European Central Bank Market Infrastructure and Payment Division Director: CBDC's main risks and problems are bank disintermediation

Author: Ulrich Binder (European Central Bank market infrastructures and payment Division)

Compilation: Wang Rui, Zhang Aimei, People's Bank of China Frankfurt Representative Office

Source: China Financial Journal

Editor's Note: The original title was: "China Finance" | Ulrich Binder: Central Bank Digital Currency with Double Interest Rate System

- Technology Sharing | Synergy between Cryptography, Blockchain and Privacy Computing

- Security Monthly Report | More than 17 typical security incidents occurred in March, the prospects and risks of Ethereum Defi coexist

- QKL123 Blockchain List | USDT market value jumped to fourth place, transaction popularity dropped significantly (March 2020)

Central bank digital currency (CBDC) can be regarded as the third form of base currency after the central bank overnight deposits and paper currency. Central bank digital currency can be divided into wholesale central bank digital currency and retail central bank digital currency. The former is only provided to specific legal persons such as banks, while the latter is available to the public. Unless otherwise specified, the research in this article is mainly aimed at retail central bank digital currencies.

Analysis of the advantages and disadvantages of central bank digital currency

Existing research believes that the central bank's digital currency may have advantages in four areas, but there is no conclusion about this.

One is to improve retail payment efficiency. For economies with underdeveloped electronic payments by commercial banks and / or a lack of a safe and efficient payment system, central bank digital currency allows the public to use modern central bank currency safely and efficiently. For economies with declining cash demand and uncompetitive private electronic payments, central bank digital currencies can further enhance the resilience, availability, and competitiveness of retail payments.

The second is to solve the problems of illegal cash payment and value storage in areas such as anti-money laundering and counter-terrorism financing. Because of its anonymity and untraceability, cash is often favored by criminal activities such as money laundering and illegal exchanges. Central bank digital currency helps to overcome these shortcomings of cash while maintaining convenience. However, to achieve this, certain prerequisites are needed: the banknotes in circulation (at least large denomination banknotes) have been widely replaced by the central bank digital currency, and the central bank digital currency cannot be a token-based digital currency (that is, based on cryptocurrency technology The issued central bank digital currency also faces issues such as anonymity and traceability).

The third is to strengthen monetary policy. Negative interest rates can be applied to the central bank's digital currency, so the central bank's digital currency can effectively overcome the zero interest rate lower limit of monetary policy, and the central bank's digital currency interest rate can be used as a new tool to further enrich the monetary policy toolbox. In the case where the public generally owns the central bank's digital currency account, the central bank can easily achieve "helicopter money".

The fourth is to strengthen financial stability and reduce the moral hazard of banks by reducing the role of banks in currency creation, and at the same time recover part of the coinage tax from banks. This is based on the premise that the central bank's digital currency can replace most or all of the bank's demand deposits.

For the above four advantages of the central bank's digital currency, in addition to the first one, the remaining three are still controversial. The second controversy has gone beyond the scope of payment efficiency, monetary policy and financial stability. Regarding the third item, economists who support negative interest rate policies may agree that “the central bank's digital currency can overcome the lower limit of zero interest rate”, but most economists do not support enriching the monetary policy toolbox with central bank digital currency interest rates or through central bank digital The point of view of currency "helicopter spreading money". Most economists do not recognize the fourth advantage.

The main risks and problems of central bank digital currency: bank disintermediation

One of the biggest risks of retail central bank digital currency is that the central bank directly issues digital currency to depositors, which may cause the bank to disintermediate the traditional financial medium, including both the structural disintermediation of the bank during the normal economic operation and the crisis. Bank runs, that is, periodic disintermediation.

During the normal economic period, the central bank's digital currency will take advantage of the central bank's unfair competitive advantage to absorb deposits, resulting in the bank's structural disintermediation and negatively affecting credit allocation, thereby affecting economic efficiency. Specifically, the central bank's replacement of digital currency notes (denoted by CBDC1) and the replacement of bank demand deposits (denoted by CBDC2) have different effects. CBDC1 only converts one form of central bank currency into another form. The balance sheets of central banks and commercial banks are unchanged, and their impact is neutral. CBDC2 will result in the reduction of bank demand deposits (this is the bank's main source of low-cost funds, see Table 1), thereby forcing banks to switch to other sources of higher-cost funds and increase financing costs. Under such circumstances, if the central bank wants to keep the financing environment of the real economy unchanged, it must cut interest rates. In addition, the reduction in demand deposits, banks have to switch to other forms of liabilities, will also have a certain impact on banks to meet liquidity regulatory requirements.

At the same time, CBDC2 may strengthen the role of the central bank in the allocation of credit resources. If the central bank's allocation efficiency is not as good as that of the private sector, it may cause a decline in the overall economic efficiency. When CBDC2 is large enough, it may cause credit concentration problems. And allowing central banks to participate in more market sectors may also mean a greater degree of administrative intervention.

During the crisis, for depositors, holding the risk-free central bank digital currency issued by the central bank may be more attractive than bank deposits, which may increase the risk of bank runs and expand the impact of the crisis. Relevant data from the Eurozone shows that during the 2008 international financial crisis and the European debt crisis, large amounts of bank deposits flowed from weak banks to safer banks or non-bank financial institutions. For example, the issuance of central bank digital currency by the central bank will undoubtedly provide a safer and more attractive flow of safe-haven funds, thereby exacerbating the possibility of run-offs by problematic banks. In this case, the effective flow of credit to the economy may also be impaired. The retail central bank digital currency is open to all the public. Therefore, compared with the wholesale central bank digital currency, the problem of exacerbating bank run-off risks will be more prominent.

The method of regulating the amount of central bank digital currency in the literature

In order to avoid the problems of structural disintermediation and exacerbating run-off risks in the crisis, the issuance of central bank digital currency should not only focus on improving payment efficiency, but also ensure that central bank digital currency is not used as the main value storage method, so the amount of central bank digital currency must be reasonably regulated .

- Four core principles for controlling the number of central bank digital currencies (Kumhoff and Noone (2018))

Principle 1: Implement floating interest rates on central bank digital currencies.

Unlike cash, non-zero interest rates are applied to the central bank's digital currency, and the exchange rate of the central bank's digital currency and other forms of currency is regulated through floating interest rates. Barrdear and Kumhof (2016) also proposed that the interest rate of the central bank's digital currency can be used as an independent monetary policy tool. For example, the implementation of negative interest rates on the central bank's digital currency helps to avoid a large number of bank deposits being converted into digital currency when there is a systemic risk in the banking industry. .

Principle 2: Separate the central bank digital currency from the bank reserve, and the two cannot be converted to each other.

By establishing this principle, it is possible to clearly distinguish the different goals and functions of bank reserves and central bank digital currency while strengthening financial stability, that is, the central bank digital currency cannot be used as an inter-bank settlement asset, nor is it subject to real-time full payment system (RTGS ) Rule constraints. In addition, the principle also prevents depositors from converting large amounts of bank deposits into central bank digital currency.

Principle 3: Commercial banks do not promise to convert deposits to central bank digital currency on demand.

This principle implies that the exchange of central bank digital currency and bank deposits should rely on the central bank. If the exchange of central bank digital currency and bank deposits is all undertaken by commercial banks, when a small amount of bank deposits is converted into central bank digital currency, commercial banks may be competent; but when a large amount of deposits are converted into central bank digital currency, banks need to sell to central bank Or repurchase qualified assets to obtain more central bank digital currency to meet the exchange needs. For this reason, the central bank may have to expand the list of qualified asset collaterals, thereby increasing the risk borne by the central bank's balance sheet.

Principle 4: The central bank only issues central bank digital currency by exchanging qualified securities.

This principle can to the greatest extent avoid the risk of the central bank's balance sheet issued by the central bank's digital currency. The central bank issues the central bank digital currency by exchanging qualified securities such as government bonds, which can realize the management of the central bank digital currency in the same way as the reserve in the balance sheet.

Although the above four principles aim to minimize the impact of central bank digital currency on the existing financial order, they will greatly change the current currency issuance and exchange rules. Taken together, these suggestions have some positive significance, but still need to find a more reasonable plan.

- Set a central bank digital currency holding limit (Panetta (2018))

Panetta (2018) proposed to solve the structural disintermediation and bank run problems related to central bank digital currency by "setting a holding limit for each central bank digital currency holder." Technically, the central bank digital currency based on distributed account book technology can easily set the upper limit for each account, that is, the transfer instruction beyond the limit will be rejected. However, the existence of the limit may cause the payer to fail to pay due to exceeding the limit, or the recipient's account has reached the upper limit and cannot receive payment. This not only causes payment uncertainty, reduces customer experience, but also greatly reduces payment efficiency.

Central bank digital currency with double interest rate system helps solve the problem of bank disintermediation

Kumhof and Noone (2018) have proposed that the implementation of "unattractive" interest rates or negative interest rates on central bank digital currencies may solve the structural and cyclical disintermediation problems caused by central bank digital currencies, but they have Whether it is effective is skeptical. Panetta (2018) also proposed to establish a layered system for the central bank's digital currency to solve the bank run problem, but did not specify that the second-tier interest rate is a negative interest rate.

Designing a reasonable double-layer interest rate system for central bank digital currencies, that is, setting two interest rates for different central bank digital currencies, can better control the number of central bank digital currencies, thereby helping to resolve bank disintermediation issues related to central bank digital currencies. The central bank digital currency can be distinguished according to different uses, with the central bank digital currency used for daily payment as the first layer and the central bank digital currency used for value storage as the second layer. This two-tier interest rate system is similar to the current operation of the European Central Bank, the Swiss Central Bank, and the Japanese Central Bank to set two or more interest rates for excess reserves. Therefore, the central banks have accumulated rich experience in this regard. It can be used in the design of the central bank's digital currency layered interest rate framework.

The central bank digital currency with double interest rate system has many advantages. First, by setting an unattractive interest rate for the second-tier central bank digital currency, it can avoid a large amount of central bank digital currency used for investment. Since the central bank should not be the main investment intermediary in the economic operation, the central bank digital currency should not be the main form of investment in the household sector, so it is not encouraged to exist a large number of central bank digital currencies in the form of value storage means. Second, because the first-tier central bank digital currency is mainly used for daily payments, even if the interest rate is very low, it will not lose its attractiveness to the holders. Therefore, it can in principle ensure that the central bank digital currency has certain appeal to all household sectors . Third, the double-layer interest rate system can better control the amount of central bank digital currency and improve manageability, thereby increasing confidence for the central bank to issue and manage central bank digital currency. Fourth, the two-tiered interest rate system allows the central bank to reduce the interest rates of all central bank digital currencies to negative numbers during times of crisis, thereby avoiding widespread public criticism of central bank policies. When the central bank introduces the central bank digital currency, the central bank can make it clear to the public: the central bank does not intend to set an attractive interest rate for the second-tier central bank digital currency, and the central bank may Interest rates are adjusted to make them less attractive; at the same time, the central bank can promise to never implement negative interest rates on the first-tier central bank digital currency. Fifth, if you want to abolish paper currency while issuing central bank digital currency, then the central bank digital currency of the two-tier interest rate system can overcome the problem of the lower limit of the nominal interest rate of traditional monetary policy when needed, and also guarantee the interest rate of the first-tier central bank digital currency Do not reduce to a negative interest rate, thereby taking into account the fairness of the low-income group and the central bank's currency payment function in a broader sense.

The central bank can set a maximum number of digital currencies for the first-tier central bank. For example, the European Central Bank can set the upper limit of the first-tier digital currency holding to 3000 Euros per capita, which means that the total amount of the first-tier central bank digital currency held by the household sector is about 1 trillion euros (assuming eligible euros The population of the district is about 340 million, and the limit allowed for minors can be set to zero, or it can be placed in the digital currency account of their parents' central bank). Let's estimate: the number of banknotes in circulation in the euro area is slightly more than 3000 euros per capita (a total of about 1.2 trillion euros), and the holdings of securities in the euro area system (including portfolios and portfolios of policy instruments) are about 3 trillion Euro, the excess reserve of the banking system is close to 2 trillion euros. If everything else remains the same, immediately issuing 1 trillion euros of central bank digital currency does not require banks to carry out large-scale credit operations. The central bank can even raise the first-tier central bank digital currency limit when the number of paper currency in circulation decreases. 3000 Euros can basically cover the average monthly net income of households in the euro area, so it can cover the payment function of currency. Since the first-tier central bank digital currency mainly serves the daily payment of the public, the first-tier central bank digital currency limit for enterprises (including financial enterprises and non-financial enterprises) may not need to be too high, or even zero. When estimating how many first-tier central bank digital currency limits will be converted to central bank digital currency, on the one hand, it is necessary to consider that not all households will open a central bank digital currency account, even if they open an account, they may not hold the upper limit of central bank digital currency On the other hand, some families may be willing to hold the second-tier central bank digital currency.

For non-bank financial institutions and non-financial enterprises, the upper limit of the first-tier central bank digital currency can be set to zero, or calculated according to a certain percentage according to their payment needs. It is important to pay attention to keeping the distribution concise and controllable. If foreigners are allowed to open central bank digital currency accounts, then their first-tier digital currency cap should also be zero. In addition, the account-based central bank digital currency framework can in principle be supplemented by the token-based central bank digital currency. The token-based central bank digital currency should implement the second-tier central bank digital currency interest rate. General stored-value cards are sufficient to meet the needs of foreign tourists to use central bank digital currency without an account. Of course, these stored-value cards should also implement the second-tier central bank digital currency interest rate.

In principle, a relatively attractive interest rate r1 can be set for the digital currency of the first-tier central bank. The highest r1 is equal to the excess reserve interest rate and the lowest is zero. The second-tier central bank digital currency has a value storage function, so the second-tier central bank digital currency interest rate r2 should be relatively unattractive. Even considering the risk premium factor, r2 should not exceed the bank deposit interest rate or other short-term financial asset returns rate. The double-layer interest rates of central bank digital currencies are not policy interest rates, and the regulation of double-layer interest rates aims to stabilize and control the motivation and quantity of holding central bank digital currencies. Normally, the double-layer interest rate of the central bank's digital currency can be synchronized with the policy interest rate; during a crisis, when the policy interest rate is close to the lower limit of zero, special measures can be taken: by promising that the first-tier central bank digital currency interest rate r1 will never be negative, reducing the public's The criticism of banks' negative interest rates; meanwhile, the second-tier central bank digital currency interest rate r2 was adjusted to be negative to reduce the impact on bank deposits.

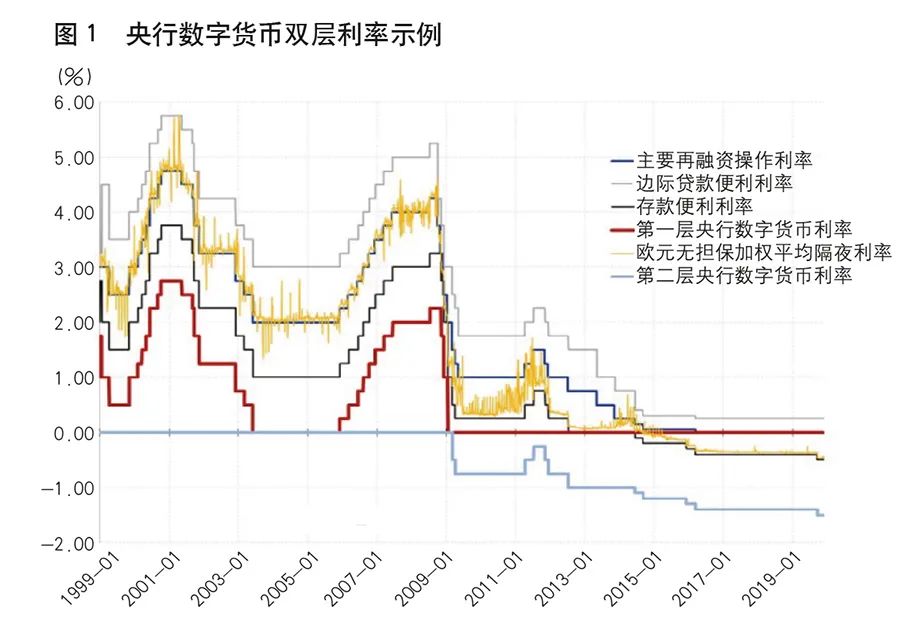

Taking the European Central Bank as an example, the two-tier interest rate design of the central bank's digital currency can consider the following framework: If the European Central Bank's Deposit Interest Rate (DFR) is used as a reference, the two-tier interest rate of the central bank's digital currency can be set to r1 = max (0 , iDFR-1%); r2 = min (0, iDFR-1%) (see Figure 1).

Of course, you can also refer to other interest rates other than the deposit convenience interest rate, only focusing on the interest rate difference with the deposit convenience interest rate. If you are worried that the central bank's digital currency usage rate is not high, you can appropriately reduce the interest rate difference with the deposit convenience rate. For example, set the two levels of central bank digital currency interest rates to r1 = max (0, iDFR-0.5%); r2 = min (0, iDFR-0.5%). If you are worried that the success of the central bank's digital currency may lead to structural and periodic disintermediation of the banking system, you can consider setting r1 = max (0, iDFR-2%); r2 = min (0, iDFR-2%) . If you want to ensure that the first-tier central bank digital currency is attractive, and at the same time worry about the disintermediation problems that may be caused by large-scale central bank digital currency, you can consider setting r1 = max (0, iDFR); r2 = min (0, iDFR -2%).

In general, the above framework can be modified according to the actual situation, but the upper limit of the per capita digital currency of the first-tier central bank should remain unchanged and the interest rate cannot be negative. For example, during periods of extreme crisis such as the collapse of Lehman Brothers, the second-tier central bank digital currency interest rate may be temporarily reduced to -5%, or even as low as -10%.

It should be pointed out that the central bank digital currency may have a profound impact on the financial system. This effect is independent of the nominal amount of the central bank digital currency to a certain extent, but it may affect the competitiveness of banks in the financial system. Therefore, even if the central bank digital The amount of money is well controlled, and it cannot be asserted that the problem of bank disintermediation can be completely eliminated. ■

(This article is compiled from the author's working paper "Tiered CBDC and the financial system")

about the author:

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Opinion | Zhongjing Jinchuang Zheng Runxiang: RMB internationalization should establish a mechanism for applying RMB digital currency in the field of commodity trading

- The People's Bank of China: unswervingly promote the research and development of legal digital currency

- Blockchain Application Case: Eliminating Hype

- Viewpoint | Cheng Xiaoming, "Godfather of the New Three Boards": What are the pain points of enterprises that can be solved by blockchain "chain reform"

- What can a blockchain do for various companies?

- Blockchain changes production relations? Big data is not ready to serve as a means of production

- How does blockchain help security on the tip of the tongue?