Has Financialization Destroyed NFTs?

Financialization's Impact on NFTsAuthor: OVERPRICED JPEGS Translator: Huohuo/Baihua Blockchain

Many people consider the financialization of NFTs as a sign of market maturity. Some believe that this will open the doors to larger and more mainstream participants. But is this really the case?

As early as 2021, things were quite simple.

- zkSync Development Diagnosis Progressive Decentralization Path, Still in Early Stage with Lack of Distinctiveness in the Ecosystem

- How much can you earn working at Coinbase in a bear market? Take a look at these 6 popular positions.

- Explaining in detail the newly launched Deals feature by Opensea The ‘barter’ of the NFT world

People actually bought NFTs because they liked them, considering the price and rare features.

After buying, they joined Discord groups to connect with other holders: communities were formed, friendships were made. And in many cases, the prices of these NFTs increased.

Then the financialization started creeping into this mature market, and dynamics began to change.

Many people consider the financialization of NFTs as a sign of market maturity. Some believe that this will open the doors to larger and more mainstream participants.

But is this really the case? At least for one major sector of the NFT market – the PFP sector – it seems that financialization has ruined a lot of what we knew about NFTs.

The rise of NFT financialization has caused a decline in the PFP market

Let’s explore this paper by studying the financialization of NFTs, its impact on the market, including cross-market and transactional innovations, token incentives, lending, and the financialization of NFT perpetual rights/futures.

1. Advanced Trading Features

Main impact: Negative

The early stages of the previous cycle (as early as late 2020 – early 2021) in the NFT market were like the wild west.

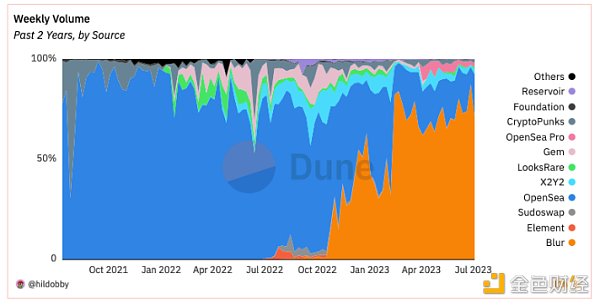

Back then, OpenSea was the king. It was a literal “open sea” of JPEGs, with almost no structure or organization, and can be considered the biggest winner of the 2021 bull market cycle, earning millions of dollars in transaction fees from billions of monthly trades.

This success brought competition, starting with LooksRare, then X2Y2, Gem and Sudoswap, and finally Blur.

OpenSea dominated NFT trading until Blur entered and took a share in an upward trend

This competition gave birth to new features implemented in the NFT market, enhancing the trading experience. There are too many to list, but some influential ones include:

1. Analytical charts and better data access

2. Massive NFT purchases (i.e., sweeping) and listings

3. Large-scale NFT sales through bidding acceptance

4. Real-time bidding and bid depth analysis

These features were popular at the time and continue to be popular now. But they were the first to start changing the way NFT traders and collectors view JPEGs.

The once unique digital collectibles, with characteristics and functions that connect with and value the holders, are beginning to transform into digital assets on screens.

Their non-fungibility is disappearing, gradually becoming replaceable.

<p"Sweeping" can be said to be the first function that NFTs have taken on this path.

One-time bulk purchases of NFTs have changed the shopping experience, and the ability to bulk sell has also changed the selling experience.

Although “sweepers” are often cheered on in NFT Discord, savvy holders soon realized the problem – most “sweepers” are more likely to become sellers, etc. They don’t care about which NFTs they own – they are all just tokens for buying and selling.

Therefore, while these functions have improved the trading experience, the experience of collecting and holding the underlying assets has begun to deteriorate. The net impact of these transactional advancements is negative, even if they have not been fully realized at the time.

But compared to the impact of competition in the secondary market, the impact of advanced transactional features is relatively insignificant: token incentives.

II. Token Incentives

Maximum Impact: Negative

Most PFP projects have already died out by the end of 2022. Those who have stayed seem to be the ones who will succeed.

The new class is led by the Bored Ape Yacht Club (BAYC), followed by Azuki, Doodles, Moonbirds, and Clone X, each with their own unique and powerful communities.

BAYC, in particular, was close to the status of Van Gogh’s goods. However, everything changed in February 2023.

Blur announced its airdrop and the second season. Early users were rewarded with $BLUR tokens through the airdrop, providing a $275 million stimulus to the market.

The $BLUR airdrop was initially widely celebrated, but then market sentiment started to change.

As stimulus measures flowed back into the PFP market, prices rose for several weeks in a row. In addition, the commitment of an additional $300 million airdrop attracted new (seemingly DeFi-native) traders into the field.

Blur kept things running by announcing incentives for the second season. Participants could earn points by listing and bidding on NFTs. Naturally, savvy users figured out how to exploit this system to make money.

Users did not receive rewards for purchasing NFTs, nor did they receive points once their bids were accepted, so the game became: keep the highest bid possible without being accepted.

This indicates that these users don’t really want the NFTs, they just want to accumulate bidding points for the $BLUR token.

This issue became even more apparent in the BAYC market after the legendary Bored Ape trading by famous trader/founder/OSF and Mando, with 71 BAYC sold for 5,545 ETH (worth $9 million at the time) in just a few seconds.

The Blur holders just absorbed 71 Bored Ape Yacht Club (BAYC) NFTs that they didn’t want, and a chain reaction started. A group of users began using them to exchange points.

Potential buyers who were on the sidelines witnessed two things:

1) The same NFT being traded back and forth dozens of times

2) The price starting to decline

Users have already calculated that as long as they accumulate enough Blur points as offsets, they can afford acceptable losses in each transaction.

Due to insufficient external demand, this has led to a gradual decline in asset prices since February 2023 until today.

It is debatable why new buyers have not entered these ecosystems yet. Many people point out the lack of execution and foresight from the team and founders. There are certainly some merits to this argument.

But another driving factor — and perhaps the more important one — is that these NFTs, especially PFPs, are losing their mystique. Buying a floor-bored ape that has been traded back and forth dozens of times is no longer worth it.

Well-known NFT trader Cirrus used an analogy, comparing it to walking into a Rolex store and seeing a group of luxury collectors throwing Rolex watches at each other all morning. Do you want to buy those Rolexes? I wouldn’t.

As a result, potential buyers are staying on the sidelines and not willing to buy assets that require “mass planting”.

As this process unfolds, the early features that attracted many people to the PFP market (traits recognition, buying NFTs worth taking pictures of, entering communities) are eroded and no longer appealing.

Since the introduction of token incentives by Blur, PFP prices have been declining, chart: NFT statistics

PFPs have become tokens to trade in order to accumulate $BLUR tokens. Their non-fungibility further deteriorates, which is why I gave a net rating of “negative impact” to token incentives in the market.

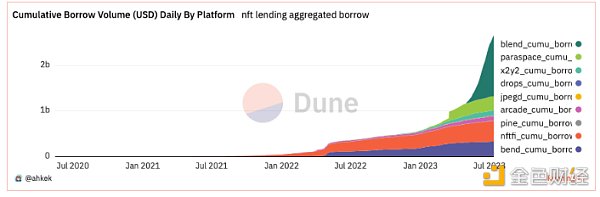

III. Non-Fungible Token (NFT) Loans

Major Impact: Positive

As the market war continues to brew, a new financial sector is taking off: NFT lending.

The NFT lending market surpassed $1 billion in cumulative trading volume in April this year, and recently surpassed the $2 billion mark in June after Blur launched its Blend platform.  It took 2 years for NFT lending to reach $1 billion, and then it took 3 months to reach $2 billion. NFTfi, which was launched in the spring of 2021, reached a trading volume of approximately $400 million by the end of 2021.

It took 2 years for NFT lending to reach $1 billion, and then it took 3 months to reach $2 billion. NFTfi, which was launched in the spring of 2021, reached a trading volume of approximately $400 million by the end of 2021.

This product is quite simple. NFT holders use their assets as collateral with the desired loan conditions, and lenders make offers against these NFTs. If the NFT holders like the terms, they accept the transaction, receive WETH, and custody the NFTs. If the loan is repaid on time, the holder can retrieve the NFTs; otherwise, the lender will receive the NFTs.

Then challengers enter the scene, including other peer-to-peer lending protocols like Arcade.xyz and pool protocols like BendDAO and JPEG’d. The loan terms are longer, and the annual interest rates are lower.

Soon, NFT holders have multiple options as long as the asset value stays above a certain liquidation threshold, and new participants like BendDAO will launch loans without repayment dates.

Then in May 2023, Blur introduced the Blend program, adding loans and a form of option market (buy now, pay later) to its protocol and providing token incentives for loans.

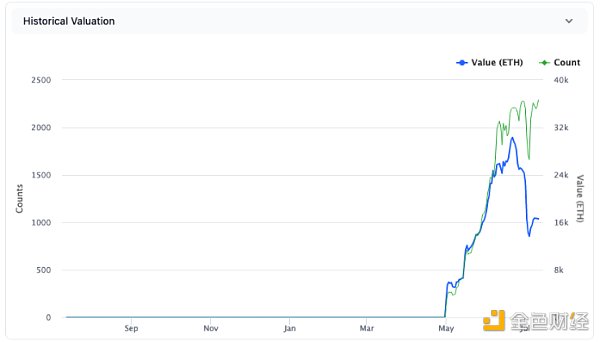

The loan-to-value (LTV) ratio increases, and the annual interest rate drops to 0. More leverage enters the system, which becomes increasingly evident before the recent Azuki Vegas party, Elementals minting disaster, and subsequent PFP liquidation cascade.

The net value of NFT assets in the Blur mixed wallet shows a significant decline after the minting of elements.

While some may see NFT lending as a potential negative impact, as leverage often ends in disaster (especially for inexperienced and overexposed traders), it is more like a positive factor for me.

Being able to borrow against NFTs for liquidity makes it easier to hold onto the NFT for a longer time.Protocols like NFTfi, Arcade, and even Zharta allow specific quotes for specific NFTs, based on attributes, rarity, etc.It does have value in the lending process.

Non-fungibility is actually rewarding. It feels like a victory, so my evaluation of NFT lending is positive.

Unfortunately, the next category is not as favorable.

Four, NFT perpetuals, options, and futures

Biggest impact: Negative

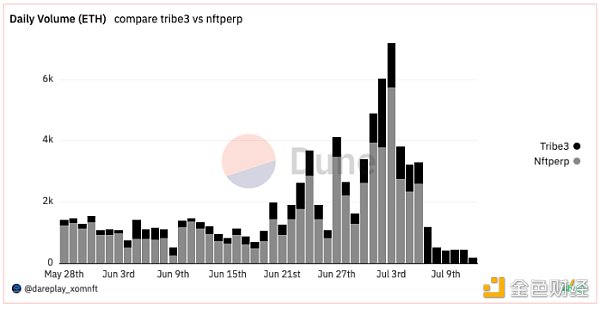

It can be said that at least in the NFT bear market, the hottest new trend in financialization is the ability to go long or short NFTs through perp protocols like NFTperp and Tribe (peer-to-peer protocol) and Wasabi (peer-to-peer).

Perpetuals and futures allow traders to bet on future prices of assets, often using leverage. For example, NFTperp allows users to get up to 10x leverage in trades (meaning a 1 ETH bet is equivalent to 10 ETH in size). The difference between perpetuals and futures is that perpetu

NFTperp dominates the NFT futures market, but may be too close to the sun.

To quickly understand how these protocols work, the perp protocol uses virtual automated market makers (vAMMs) to allow traders to take long (betting on price increase) and short (betting on price decrease) positions on NFTs. As described by the famous crypto thought leader 0xFoobar, vAMMs operate similarly to Uniswap V2 pools, but without any actual liquidity. They simulate liquidity and move prices up and down algorithmically based on long/short trading volume.

This product allows:

1) Holders to hedge the decrease in value of their NFTs by opening short positions;

2) Those who do not have enough funds to buy NFTs (such as 35 ETH for BAYC) to bet on their increase by opening long positions with any amount;

3) Those who believe that NFTs will decrease in value to bet on the trend by shorting.

All 3 use cases make sense and have a place in comprehensive trading strategies for active traders. However, these types of trades and this underlying model have limitations that can be tested in extreme market events – NFTperp has just discovered this.

NFTperp recently unexpectedly shut down its platform, shocking the market, citing its accumulated bad debt as the cause of $518 million in futures trading volume. They shared some details of the events that occurred, but it appears that the massacre of the NFT market after the Azuki Elementals mint and the subsequent liquidation led to a surge in short trading volume on NFTperp, causing an impact that the system was not ready to absorb.

This leaves only Wasabi and Tribe as remaining protocols for the short market.

In the weeks leading up to and following the Azuki party and mint, Perps trading volume skyrocketed, impacting NFTperp in the process.

Overall, this is the newest and least mature NFT financial market, and some, like 0xFoobar, believe that NFTs are fundamentally doomed to fail (which is worth mentioning).

But one thing is clear – in all the financial aspects discussed so far, perpetual equity and futures may be the least favorable for maintaining non-fungibility.

Literal price (more precisely, vAMM oracle price) is the most important. The entire community and collection are reduced to numbers on the screen. Mid-level and rare items are not important. All bets are related to changes in the literal price.

Therefore, I give a negative rating to NFT Perps, options, and futures.

Conclusion

The points presented here are mainly focused on the NFT PFP field, as Art Blocks and the broader digital art market, as well as other NFT areas such as gaming and metaverse, are largely unaffected by token incentives and Perps (although if Art Blocks were added to Blur as outlined in the early roadmap circulated by Blur, they would likely be affected).

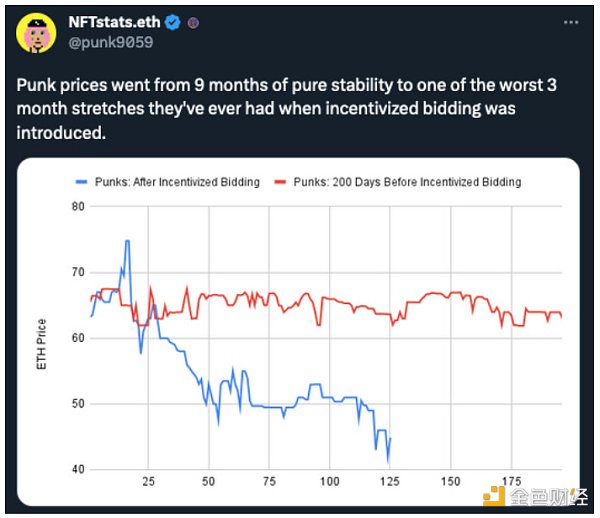

Interestingly, the Art Block Index has slightly increased over the past year, while the PFP Index has declined by over 50%.

Perhaps the most compelling evidence is the CryptoPunks market, which maintained a stable fluctuation of 10% for 200 days before experiencing extreme volatility for 120 days, with fluctuations ranging from 15% to -40%.

But even this chart is controversial.

The ultimate test will be to add Chromie Squiggles to Blur and conduct incentive bidding to see how they perform in the next 6-12 months. Perhaps we will see this happen in the near future (although it seems less likely than before).

In summary, evaluating the financialization of NFTs’ impact on the PFP industry:

❌ Advanced trading – negative

❌ Token incentives – negative

✅ NFT lending – positive

❌ Futures, perpetual bonds, and options – negative

As the non-fungible token market matures, we are beginning to see how various functionalities and mechanisms affect this new market. Many of these functionalities and mechanisms have had significant unforeseen impacts (e.g., Blur airdropping $300 million and paying traders’ bids, resulting in a 50% market decline). However, most of these financial innovations have eroded the non-fungibility of NFTs.

The elimination of non-fungibility has had a negative impact on collectors’ desire to hold these assets, which is also reflected in the market.

Unfortunately, the damage that has been done to this market may be irreversible, and the possible outcome is that existing PFP collections will never see new ATHs or valuations close to previous highs.

Perhaps our early NFT market did not need such a degree of financialization. Perhaps new innovations will revive non-fungibility.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Arweave’s total number of transactions has exceeded 1 billion. How will it move towards large-scale applications in the future?

- Left or Right North Korean Hacker Group and US SEC Chairman

- Buidler DAO How Tokens Drive Growth from the Blur Airdrop Strategy

- Opinion The true and complete Telegram Bots experience will appear on Ton.

- Variant Partner Distinguish DePIN and DeREN as two types of decentralized infrastructure networks.

- DePIN and DeREN Better Classification of Decentralized Infrastructure Networks

- After Unibot went viral, which other mainstream Telegram bots are worth paying attention to?