Viewing the Supervision of Global Encryption Industry from the Regulations of Hong Kong Virtual Assets Trading Platform

Overview Overview

Background: This article will explain the regulatory methods and historical rules of ICO, exchanges and derivatives transactions, STO, etc. from local regulatory agencies. A cautious and open regulatory attitude, high compliance costs, and whether the digital currency markets of each country will be included in the regulatory scope?

Report report

The SFC of the Hong Kong Securities Regulatory Commission issued the "Trading Platform Position Book" on the official website on November 6, 2019 to remind companies or individuals engaged in STO of the applicable laws and regulations. The main points are as follows:

- First of all, it has Hong Kong No. 1 (Securities Trading) and No. 7 (providing automated trading services);

- At least one securitization token project;

- Platform funds must be hosted by a third party;

- 98% of the customer's virtual assets are stored online under the wallet;

- The exchange insurance coverage needs to cover 95% of the assets;

- It is best to apply without a platform for digital currency trading, as the single entity principle and the application for other business will be included in the scope of supervision;

- Must be a centralized trading platform;

- Serve only qualified investors;

- The operational framework adopted and the technology used should ensure that the same guarantees are provided to customers as traditional financial institutions in the securities industry.

See the appendix for details.

- The Supreme People's Court requested to strengthen the application of blockchain to promote the wisdom court; the Hong Kong Securities Regulatory Commission issued a new virtual asset policy

- 11000+ participants, 130+ speakers, 13.5 million+ full network exposure, World Blockchain Conference·Wuzhen created these “data miracles”

- Viewpoint | Exchange is the public chain platform

Hong Kong Securities Regulatory Bureau's attitude towards virtual assets

On September 5, 2017, the Hong Kong Securities and Futures Commission (SFC) issued a statement on the ICO (according to the statement of the Securities and Futures Commission, although the digital tokens usually provided in the ICO are often referred to as “virtual goods”, According to the facts and circumstances of the ICO, the digital tokens offered or sold may be “securities” as defined in the Securities and Futures Ordinance and the Futures Ordinance (Chapter 571) and subject to Hong Kong securities laws.

According to the Securities and Futures Ordinance, whether the ICO's digital tokens are considered securities is a complex legal issue. There are many relevant factors to consider when determining whether a digital token is a security, such as the terms of the token (including its characteristics) and the underlying platform and business model, such as whether the token is used to fund the project to facilitate the payment system or A tool for trading cryptocurrencies on exchanges.

The SFC Statement outlines three products that may constitute “securities” by digital tokens, ie, digital tokens are considered shares, bonds or equity in the Collective Investment Plan (CIS).

A digital token sold in ICO, if it represents a company's equity or ownership interest, may be considered a “share”. For example, a token holder may be entitled to shareholder rights, such as the right to receive dividends and the right to participate in the allocation of the remaining assets when the company is wound up.

If the purpose of the digital token is to enter into or confirm the debt or debt borrowed by the issuer, it may be considered a "bond". For example, the issuer can repay the principal of the investment and pay interest to them on the specified date or redemption.

If the proceeds from the sale of tokens are collectively managed by the ICO planners and invested in different projects, so that the token holders can participate in sharing the returns provided by the relevant projects, the digital tokens may be considered as " The interest in the collective investment plan.

Equity, bonds and collective investment plans are considered “securities”.

Clear boundary

A digital token that trades or provides advice under the Securities and Futures Ordinance, or a fund that manages or sells such digital tokens, may constitute a “regulated activity”. A party engaged in a “regulated activity” must obtain a license from the SFC for its activities against the public in Hong Kong, whether or not it is located in Hong Kong. In the case of a person acting as a principal with a “first class professional investor”, there is only a limited exemption requirement to trade the securities. This includes licensed investment intermediaries, authorized financial institutions, regulated insurance companies, regulated collective investment schemes, governments and various institutional agencies.

If the ICO is involved in the sale of shares to the public, the detailed prospectus (eg format, content and registration) requirements under the Companies (Winding Up and Miscellaneous Provisions) Ordinance, Chapter 32 of the Laws of Hong Kong will apply unless the ICO is in compliance with the Companies (Winding and Miscellaneous) The exception is one of the twelve "safe harbors" listed in Schedule 17 of the Ordinance. Some safe harbors include:

- An offer to an investor who meets the definition of "professional investor";

- An offer to no more than 50 persons;

- "Small-scale offering" means that the total consideration payable for the relevant shares does not exceed HK$5 million (or equivalent in another currency); or the minimum denomination of the relevant shares or the minimum consideration payable by any person for the relevant shares. An offer of less than HK$500,000 (or equivalent in another currency).

In addition, if the ICO involves an offer to participate in a collective investment plan to the public, it must be authorized by the SFC unless the exemption applies. Section 103 of the Ordinance provides that any advertisement, invitation or document shall be issued unless the Commission's authorization or exemption applies, and the advertisement, invitation or document contains or invites the Hong Kong public to invest in the collective investment scheme, ie He is guilty of an offence and is liable to a fine and imprisonment. Therefore, issuing an advertisement, invitation or document to invite the Hong Kong public to invest in the ICO that constitutes a collective investment scheme will be defined as a criminal offence.

Strict supervision

The Hong Kong Securities Regulatory Commission's regulatory attitude toward virtual assets is serious and firm, and it is not just a paper-based policy, it is not compromised in the law enforcement process.

On December 11, 2017, the Hong Kong SFC issued a Circular to Licensed Corporations and Registered Institutions: About Bitcoin Futures Contracts and Investment Products Related to Cryptographic Currency. The circular reminds that "Hong Kong investors can buy and sell Bitcoin futures contracts through intermediaries, but providing trading services and related services (including communication or delivery of trading orders) to Hong Kong investors constitutes a regulated service, regardless of whether the business is located or not. Hong Kong must apply for a licence from the Securities and Futures Commission."

In February 2018, SFC issued a warning letter to seven cryptocurrency exchanges, warning them that they should not buy or sell cryptocurrencies that belong to 'securities' without a license. In addition, SFC sent a letter to seven ICO issuers, most of whom have confirmed compliance with the regulatory system or have immediately stopped selling tokens to Hong Kong investors.

In March 2018, SFC also directly called the ICO activity of a crypto company, Black Cell Technology, because the ICO activity was an unregistered collective investment plan (CIS), which was classified as “securities”. Also, SFC requires Black Cell to refund funds from Hong Kong investors who have subscribed to the token.

On November 1, 2018, the CSRC issued the “Declaration on the Regulatory Framework for Management Companies, Fund Distributors and Trading Platform Operators for Virtual Asset Portfolios”, and listed two types of virtual asset portfolio management companies in the securities regulatory system. Within the scope of supervision:

The first category is companies that manage funds that are fully invested in virtual assets that do not constitute "securities" or "futures contracts" and distribute them in Hong Kong. These companies are generally required to receive the first ones because they distribute these funds in Hong Kong. A license for a regulated activity (dealing in securities). The SFC will also impose licensing conditions on the activities of these funds to monitor them.

The second category is a company that has a licence to manage a portfolio of "securities" and/or "futures contracts" and is required to apply for a type 9 regulated activity (providing asset management). Or part of (subject to the minimum exemption requirement 6) investing in a portfolio of virtual assets that do not constitute "securities" or "futures contracts", the SFC will also carry out relevant management work by applying licensing conditions. Monitoring.

On March 28, 2019, the Hong Kong Securities Regulatory Commission issued the "Statement on the Issuance of Securities-type Tokens", which stipulated the securities-type tokens in the STO as "securities" and included them within the scope of the Securities and Futures Ordinance.

With the release of the trading platform position book on November 6, 2019, the CSRC has added the last piece of the digital asset regulation. Since then, the laws and regulations related to the issuance of tokens have become clearer. It can be said that Hong Kong's regulators have always maintained a prudent attitude and have never slackened.

National blockchain regulatory policies

In the past few years, the global attitude towards the rise of cryptocurrencies has changed a lot. Although the term "cryptocurrency" is a bit of a misnomer, some countries do consider digital currency to be legal tender, and some countries treat cryptocurrency as a commodity.

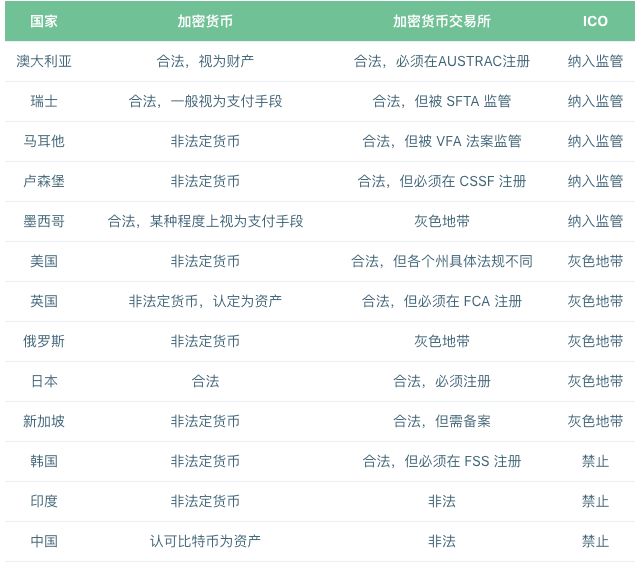

The following table is a table of the major countries where cryptocurrency regulations are issued:

US: Strong supervision, perfect legislation

The first important announcement about ICO was issued by the US Securities and Exchange Commission (SEC).

In July 2017, the US Securities and Exchange Commission (SEC) issued a survey report based on the Securities Act of 1933 and the Securities Exchange Act of 1934, provided by a “virtual” organization called DAO. And the "DAO token" sold is "securities". It provides tokens to exchange Ethereum (ETH) and uses the raised ETH to provide project funding. DAO token holders are willing to share the expected profits of these projects as a return on their investment in DAO tokens.

According to the US Securities Law, securities include “investment contracts”, which are monetary investments in ordinary businesses whose reasonable expected profits come from the efforts of other entrepreneurs or managers. The SEC stated that the offer and sale of a particular transaction involving securities will depend on the facts and circumstances.

Since the beginning of this year, the US Securities and Exchange Commission (SEC) has published at least 12 related penalties and review incidents. Among these penalties, the US SEC imposed a penalty of between US$30,000 and US$3 million; the penalty targets are wide, including 3 cryptocurrency trading platforms, 3 companies suspected of fraudulent ICO, and 2 Companies that conduct ICO projects, two companies or funds that provide asset management, and litigation with individuals, a blockchain concept company.

China: ICO is banned against cryptocurrencies

So far, the most rigorous response to ICO has been the People's Bank of China, which issued a notice on September 4, 2017, with six other financial regulators in China, prohibiting the issuance of ICOs in China. In the circular, the ICO was declared an unauthorized illegal fundraising event. The notice also prohibits the circulation of digital tokens as currency in the market. The notice states that ICO is not issued by the monetary authorities, does not have legal and monetary attributes, and does not have the same legal status as currency. All ICOs must stop immediately from the date of the circular. Funds already raised through ICO must be returned to investors.

Digital token financing and trading platforms are prohibited from redemption of legal tender and virtual currency, trading of virtual currency, and provision of pricing, information and intermediary services related to virtual currency.

Financial institutions and non-bank payment institutions are prohibited from providing ICO-related services or products, such as account opening, registration, trading, settlement, clearing and insurance, directly or indirectly. Until now, China has only advocated the development of blockchain technology, but the attitude towards the coin blockchain project has remained unchanged.

Singapore: Serious regulation, but open compliance

In August 2017, the Monetary Authority of Singapore (MAS) issued a press release clarifying that if the token constitutes a product regulated by the Securities and Futures Act (Chapter 289) (SFA), it will be issued or issued in Singapore. Digital tokens are regulated. .

MAS also noted that given the anonymity of ICOs and the ease with which large amounts of funds can be raised in a short period of time, they are vulnerable to AML/CTF risks. MAS is evaluating AML/CTF risk monitoring methods related to digital tokens that are not purely used as virtual currency.

MAS pointed out that the function of digital tokens has surpassed the scope of only virtual currency. For example, a digital token may represent ownership or security interest in the issuer's assets or property and may therefore constitute a share or unit offer in the SFA's collective investment plan. As another example, a digital token may represent the debt owed by the issuer and is therefore considered a bond under the SFA.

If the digital token is a definition of a security as defined by the SFA, the issuer will be subject to the prospectus (unless exempted) and the issuer and intermediary will also be licensed by the SFA and the Financial Advisers Act (Chapter 110). Requirements (unless exempted) and AML / CTF requirements.

On January 14, 2019, the Payment Services Act was reviewed by the Singapore Parliament and has been formally enacted. The bill has a direct impact on many digital currency exchanges, wallets and OTC platforms in the Singapore market, and comprehensive oversight of related businesses from both risk control and compliance. The scope of the bill is that all relevant institutions operating in the Singapore market are not limited to those registered in Singapore. After the official launch, the relevant agencies will have six months to file with the HKMA.

The first license is applicable to a “money changer” and the service provider who obtains the license can only provide a money change service. The scope of the regulation is quite narrow, as these are off-site services that are usually provided by small businesses such as sole proprietors and have limited risks. The HKMA primarily monitors suppliers' money laundering and terrorist financing risks.

The second license "Standard Payment Agency" can provide any combination of seven defined payment services. If the entity holds a digital currency of no more than $5 million and the monthly transaction amount exceeds $3 million, the license can be applied for. Such service providers will be subject to a lower degree of supervision, and the regulatory environment is similar to the “sandbox” established by the Hong Kong Monetary Authority for digital currency exchanges.

The third license "large payment institution" license is subject to supervision over all businesses set by the "standard payment institution" license. Due to the larger amount involved, the risk is higher, the licensing requirements are more stringent, and the scope of supervision is broader.

In summary, Singapore's digital currency exchange involves a third type of “large payment institution” license when it comes to payment-type token transactions (such as bitcoin).

Russia: The corresponding regulations are not clear

According to Olga Skorobogatova, deputy governor of the Central Bank of the Russian Federation, in June 2017, the central bank intended to introduce its own national cryptocurrency. On September 4, 2017, the Bank of Russia issued a statement warning the high risks associated with cryptocurrencies and expressed the view that it is too early to recognize the cryptocurrency trading in Russia.

On September 8, 2017, Russian Finance Minister Anton Siluanov said at the Moscow Financial Forum that the Treasury will regulate Russian cryptocurrency by the end of 2017. According to Siluanov, buying cryptocurrencies is not a ban on cryptocurrencies, but should be treated like buying securities.

Britain: prudent response, but open

On September 12, 2017, the UK Financial Conduct Authority (FCA) issued a statement on ICO warning consumers that ICO is “very high-risk speculative investment”. FCA warns people that they should invest in ICO only if they are confident in the quality of the ICO project and are prepared to lose all their shares.

FCA warns of ICO-related risks, including most ICOs are not regulated by FCA, lack investor protection, price volatility, the possibility of fraud, and most are in the early stages of development. In addition, the ICO is not subject to a regulated prospectus, but rather a “white paper” is usually issued, which may be unbalanced, incomplete or misleading.

Whether the ICO is regulated by the FCA depends on the circumstances and depends on the structure of the ICO. FCA warns companies that they should carefully consider whether their activities can constitute arrangements, transactions or consultations on regulated financial investments.

However, in recent months, as the Financial Market Conduct Authority (FCA) updated the guidelines for cryptocurrencies and a series of negotiations on crypto-industry regulation will begin at the end of this year, the situation begins to change slowly.

So far, the UK has not enacted any laws specifically for cryptocurrencies, and its regulators have adopted a fairly relaxed attitude towards cryptocurrencies. Although the country does not have explicit cryptographic monetary legislation, cryptocurrency is not considered legal tender, and exchanges are required to be registered with the FCA. The guiding principles emphasize that entities engaged in encryption-related activities should comply with current derivatives financial regulations. Obtain authorizations (such as futures and options).

However, this will change after the entry into force of the UK's fifth edition of the Anti-Money Laundering Act on January 10, 2020. Eric Benz, CEO of Exchange's Changelly, said of the current regulatory situation in the UK that the regulatory framework is trying to keep up with emerging markets and added: "I do think that regulation is a good thing, but only if it is appropriate The way to market new markets. Applying traditional old regulations to cryptocurrencies simply doesn't work because its essence is designed to avoid regulations. Not only in the UK, governments around the world must have a better understanding of markets and technologies. ”

appendix

What are the conditions for applying for this license?

- The subject of the transaction is the securitization token;

- There is at least one securitization token, which already has 1, 7 licenses. And a trust company that holds a license for a trust or company service provider to apply;

- Provide automatic control services and control of token assets. Decentralized exchanges are not regulated. OTC is not automatically traded or regulated.

What rules are required for digital asset exchanges?

Investment asset restrictions:

- The platform operator should only include virtual assets that meet the following instructions (Note 1);

- Asset-backed;

- Approved by a regulatory body in a comparable jurisdiction (which is approved by the SFC from time to time), deemed eligible or registered;

- Assets with a 12-month post-release history record;

- The platform operator shall hold the client's assets for its clients through a company in trust, and the company shall be (i) the “connected entity” of the platform operator under the Securities and Futures Ordinance (Note 2).

Investor restrictions

- Only provide services to professional investors (Note 3);

- As long as it is only sold to professional investors, it is not subject to the Hong Kong investment offer approval process and the prospectus registration system. (As long as it is sold to qualified investors, it does not need to be disclosed)

Off-site supervision

- Approved by the SFC for any introduction or provision of new or accompanying services or products;

- An independent professional company acceptable to the SFC must be engaged to conduct an annual review of the licensee's activities and operations, and to prepare a report confirming that it has complied with the licensing conditions and all relevant legal and regulatory requirements (trusted independent Tripartite audit).

Other focus

- Clients should not be provided with any financial facilities for them to purchase virtual assets, and should be as close as possible to ensure that the corporations in the same group of companies to which they belong do not. (Cannot conduct margin financing and securities lending)

- It should always have sufficient liquidity and assets of its own in Hong Kong, such as cash, deposits, treasury bills and certificates of deposit (but not non-virtual assets). The amount should be equal to the actual operation of the platform operator on a continuous basis for at least 12 months. expenditure. (financial stability requirements, class deposit reserve)

- A licensed operator is a licensed corporation and is required to comply with the relevant provisions of the Securities and Futures Ordinance and its subsidiary legislation (compliance requirements are in compliance with the Securities and Futures Ordinance).

- Unless the applicant for the licence is a suitable candidate (Note 4), the SFC must refuse to grant the licence.

- The Platform Operator shall establish a function for the formation, implementation and execution of: rules that apply to the obligations and limitations of the Virtual Asset Issuer (for example, any proposed hard-fork or airdrop, any significant change in the issuer's business) Or any liability for the issuer's regulatory actions to inform the platform operator); the criteria and applications for the inclusion of virtual assets in their platforms (which take into account the criteria set out in the relevant terms and conditions); and related suspensions, suspensions and withdrawals The criteria for trading a virtual asset on its platform, the option that the customer holding the virtual asset can exercise, and any notice period. (Need to establish a series of public currency standards)

- The platform operator ensures that the company's activities are carried out under a single legal entity licensed by the Securities and Futures Commission.

- As long as the platform involves securities-type token trading activities (even if it only accounts for a small portion of its business), the SFC's regulatory area covers all relevant areas of the platform's operations.

Conflict of interest

Platform operators should not participate in proprietary trading (Note 5).

Asset protection

- The SFC will require platform operators to ensure that (or their associated entities) store 98% of their virtual assets in online wallets and limit their virtual assets held in online wallets to no more than 2%.

- The platform operator ensures that the insurance purchased is valid at all times, and its coverage should cover the risks involved in holding the virtual assets of customers in online storage (full coverage), and the custody of holding virtual assets of customers in offline storage. The risks involved (most of the guarantees, such as 95%).

Due diligence

Before the platform is in the currency, you need to investigate:

- The background of the management or development team of the virtual asset issuer;

- The regulatory status of virtual assets in various jurisdictions where the platform operator provides trading services, including the availability and sale of virtual assets under the Securities and Futures Ordinance, and whether the regulatory status will also affect the regulatory obligations of the platform operators;

- The supply and demand of virtual assets, market maturity and liquidity, including its market value, average daily volume, whether other platform operators also provide services that facilitate the trading of virtual assets, and whether there are related transaction combinations (such as legal currency against virtual assets) ), and in which jurisdiction the virtual asset has been sold;

- The technical level of the virtual asset, including the security infrastructure of the blockchain protocol for the virtual asset, the size of the blockchain and network (especially whether it is vulnerable to 51% attacks), and the type of consensus algorithm;

- The level of activity of the development community;

- The popularity of the ecosystem;

- The virtual asset promotion materials provided by the issuer shall be accurate and not misleading;

- The development of virtual assets, including the results of any of its related projects contained in its white paper (if any), and any significant events related to its history and development.

Name explanation

Note 1. Virtual assets: A reference to “virtual assets” refers to assets that express value in digital form, in the form of digital tokens (such as digital currency, functional tokens, or tokens secured by securities or assets). ), any other virtual commodity, crypto asset or other asset of substantially the same nature, whether or not such asset constitutes a "securities" or "futures contract" as defined in the Securities and Futures Ordinance.

Note 2. Associated entity: A reference to a “connected entity” means a company that meets the following requirements: (i) has notified the SFC that it has become a licensee under section 165 of the Securities and Futures Ordinance. (ii) a corporation incorporated in Hong Kong; (iii) a "trust or corporate service provider licence" within the meaning of the Anti-Money Laundering and Terrorist Financing Ordinance (Cap. 615); and (iv) a wholly-owned subsidiary of the licensee;

Note 3. Professional investors: Professional investors must meet the following requirements:

- Any individual ("individual professional investor") having a portfolio of not less than 8 million yuan (or any equivalent foreign currency) (either alone or in conjunction with his spouse or children in a joint account);

- Any trust corporation with a total assets of not less than $40 million (or any equivalent foreign currency) entrusted;

- Have (a) a portfolio of not less than $8 million (or any equivalent foreign currency); or (b) any corporation or partnership with a total asset of not less than $40 million (or any equivalent foreign currency); and the sole business It is any corporation that holds an investment project and is wholly-owned by any one or more individual professional investors or persons mentioned in 2 or 3 above.

Note 4. Appropriate candidates: Applicants are – (i) a company; (ii) a registered non-Hong Kong company as defined in section 2(1) of the Companies Ordinance (Cap 622); or (by 2012 Replacement of No. 28, Nos. 912 and 920) (iii) A corporation that meets the following description and is not a company or a non-Hong Kong company – (Amended 30 of 2004 s. 3) (A) mainly operates a business outside Hong Kong The business of the event, if carried out in Hong Kong, would constitute such a regulated activity; (B) if there is no provision of section 115(1)(i) and (ii), section 114(1) And (c) if the corporation has a place of business in Hong Kong, section 16 of the Companies Ordinance (Cap 622) will apply to the corporation; (28 of 2012) (Amended) Sections 912 and 920) (b) A person referred to in section 125(1)(a) and (b) has made an application under section 126 for approval of their duty to be an applicant for such activity. Personnel; and (c) an application under section 130(1) requesting approval of the use of a premises as an applicant for the storage of records or documents required by this Ordinance.

Note 5. Self-employed trading: refers to the trading activities for the following accounts:

- The account of the platform operator who trades as the principal;

- An account of any user who is a company of the same group of companies as the platform operator and is trading as a principal;

- The platform operator or any account that is itself interested in any user of a company that is part of the same company group as the platform operator.

Conclusion

Although the degree of cognition and acceptance of virtual assets varies from country to country, what we can see is that worldwide regulatory regulations for virtual assets are accelerating development and implementation. The barbaric growth of the digital currency economy will gradually come to an end as the regulations improve. For participants in the digital currency industry, actively welcoming compliance has become the only choice for maintaining the path of development in the future. The sooner you actively embrace compliance, you can take the lead in the second half of the industry.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Science | Ether Square 2.0's future blueprint and challenges

- Wuzhen·Policy is coming. Are you waiting to be acquired by BAT or become the blockchain native BAT?

- "Bitcoin Revolution" report: Bitcoin economy is similar to Europe in the 16th century, optimistic about the derivatives market

- The world's first CBDC, Tunisia's counterattack

- Singapore Monetary Authority and JPMorgan Chase to develop blockchain-based cross-border payment prototypes

- Bitcoin Position Weekly | The largest such account has begun to “prompt risk”

- Bitcoin version 0.19.0 Core client will be officially released, the bech32 address format is enabled by default and BIP70 is disabled.