Goodbye Fork Swap, Uniswap V4 Enters the Era of “Ten Thousand Hooks”

Uniswap V4: "Ten Thousand Hooks" Era Begins - Goodbye Fork SwapAuthor: YBB Capital Researcher Ac-Core

Word Count: Over 5500 Read Time: 13 minute

Introduction:

Compared to the V3 version that was launched two years after May 21, V4 has more flexible asset composability and greatly reduces the Gas fees required to provide liquidity and exchange. With the support of the new feature Hooks, developers do not need to develop xxSwap, but only need to customize liquidity in Hooks and add front-end pages and elements that meet their own needs to open a “designated place”. At the same time, there is no need to worry about the lack of liquidity in the “designated place”. Let’s explore how Uni V4 leads DeFi from the “Lego era” to the “Ten Thousand Hooks” era.

- LD Capital: MakerDAO Status Update

- Evening Must-Read | Cancun Upgrade is Coming Soon, Reviewing Key Milestones in Ethereum’s History

- Is the surge in zkSync Era on-chain data a bubble or a real ecosystem?

YBB Capital Researcher Ac-Core self-made

Uniswap V4 – One of the few true innovations in the bear market

Uniswap’s iterative upgrades have shown us the infinite potential of the DeFi world, and it has never violated the original intention and rules of X*Y=K. The innovation of Uniswap V4 mainly focuses on providing more customized transaction logic, improving Gas efficiency and developer experience, and improving the convenience and efficiency of transactions. Compared with using V3, both developers and users can get more open, free, and efficient automated market maker services. The following article will comprehensively introduce the upgrade of V4 and the two most important changes: Hooks and Singleton.

The introduction of Hooks that changes everything

The core function of the Uniswap V4 version-Hooks, which allows each developer to create a customized DEX that meets their scenario requirements, and build their own “Lego blocks”. Hooks are an important concept introduced by Uniswap V4. They are plugins for customizing liquidity pools, exchange, fees, and liquidity provider (LP) position interactions. Through the Hooks mechanism, developers can perform specific operations at critical moments in the lifecycle of the liquidity pool, such as before/after the exchange, or before/after the LP position changes.

At the same time, Hooks are also smart contracts, and they interact with the core contracts of Uniswap V4, allowing developers to define and execute custom logic in a flexible way. Hooks can be bound to specific liquidity pools to control pool behavior and interaction. For example, developers can create a Hook that verifies specific conditions before each exchange, or perform some additional operations when the LP position changes.

YBB Capital Researcher Ac-Core

Through Hooks, mining pool creators can adjust mining pool parameters and introduce new functions to AMM. It can even allow various DeFi strategies to be built on Uniswap, ultimately benefiting LPs/swappers even more. We can imagine that the introduction of Hooks will bring greater flexibility and innovation space for developers, who can create unique liquidity pools according to their own needs and strategies to provide more innovative and personalized trading experiences, such as:

● Time-Weighted Average Market Maker (TWAMM): Developers can use Hooks to create liquidity pools that support TWAMM strategies to trade large orders averaged over a period of time.

● Dynamic fees: With Hooks, liquidity pools can dynamically adjust fees based on market volatility or other input parameters to better adapt to market conditions.

● Onchain limit orders: Hooks can be used to create and execute limit orders on-chain, allowing users to trade at a specified price.

● Interaction with lending protocols: Developers can automatically deposit funds that exceed the liquidity range into lending protocols through Hooks to maximize the utility of funds.

At the same time, Uniswap V4 currently supports the eight Hooks callbacks shown in the figure below. These Hooks can be executed before and after the transaction starts, enabling on-chain limit orders. In actual operation, a limit price can be set before the transaction starts, and then it can be checked after the transaction ends to see if it meets the limit price. If it does, the transaction is executed, otherwise it is cancelled.

YBB Capital Researcher Ac-Core

YBB Capital Researcher Ac-Core

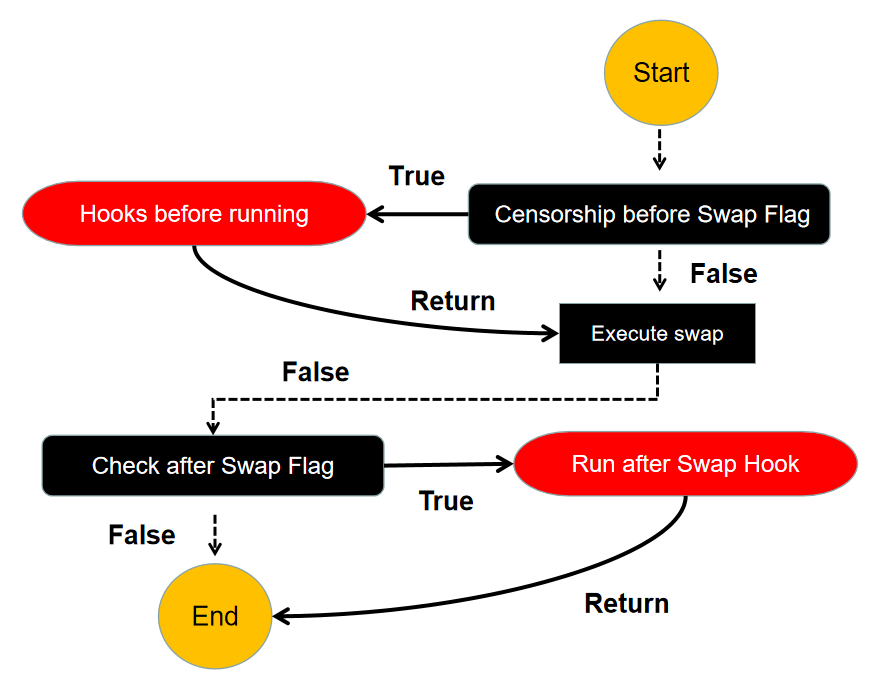

Another Hooks in V4 —— “ Action Hooks”

In addition to Hooks, there is another “Action Hooks” in Uniswap V4. It can only trigger the contract to run when the Flag condition is met, so it can call logic during the contract execution. Refer to the flow chart below to explain that before our asset exchange, the contract needs to check the Flag to evaluate the volatility of the liquidity pool. If the liquidity is high, the Flag will become True and run our Hooks. If there is insufficient liquidity, the Flag will become False, rejecting Hooks and keeping the interaction unchanged. By executing the operation shown in the figure below, “Action Hooks” enables a more gas-saving method to execute the Hooks we need. Next, the Singleton structure and Flash accounting will be introduced to achieve a cheaper asset exchange and contract deployment experience in V4.

YBB Capital Researcher Ac-Core 自制

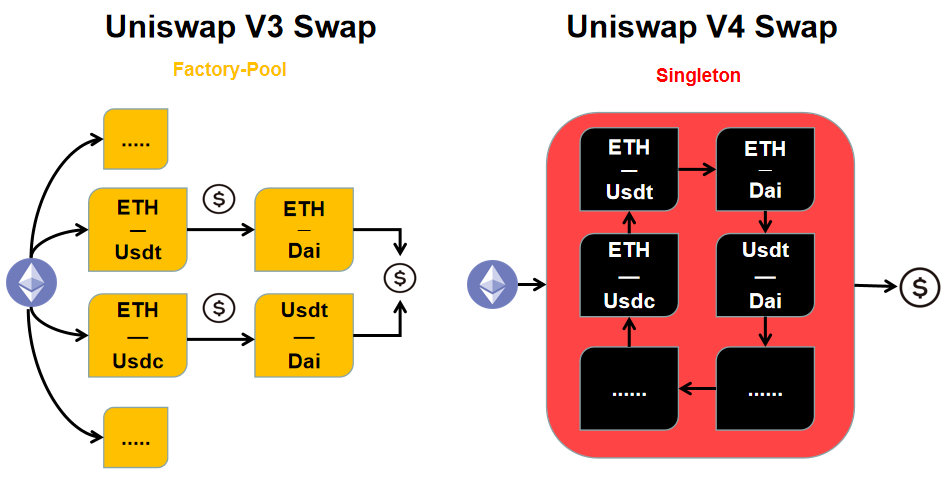

New Singleton Structure: Singleton

In previous versions of Uniswap, Factory-Pool was the contract structure used from V1 until now. It is also the contract structure most commonly used in the DeFi world for DEXs and derivatives. However, in V4, it abandons Factory-Pool and replaces it with the Singleton contract structure. In V3, each time a liquidity pool was created, a brand new contract had to be redeployed, which was very expensive. In V4, the Singleton structure saves all liquidity pools in one contract, which maximizes the reduction in gas consumption for creating liquidity and cross-chain pools (contracts). This means that token transactions no longer need to be transferred between different contracts, and it can even reduce gas costs by 99% from V3.

This Singleton structure is also equipped with a new “Flash Accounting” system. In V3, assets had to be transferred between liquidity pools every time an interaction ended. In V4, this system only transfers assets on the “net balance”, and each operation (exchange/deployment) only changes the internal balance. Asset balances are shown in units of “delta”. When the exchange ends, it only exchanges the net “delta” balance after a series of calculations. This means that a more efficient system can once again provide additional gas savings for Uniswap V4.

With “Singleton” and “Flash Accounting”, Uniswap V4 supports Native ETH. Users can trade directly with Ether (ETH) without the need for additional conversion operations, thereby improving the convenience of trading and saving gas fees. This makes the Uni and ETH ecosystems closely tied, and helps to support Ethereum.

In terms of contract structure, the storage and encapsulation of V4 liquidity positions data has also undergone huge changes. In V2, liquidity was distributed throughout the entire range (as shown in Figure 1), so the Uni protocol used homogeneous tokens (ERC-20) as liquidity certificates. In V3, due to the addition of limit liquidity, the corresponding liquidity display was changed to non-homogeneous tokens (ERC-721). In V4, we speculate that liquidity display will not be tokenized, but will be managed using the address of each wallet. In addition, EIP-1153 of the Cancun upgrade’s “transient storage” is also beneficial to the V4 system, which helps to further achieve cost optimization.

YBB Capital Researcher Ac-Core 自制

YBB Capital Researcher Ac-Core 自制

How to Allow Custom Oracle and Distribute Internalized MEV to LP Holders

UniSwap V4 is a decentralized trading protocol designed to enable trustless token trading on the Ethereum network. It offers higher liquidity and better trading experience by using custom Oracle implementation and internalized MEV (Maximizing Extractable Value) distribution mechanism. To allow custom Oracle implementation and distribute internalized MEV to liquidity providers (LP holders), consider the following steps:

1. Design a custom Oracle: You need to develop an Oracle that can provide customized price data. Oracle is a contract that fetches external data and provides real-time market price and other information to smart contracts. You can develop an Oracle contract customized according to your own needs, based on factors such as trading pairs, time, or other factors.

2. Implement internalized MEV distribution mechanism: MEV refers to the benefits generated in blockchain transactions due to changes in transaction order. UniSwap V4 directly distributes these benefits to liquidity providers through internalized MEV distribution mechanism. You can design a mechanism to distribute part of the profits directly to the corresponding LP holders when MEV occurs.

3. Contract integration and deployment: Integrate custom Oracle and internalized MEV distribution mechanism into UniSwap V4’s smart contracts. You only need to make modifications and extensions to the corresponding contracts to support these features. Ensure that security best practices are followed during contract development and modification, and conduct sufficient testing and auditing.

4. Notification and incentive mechanism: Promote this new feature to liquidity providers and provide them with appropriate incentives. Communicate with users through social media channels or other means to let them know the benefits of the new custom Oracle and internalized MEV distribution mechanism.

5. Monitoring and improvement: After deployment, closely monitor the operation of the system. Monitor the effects of transactions and MEV distribution and make improvements as needed. Feedback and participation in the community are important for further optimization of this mechanism.

Advantages of Customized Liquidity Pools

UniSwap V4 introduces the concept of customized liquidity pools, but customization is recommended based on centralized liquidity, so this change not only affects the development pattern of Fork Swap, the existence of aggregators, but also brings many advantages to liquidity providers and traders.

● Expanded liquidity provisioning options: Traditional AMM models often have fixed rules and parameters, which limits liquidity providers’ choices. However, Uniswap V4 allows for customized liquidity pools through Hooks, enabling liquidity providers to create different types of liquidity pools based on their preferences and strategies. This allows for a variety of liquidity pools of different sizes to appear on the market, providing users with more choices and flexibility.

● Reduced costs and increased efficiency: Uniswap V4’s architecture concentrates all liquidity pools in a single smart contract by introducing a “Singleton” contract. This architecture can reduce transaction costs, increase transaction efficiency, and simplify contract deployment and maintenance. In addition, customized liquidity pools can set more suitable fee structures based on specific needs, to meet the needs of different users.

● Provide a wider range of trading strategies and risk management tools: Customized liquidity pools provide traders with more opportunities for trading strategies and risk management tools. For example, by supporting the TWAMM strategy, large orders can be averaged over a period of time, reducing the impact on market prices. In addition, customized liquidity pools can integrate with other DeFi protocols, such as lending protocols and custom oracles, to provide users with more comprehensive trading solutions.

● Comprehensive enhancement of flexibility and creativity: Customized liquidity pools bring greater flexibility to liquidity providers. They can customize the management of their liquidity based on market demand and strategy. This flexibility and innovation potential can motivate more liquidity providers to participate, providing traders with diversified liquidity choices.

Issues to consider

YBB Capital Researcher Ac-Core 自制

1. What problem does the Curve solve that Uni V3 does not?

The Uni V3 AMM model is based on the X*Y=K trading model. In the process of actually combining LP, we will find that when extreme market conditions occur, not only is there a risk of total value loss without compensation, but there is also a risk of the exchange rate of the liquidity pool exceeding the range. Curve and Uniswap V3 are two different decentralized trading protocols that face slightly different problems and targets.

Compared to V3, Curve solves the following problems:

1. Earning profits in low liquidity ranges: Uniswap V3 has the feature of concentrating liquidity in specific price ranges, influenced by its AMM model, while other price ranges lack liquidity. This leads to higher transaction costs and limited liquidity when trading within larger price ranges. In contrast, Curve focuses on stablecoin-to-stablecoin trading and increases liquidity within price ranges by using an adaptive liquidity curve. This means that users can trade stablecoins within larger price ranges with lower slippage.

2. Low-cost trading: As Curve focuses on stablecoin-to-stablecoin trading, which includes assets with fixed price relationships, it employs specific algorithms and strategies to reduce slippage and transaction costs. This allows users to trade stablecoins at more competitive prices.

3. Better price discovery: Curve provides greater liquidity over a wider range, particularly when trading stablecoins, which allows for better price discovery. This means that users can obtain more accurate market prices for stablecoins to make better trading decisions.

4. Efficient stablecoin trading: Curve uses specially optimized algorithms and liquidity curves to provide efficient stablecoin trading. This enables users to exchange stablecoins quickly and securely with minimal slippage or cost.

2. Camelot: A DEX with a dual token economic model created using Uni V2

Camelot was originally a project launched on the Fantom network, named Excalibur. It later collapsed due to the use of UST as the stablecoin and randomly migrated to the Arbitrum ecosystem, where it was renamed Camelot. Unlike GMX, Camelot is more focused on guiding liquidity for new projects, with its main innovative mechanism being the permissionless “Nitro Pools”. Projects can completely control incentive measures to establish the liquidity type required for their own development.

It is important to emphasize Camelot’s dual token economic model, which combines Uniswap V2 with Curve’s decentralized trading protocol and supports trading for both volatile and stable token pairs, dispersing liquidity across the entire range from zero to infinity. Most importantly, it allows project teams to set the proportion of transaction fees based on market conditions and the specific situation of the protocol to manage dynamic and directional transaction costs.

In addition, Camelot’s custom LaunchBlockingd is also unlicensed for projects to issue tokens and guide more liquidity to them. Furthermore, each project that launches or collaborates on Camelot AMM can configure specific transaction rates for its LP to suit its own liquidity strategy needs.

Summary

Uniswap V4, as an important upgrade for decentralized exchanges, brings greater flexibility and creative space to the DeFi ecosystem by introducing the concepts of Hooks and customized liquidity pools. The Hooks mechanism allows developers to create unique liquidity pools according to their own needs and strategies, and provides rich transaction strategies and risk management tools. Customized liquidity pools expand the options for liquidity provision, reduce costs and increase efficiency, and provide a wider range of transaction strategies and risk management tools.

However, the emergence of V4 is bound to rebuild the underlying foundation of DeFi. It provides a super-large liquidity base pool, which developers can use to deploy their own Hooks or ecosystems, and even obtain high liquidity without a single-function xxSwap, enabling more developers to develop various multi-functional ecosystems on the Uniswap platform. Whether Hooks + SingLeton will combine with Curve+Camelot’s advantages to affect the next development trend of DeFi remains to be seen.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- As the staking rewards for Ether decrease, the protocol will have to seek innovative solutions.

- Exclusive new research on SUI: Distorted emissions? Dumping of non-tradable tokens?

- How to empower infrastructure and serve billions of users through account abstraction?

- Reflections One Month After Montenegro EDCON 2023: Forward-looking Trends in Infrastructure and Applications

- Can you earn money by running a node? How to choose a public chain? We talked to a node operator about it.

- Interpreting the Narrative of HOPE’s Resurrection

- Artificial intelligence data analysis tool KyberAI