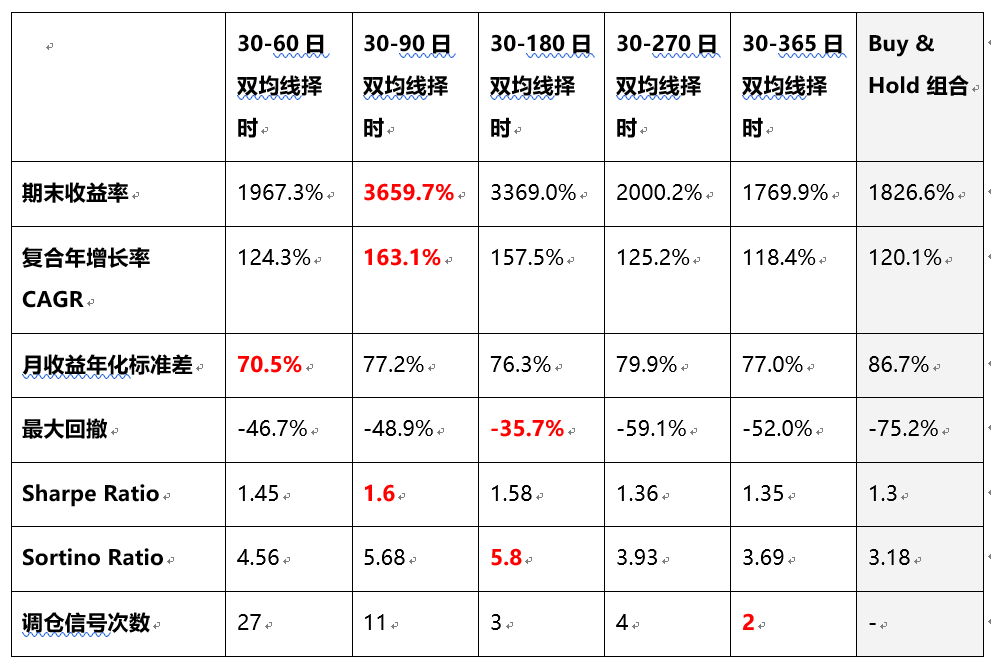

Secondly, during the historical period from January 2016 to September 2019, 30-60 days, 30-90 days, 30-180 days, and 30-365 days were used as the moving average period to select the bitcoin single assets. The results of the backtesting still show that even such a simple strategy can effectively reduce the fluctuation of the combination, especially in the avoidance of large-scale retracement.

In addition, compared with the single moving average strategy, the double moving average strategy filters out the abnormal fluctuations of more single-day prices, so that the number of times the call signal appears is much lower than the single moving average strategy, and the transaction cost and spread caused by the actual position adjustment are lost. It will also be reduced accordingly .

Table 13: Five-period double-average strategy 2016.1~2019.9 backtest results (optimal result red bold display)

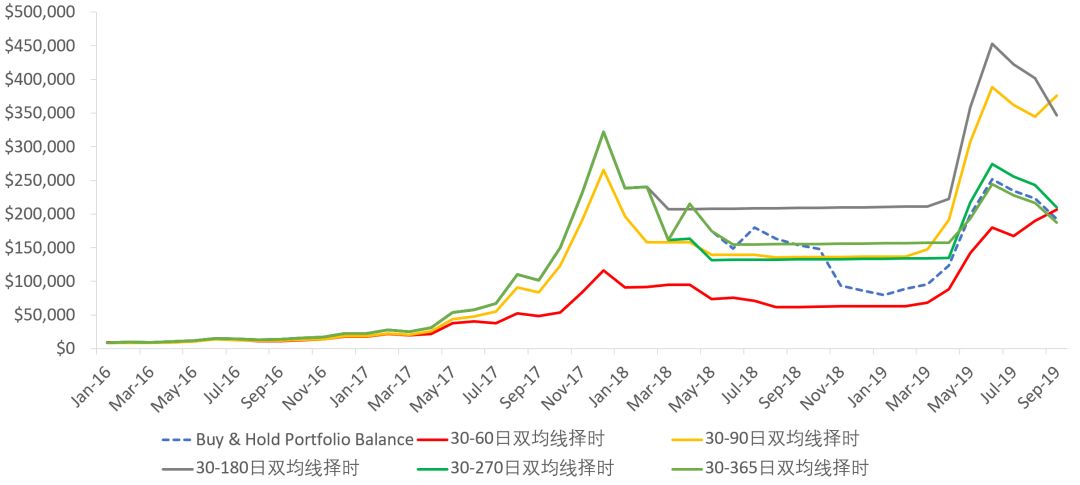

Figure 15: Assuming a net change in BTC investment with an initial net worth of $10,000 under different strategies

Source: Coin Research Institute, Distributed Capital

The secondary market can be used as a metric for timing signals. We have only tested the moving average strategy in the trend tracking method. In addition, the use of some relative strength indicators such as RIS, MACD, Beta coefficient, etc. can also be used to make kinetic timing, using market sentiment, trading volume, and even bitcoin network such as active address, chain transfer amount and other data, can become Timing indicators.

The above backtest shows that although a simple timing strategy may not improve the final return level, it is expected to further reduce the net value fluctuation of the digital asset allocation part and optimize the risk-return performance of the portfolio.

However, it should be noted that in most cases, the fund manager or its customers are configured in the portfolio because of long-term bullish bitcoin /digital assets. The short- and medium-term trend transactions should not be made, and it is difficult to become a portfolio. The main source of income, in addition to long-term admission opportunities often appear in the market down, as institutional investors, should pay more attention to the "left" investment opportunities.

6. Sources of income other than capital gains

The main discussion above is the “capital gain” portion of the investment in digital assets, which is the difference between the bid price and the bid price. However, in fact, if it is a professional asset management institution, the investment income of digital assets should also include “interest income” and “reinvestment income”.

The so-called “interest income” refers to the potential “risk-free” income that may be received during the holding of digital currency, and “reinvested income” refers to the acquisition of the already held digital currency into some risky products/platforms. Income.

The risk-free income component includes:

- "airdrop": The project/community is to promote/active the network for free distribution to existing currency holders (but may require some threshold or complete some tasks). For example, the Tron network mobilized the USDT to transfer its USDT to its network, and conducted a $20 million airdrop for users of the USDT in the TRC20 format.

- "fork" : The new "forked coin" brought about by the main chain. If you hold BTC, you can receive dozens of bitcoin forks in 2017~2018. Although there are not many valuables, a few market-recognized such as BCH, BTD, BTG, etc. can be used at certain times. Bringing considerable benefits, including the BCH's subsequent forked out of the BSV, means that investors can not only get "children" coins, but if they continue to hold even "sun" coins.

- Stake staking: For some blockchain networks that use the Proof of Consensus (PoS) mechanism, lock the token to the contract/address of the blockchain and participate in chain management or PoS mining activities. The rewards, this part of the income is risk free. The process of generating interest can be analogized to currency.

Table 14: Estimated rate of return for major digital currencies

Source: Coin Research Institute, Distributed Capital, stakingrewards.com

It is worth noting that if the number of digital currency itself is used as the valuation standard (currency standard), then the above three kinds of income will undoubtedly bring about a steady increase in the value of the relevant position, but if the purchasing power such as legal or stable currency is relatively volatile When small units are measured, the value of the above three types of income will be subject to greater uncertainty, mainly due to price fluctuations in the digital production itself.

For example, the BTC forked out of the BCH, if you sell at the beginning of the fork, you can get $555/piece. If you sell at the highest point, you can get $4,000/piece. If the sell-off is at the lowest point, you can only get $110/piece.

Then, the source of income that is held by the digital currency to take on additional risks is mainly pledge borrowing, which can be subdivided into two types, and the degree of risk is different.

● Lending for trading : After the money lender pledges assets into a platform, the platform lends its assets to users of the platform, and users can only use it for digital currency transactions on the platform. Unable to withdraw. This model is consistent with the model of margin financing and financing in the A-share market. The platform will have the ability to control the borrower's position and try to avoid the loss of the lender's principal.

● Lending for OTC financing : After the money lender, that is, the lender, pledged the assets into a platform, the platform lends its assets to the users of the platform or uses it for personal use. The user can transfer the digital currency. To any wallet, including selling into French currency. These platforms often require users to over-collateralize. For example, Dai requires ETH with a minimum mortgage currency value of more than $1.5 to borrow a $1 Dai.

Table 15: Loan interest rates for major digital currencies on the DeFi platform

Source: Coin Research Institute, Distributed Capital, loanscan.io

In order to obtain such benefits, the risk that the digital asset holder, that is, the lender, may include:

The volatility of variable interest rates: On most decentralized financial platforms, interest rates will fluctuate according to the agreement supply and demand mechanism, and the centralized lending platform is artificially formulated. Therefore, it brings risks associated with the uncertainty of interest rate returns.

Risk of price fluctuations: If the price of the collateral changes drastically, whether the price of the collateral changes drastically, the platform may not be able to realise the collateral of the borrower in time, resulting in the loss of the assets of the lender. During the period of the fund-raising platform, the phenomenon of “wearing the warehouse”.

Smart Contract Risk: As with most smart contract-based decentralized financial agreements, there may be risks in the overall behavior of smart contracts. However, some insurance platforms have emerged so that users can insure against smart contract risks that are unique to the dYdX platform.

Uncertainty about loans: Some platforms cannot match loans immediately, and if they are too long, they may lead to negative returns.

Long-term mismatch risk: Some products with pledge financial management cannot be redeemed in advance, and there may be a risk of long-term mismatch. If the fund is nearing the end of the lock-up period, there are a large number of digital assets locked in the pledge product. At this time, there are large LPs. Need to quit.

The platform poses a risk: the platform misappropriates customer assets, causing losses and even running.

In general, the five channels mentioned above for obtaining additional income, in the acceptable risk range, allow the digital asset position to receive at least an additional annualized 1% to 10% revenue, and the contribution to the overall portfolio should not be be ignored. However, due to the short time of the birth of the digital asset management industry, there is still much room for improvement in the fineness of management.

7. The correct way to open the door to digital assets

Although Nakamoto's vision in creating Bitcoin is to make Bitcoin an independent currency that is not affected by government policies, today's digital asset industry needs more clear and active regulation by the government than ever before.

When Global Custodian surveyed the current mainstream financial institution investors, the most people answered the most uncertain concerns about digital assets. The most people chose the uncertainty of the regulatory policy. The second place was the infrastructure of custody. imperfect.

First look at hosting, in addition to the digital currency exchange with its own hosted properties, there are currently dozens of service providers specializing in digital asset custody technology and solutions, the most famous such as Fidelity Digital Assets), Coinbase Custody, Anchorage, Bakkt, etc., similar to Cobo, Invault, KeyShard, Keystore, Matrixport, etc., can provide customers with digital asset storage, rights management, multiple security protection and other managed services.

However, infrastructure technology is not the core issue. The core issue is that there are no regulated custodians at the regulatory level. In other words, most countries and regions do not issue any digital asset escrow licenses to allow access and supervision of service providers; Many countries or regions do not even regard digital assets as a kind of financial asset, or at least qualitatively unknown, so as not to mention the supervision of custody services. Back in the end, infrastructure issues such as hosting are also policy issues. Currently, only Switzerland in the mainstream countries has just issued a license for digital asset banking, which regulates digital asset custody as part of its banking business.

Accordingly, in the case of digital asset-related transactions or other businesses, most countries and regions do not require parties to seek a qualified custodian for custody.

In the United States, for example, in 1940, the United States enacted the "1940 Investment Company Law," which clearly stated that funds must keep their securities and similar investment 'compliant custodians', including commercial banks with certain qualifications, and the National Stock Exchange. Members, etc. Currently, the US Securities Depository and Clearing Corporation (DTCC) is responsible for the custody and clearing of almost all US stock exchanges, corporate and government bonds, mortgage-backed securities, money market instruments and over-the-counter (OTC) derivatives.

For the custody of digital assets, the SEC (the US Securities Regulatory Commission) and FINRA (the US Monetary Authority) stressed in a statement in July 2019 that there is currently no solution for digital asset custody to meet the SEC's Investor Protection Act. 》 requirements. The reason is that the SEC and FINRA believe that holding only the private key does not represent legal ownership of the asset, but at best it represents an actual control capability (non-legal rights). The fact that a person holding a private key copy can take away digital assets without the permission of the custodian is one of the fundamental technical characteristics of the digital asset, but it also makes the digital asset unable to meet the regulatory requirements as an investable asset.

The crux of the problem lies in the “who holds the private key who owns the assets” advocated by Bitcoin, which is what the encrypted punks are proud of. “Assurance is absolutely privatized, and banks and governments cannot handle it”. This geek concept of “capability is the right” is not compatible with the modern property legal system, especially the fundamental conflicts with the principles of financial supervision.

However, for the regulatory rules of institutional investors themselves, the Hong Kong Securities Regulatory Commission also published the Standard Terms and Conditions of Licensed Corporations for Managing Investment Portfolios in Virtual Assets on October 4, 2019. Regulators who are willing to manage the configuration of digital assets for their clients can follow the example.

For institutional investors, the digital asset position allocation method has some indirect participation methods in addition to its own custody and three-party custody:

Table 16 Indirect investment in digital assets by institutional investors

( 1) Participation in the mining of digital currency: “mining” here narrowly refers to the process of participating in the new currency issuance of bitcoin and other digital assets using the workload proof mechanism, if the bitcoin is issued as a printing process Banknotes, then "mining" is the process of putting money into the printing machine, electricity and manual printing. (The specific bitcoin production process is not detailed here, please refer to the relevant documentation.)

Institutional investors' participation mainly includes direct investment in mining machine manufacturers and purchase of mining machines (computing power).

● Investment in mining machinery enterprises: As the mining machine manufacturer has a core position in the mining industry chain, it has the pricing power of the mining machine, and the efficiency of the mining machine is the most important part of determining the mining cost. Therefore, mining machine manufacturers have captured most of the profits in the digital currency mining industry chain. Several major mining machine manufacturers such as Bitian, Jianan, and others have previously submitted prospectuses to the Hong Kong Stock Exchange. However, due to the fluctuations in performance due to the impact of the digital currency market, they are seeking opportunities to list in the US and other markets. For institutional investors, investment in digital currency mining machine producers is closer to traditional equity investment, while enjoying the benefits of rising digital currency prices. In addition, mining machine manufacturers are also exploring the application of their chip business in AI and other fields, to a certain extent, to help smooth the impact of currency fluctuations on performance.

● Investing in mining equipment /mines (ie purchasing power): The process of directly purchasing a mining machine or indirectly purchasing computing power is essentially equivalent to paying a certain amount of fixed cost, pre-positioning the cost of purchasing digital currency as a fixed asset. The investment, if invested in the right time, can obtain digital currency at a lower cost relative to the market price.

The cost of directly participating in mining depends on factors such as the price of the mining machine, electricity costs, operation and maintenance costs, etc. The income is also closely related to the price of the digital currency. Once the digital currency price is lower than the fixed cost, the risk of shutting down is faced. But the benefit to institutional investors is that accounting may be simplified into equipment investment or service purchases rather than financial assets.

( 2) Investing in digital currency derivatives: Institutional investors can choose to trade on a compliant futures exchange, such as CME, Bakkt, or through investment trust funds (such as Grayscale, First Block). The disadvantage of investing in compliant futures contracts (CME, Bakkt's compliant futures products), trust funds, etc., is that current compliance futures contracts have time limits.

(3) Investment in open market products: compliant exchanges publicly listed funds (such as digital currency ETPs currently have publicly listed products in Switzerland and Sweden), and compliant registered private equity encrypted digital currency funds.

(4) Equity investment: There are many blockchain projects with equity structure, such as digital asset exchanges and technical service providers. Equity investment funds can obtain future digital assets issued by investment companies through investment in blockchain projects. The right to income, such methods have been adopted by many traditional equity investment funds.

to sum up

Although digital assets do not have widely accepted valuation methods, their value capture is clearly visible and even measurable. The digital assets represented by Bitcoin have great volatility, but the statistics show that their yield distribution is extremely positive and sharp, which means that they have a longer “right tail” and a relatively high probability of extreme positive returns. This means that Bitcoin has very good risk compensation, and the low correlation with the traditional financial assets is a valuable and scarce target for building a long-term investment portfolio.

Especially in today's global economic and monetary policy linkage, the systemic risk position of traditional portfolios is essentially converging, and encrypted digital assets are expected to be an excellent tool for diversification . However, given the special statistical characteristics of Bitcoin, if the goal of the portfolio is to pursue simple volatility minimum or maximum return, or the largest benefit-risk ratio (such as Sharpe ratio), it can only bring "non-black or white". (0 or 100% configuration) results.

However, if the maximum volatility or expected return target can be used as a constraint, the optimal configuration of Bitcoin can be calculated. The core logic is to replace large proportions of highly volatile stocks with low-proportion bitcoins, making bitcoin a source of excess returns, thereby increasing the allocation of low-volatility bonds and optimizing the yield-risk ratio of the entire portfolio.

In addition, the investment income of holding digital assets also includes “interest income” and “reinvestment income”. Some assets can provide relevant income of more than 10%, which is a considerable income channel other than capital gains. However, this seems to have not been widely Market participants value it.

It should be noted that trading slippage, taxation, and managed warehousing costs are not discussed in detail in this report, but for large investors, these are unavoidable issues that may affect asset management products to a large extent. Design and actual rate of return. In addition, the use of historical fluctuations and yields as input to the forecasting model is somewhat controversial for some people, but since the number of holders may be only 30 to 40 million vs. 7 billion people worldwide, even bitcoin is even At a very early stage, it is therefore difficult to make assumptions about the future benefits and volatility characteristics that are too conservative.

Reference material

1. "The depth of the block chain in Guosheng District | The dry season is approaching, the analysis of the whole industry chain of Bitcoin mining" 2019-09-02

2.SEC, FINRA, "Joint Staff Statement on Broker-Dealer Custody of Digital Asset Securities", July 2019

3. “InvestingLike the Harvard and Yale Endowment Funds” Michael W. Azlen, Ilan Zermati, 2017 Third Quarter

4. "TRONINCENTIVE PLAN REWARDS EARLIER USDT TRON ADOPTERS", Tron Foundation, April 2, 2019

5. Terms and Conditions of Licensed Corporations for Managing Investment Portfolios in Virtual Assets, Hong Kong Securities and Futures Commission, 4 October 2019

6. "Mining", Bitcoin wiki

7. "Numberof Blockchain wallet users globally 2016-2019", M.Szmigiera, October 7, 2019

8.AreBitcoin Bubbles Predictable? Combining a Generalized Metcalfe's Law and theLPPLS Model Spencer Wheatley March, 2018

|

|

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- US compliant project Blockstack on line currency security, regularly paying $250,000 in marketing expenses

- Analysis: Is Bitcoin still expected to be $20,000 at the end of the year? These three favorable conditions or help achieve the goal

- Domestic public chain is hot, which is strong?

- Blockchain Industry Weekly | Total market capitalization rose by 14.73%, China accelerated blockchain technology innovation

- Zhou Hongyi strongly recommended | New Yorker 16000 words heavyweight article: blockchain is the only hope to return to the essence of the Internet

- Jiang Zhuoer: How much does it cost for Bitcoin to rise to $100,000?

- Popular Science | Introduction to Cryptography (Part-1)