Popular science | Zou Chuanwei: Global stablecoins and central bank digital currencies

Source: Wanxiang Blockchain

On November 21st, Dr. Zou Chuanwei, Chief Economist of Wanxiang Blockchain and PlatON, introduced the global stablecoin and central bank digital currency in detail in the open class of Wanxiang Blockchain Hive Academy. This article is the content of the fourth lecture of the open class, which was edited by the speaker Dr. Zou Chuanwei.

My topic today is "Global Stable Currency and Central Bank Digital Currency." Global Stablecoin is the term used in the report of the G7 Stablecoin Working Group in October this year, which is mainly aimed at the Libra project. My speech is divided into four parts: one is to explain the origin and origin of the problem; the other is to discuss the account paradigm and token paradigm of the financial infrastructure; the third is to analyze the Libra project; the fourth is to analyze the DC / EP of the People's Bank of China.

Eleven years ago, Satoshi Nakamoto wrote in the Bitcoin white paper:

- Trend analysis: The transaction volume of the Bitcoin chain exceeds the on-chain, and the main application scenarios tend to be centralized

- Ripple has completed the final USD 20 million investment in MoneyGram, with a total investment of USD 50 million

- Are Bitcoin miners still mining in 2140?

It can be seen that he envisages Bitcoin as a peer-to-peer electronic cash. The transaction does not depend on financial institutions. Through technical proofs such as proof of work, hash functions and digital signatures, it will not be "double-spend" and historical records will not be tampered with.

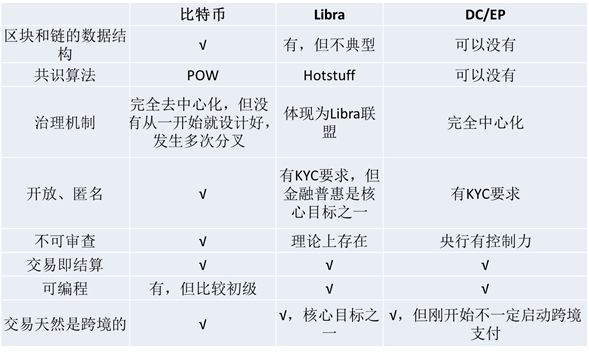

10 years have passed. What problems did Bitcoin solve and what problems did it not solve? Bitcoin introduces the concept of blockchain. Bitcoin is the first application of the blockchain, and in a sense it is also the most successful application to date. The blockchain has several points: 1. The data structure of the block and the chain; 2. The consensus algorithm; 3. The governance mechanism under decentralization; 4. Openness and anonymity; 5. Uncensorable; 6. Transaction is settlement; 7. Programmable; 8. Transactions are naturally cross-border. However, the high price fluctuations have prevented Bitcoin from becoming an effective payment tool. At present, the market more regards Bitcoin as a digital gold, and gold has long exited the circulation field and no longer assumes currency functions.

The blockchain field has tried a variety of methods to stabilize the price of cryptocurrencies. The first is to expand the scope of use. However, in theory, whether the expansion of the scope of use can stabilize the price of cryptocurrencies has been controversial; in practice, the issue of expanding the scope of use and stabilizing the price of cryptocurrencies also has "chicken first, or eggs first". The second is to expand the block capacity, ease congestion on the chain, and improve the user experience. The Bitcoin Cash example shows that this method cannot stabilize prices. The third is "algorithmic stablecoin" which uses algorithms to adjust supply. This method is also difficult to succeed because the demand for cryptocurrencies has many influencing factors and the changes are very complicated, no matter how complicated the algorithm is, and it is difficult to make supply and demand perfectly respond to changes in demand to stabilize prices. The fourth is to issue stablecoins with risk assets as collateral. This method works on a small scale, but scalability is questionable. Fifth, stable currency was issued with fiat currency assets as reserves. Tether / USDT and its predecessor Realcoin (launched in 2014) adopted this approach. Although USDT is very non-compliant, as the largest and most widely used stablecoin at present, this direction has proved feasible and the relevant demand is strong.

The issuance of stablecoins with fiat currency assets as a reserve is a methodological dichotomy: on the one hand, the blockchain is used as a financial infrastructure to take advantage of the characteristics of transactions as settlement, programmable settlement, distrust, and openness and anonymity; on the other hand, Tokens are linked to off-chain value using economic mechanisms. From a practical point of view, no matter whether it is the use of the blockchain or the economic value linkage mechanism, various forms have appeared.

Financial infrastructure is divided into account paradigm and token paradigm. The former is represented by the bank account system and the latter is represented by the blockchain. These two paradigms are very different, but both can be used to carry financial assets and transactions, presenting very complex substitution and complementary relationships in many application scenarios.

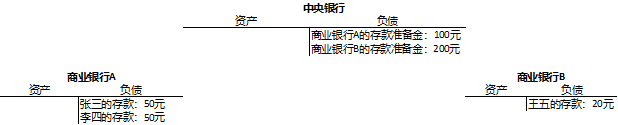

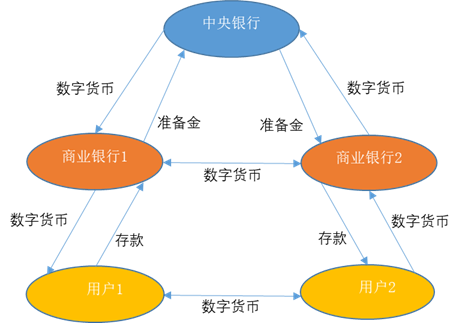

Individuals, enterprises and government departments open deposit accounts with commercial banks, and commercial banks open deposit reserve accounts with central banks. Fiat money exists on the debtor side of the financial system. The base currency is the liability of the central bank. Among them, cash is the central bank's liabilities to the public, and deposit reserves are the central bank's liabilities to commercial banks. Deposits are liabilities of the central bank to individuals and businesses. In modern economies, cash accounts for only a small percentage of the money supply, and most of the broad money supply is deposits. Currency forms such as reserve requirements and deposits have all been digitized.

Figure 1: Secondary bank account body

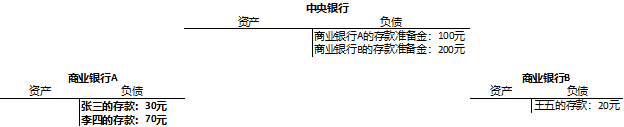

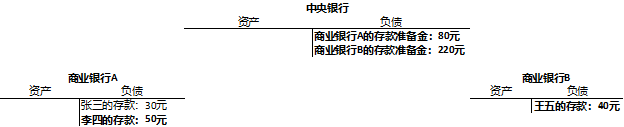

In cash transactions, as long as both parties to the transaction confirm the authenticity of the cash, they can deliver without the need for a trusted third party. This is similar to Token trading. Transfers and remittances involve bank account operations. For example, for peer transfers, the balances of the deposit accounts of the two parties in the same bank must be adjusted simultaneously. In addition to adjusting the balance of the deposit accounts of the two parties in the respective banks, the inter-bank transfer also involves settlement between the two banks. Settlement between commercial banks requires adjustments to their reserve account balances with central banks. Figure 2 is a simple example.

(Peer transfer: Zhang San transfers 20 yuan to Li Si)

(Inter-bank transfer: Li Si transfers 20 yuan to Wang Wu)

Figure 2: Currency transactions

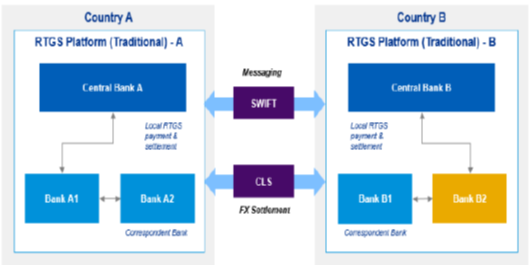

Bank account operations involving cross-border payments are more complicated. Figure 3 is taken from the 2018 research report "Bank of Canada, Bank of England, and Monetary Authority of Singapore" by Bank of Canada, Bank of England and Monetary Authority of Singapore (Bank of Canada, Bank of England, and Monetary Authority of Singapore, 2018), which is on page 28 of the report Figure 1.

Figure 3: Cross-border payments

Suppose two countries, country A and country B, and their respective currencies-currency A and currency B. In both currencies, payment systems were established by the respective central banks (RTGS in Figure 3, the real-time full payment system). For example, the RMB is a large and small payment system and a cross-border payment system (CIPS), the US dollar is the Federal Electronic Funds Transfer System (Fedwire) and the New York Clearing House Interbank Payment System (CHIPS).

Suppose Alice, a resident of country A, has a deposit in currency A in a bank A1 in country A. She wants to pay Bob, a resident of Country B, who has a B currency deposit account at a bank B in Country B. The problem is that there is no direct business relationship between Bank A1 and Bank B2. Therefore, it is necessary to introduce a correspondent bank (bank A2 and bank B1 in FIG. 3). The correspondent bank acts as a bridge between banks A1 and B2, but lengthens the cross-border payment chain.

Under the agency banking model, cross-border payments are made as follows. First, in country A, Alice's A currency deposit in bank A1 is transferred to bank A2 (through the A currency payment system). Second, funds are transferred from bank A2 to bank B1. The correspondent banks open accounts with each other. For example, from the perspective of bank A2, the account it opens at bank B1 is called a nostro account (in B currency), that is, a foreign interbank account. The account opened by bank B1 in bank A2 is called a vostro account (in A currency), which is an interbank deposit account. Funds are transferred from bank A2 to bank B1 by adjusting these account balances. Currency exchange requires a continuous connection settlement system (ie CLS in Figure 3). Finally, funds are transferred from bank B1 to bank B2 (through the payment system of B currency).

Two points need to be explained: First, unlike popular perception, the Global Interbank Financial Telecommunications Association (SWIFT) is an interbank messaging system that handles the flow of information in cross-border payments. The flow of funds in cross-border payments occurs through the bank account system. Second, some blockchain projects believe that SWIFT is the main reason for the high cost of cross-border payments. But in fact, it's not. McKinsey's 2016 research shows that the average cost of a U.S. bank to make a cross-border payment through a correspondent bank is $ 25- $ 35, which is more than 10 times the average cost of a domestic payment. Among them, 34% of the cost comes from liquidity locked in the correspondent bank account (because these funds could have been used in places with higher returns), 27% comes from treasury operations, 15% comes from foreign exchange operations, and 13% From compliance costs.

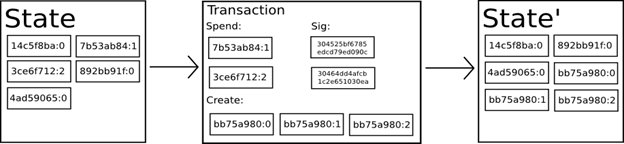

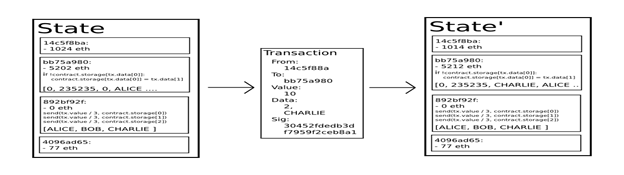

Token is essentially a state variable defined in the blockchain (Figure 4). Tokens defined according to the same rules are homogeneous and can be split into smaller units. Asymmetric encryption can guarantee the anonymity of Token holders. Tokens can be transferred between different addresses. The blockchain consensus algorithm and non-tamperable features can guarantee that the Token will not be "double spent". The total amount remains the same during the Token transfer process-the gain of address A is the loss of address B. The status (ledger) update and transaction confirmation are completed at the same time, and there is no settlement risk. Confirmed transactions are public and cannot be tampered with throughout the network. Token transactions in the blockchain do not need to rely on a centralized trust institution.

(Source: Ethereum White Paper)

Figure 4: Token and its transactions

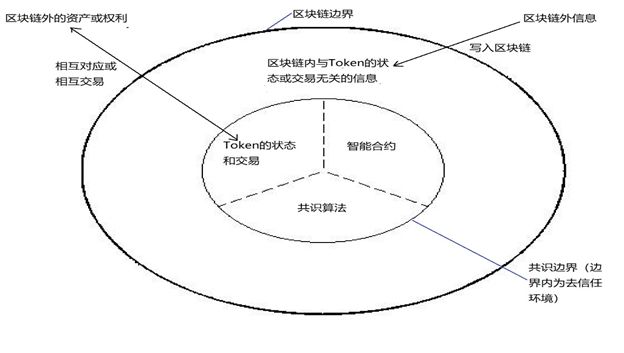

Figure 5 summarizes the design of mainstream blockchains from an economic perspective. At present, mainstream blockchain systems, whether they are public or alliance chains, regardless of the UTXO model represented by Bitcoin or the account model represented by Ethereum, regardless of whether the scripting language is Turing complete or supports smart contracts, Regardless of whether or not a non-mainstream blockchain structure such as a directed acyclic graph structure (DAG) is adopted, it is economically consistent with the description in Figure 5.

Tokens, smart contracts, and consensus algorithms are all within the consensus boundary. There is an inseparable relationship between tokens and smart contracts. The consensus algorithm ensures a trust-free environment within the consensus boundary. Information that is not related to the status or transaction of the Token in the blockchain is outside the consensus boundary and within the blockchain boundary. There are two types of interactions inside and outside the blockchain: one is that the information outside the blockchain is written into the blockchain; the other is the mutual transaction or correspondence between tokens and assets or rights outside the blockchain.

Figure 5: Blockchain Token Paradigm

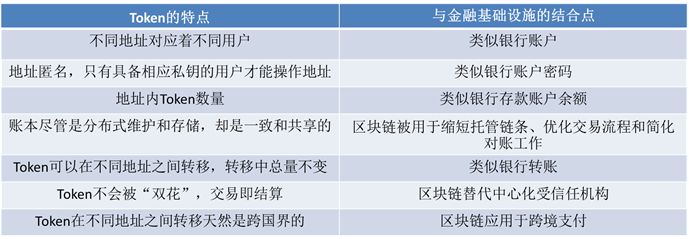

The following properties of Token and its transactions are the key to the application of blockchain to financial infrastructure (Table 1):

Table 1: Combination of Token Paradigm and Financial Infrastructure

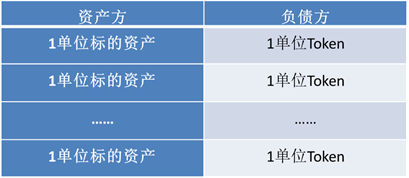

Token is a piece of computer code in its existence form, without any intrinsic value. So, what is the value source of Token? Token is generally translated into tokens or representations in Chinese. The mark or sign has no value in itself, and the value comes from the assets it carries. The use of Tokens to carry real-world assets (the so-called "asset on-chain") is essentially based on laws and regulations and uses an economic mechanism outside the blockchain to link the Token to the value of certain types of underlying assets. This process is inseparable from centralized trusted institutions (Table 2).

Table 2: Use Token to carry assets

There are three rules that must be followed to carry assets with Tokens. The first is the issuance rule : centralized trusted institutions issue tokens based on the underlying assets in a 1: 1 relationship. The second is the two-way exchange rule : a centralized trusted institution ensures a two-way 1: 1 exchange between the Token and the underlying asset. The user issues 1 unit of the target asset to the centralized trusted institution, and the centralized trusted institution issues 1 unit of token to the user. The user returns 1 unit of token to the centralized trusted institution, and the centralized trusted institution returns 1 unit of the underlying asset to the user. The third is the credible rule : the centralized trusted institution must be regularly audited by a third party and fully disclose the information to ensure the authenticity and adequacy of the underlying assets used as the reserve for token issuance.

Under the constraints of these 3 rules, 1 unit of Token represents the value of 1 unit of the underlying asset. When the Token has secondary market transactions, the market price of the Token will deviate from the value of the underlying asset, but the market arbitrage mechanism will drive the price to return to value. Once these three rules are not strictly adhered to, the effect of the market arbitrage mechanism will weaken, and the token price will be decoupled from the value of the underlying asset (not necessarily completely decoupled).

Some friends may ask, why should the Token paradigm be developed when the account paradigm is so developed? There is a big difference in privacy protection between the two. Opening an account generally requires approval and is therefore highly selective. In particular, personal bank and payment accounts must meet strict identity verification requirements. Financial accounts can generally guess the owner from the account name, but how much assets are in the account is only visible to people with relevant permissions. However, the collection and use of personal information under the account paradigm can easily become a violation of personal privacy. The blockchain is highly open to users. Anyone who has a pair of public and private keys based on a digital signature algorithm can own an address in the blockchain. The address has good anonymity, but the number of tokens in the address and the token transactions between the addresses are visible on the entire network and cannot be tampered with. Transaction with Token is like being covered by a layer of anonymity. Although this helps protect the privacy of address owners, it also makes it more difficult to regulate KYC ("Know Your Customer"), AML (Anti-Money Laundering), and CFT (Anti-Terrorist Financing). In short, both paradigms have their own pros and cons.

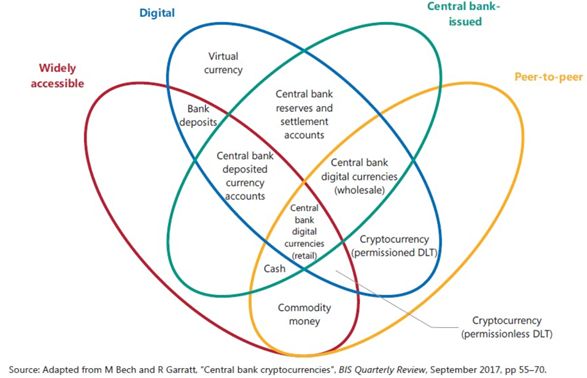

Figure 6 is the "Flower of Money" model proposed by the Bank for International Settlements for Central Bank Digital Currency (CBDC). Figure 6 compares CBDC with cryptocurrencies and bank accounts from multiple dimensions: is it account-based or token-based, is it only used between institutions or is it generally available, is it issued by a central bank, is it peer-to-peer, and so on.

Figure 6: BIS "Flower of Money" model

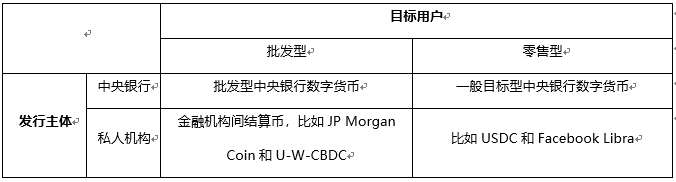

Table 3 focuses on the application of the Token paradigm in the field of fiat currencies and classifies them according to two dimensions. The first dimension is whether the issuer is a central bank or a private institution. The second dimension: whether the target user is wholesale (for institutions only) or retail (for the public).

table 3: Classification of Token Paradigm in Fiat Currency

There are 4 key concepts in this: 1. Tightly coupled accounts vs loosely coupled accounts, loosely coupled accounts and the Token paradigm are basically synonymous, but the Token paradigm does not necessarily depend on the blockchain; 2. Central bank issue vs private institution issue 3. A single currency reserve vs a basket of currency reserves; 4. Wholesale vs. general target. But no matter what kind of application, there are three elements: 1. The user interface, that is, how the user owns and uses; 2. The release and stability mechanism; 3. The transfer mechanism.

Table 4 compares the use of these applications for blockchain, and it is not difficult to see that there is a lot of flexibility in this regard.

Table 4: Different applications for blockchain

The first is the economic connotation : Libra is a synthetic currency unit based on a basket of currencies (50% of the US dollar, 18% of the euro, 14% of the Japanese yen, 11% of the British pound, and 7% of the Singapore dollar). The weighted average exchange rate between the price of Libra and this basket of currencies hook up. Although Libra does not anchor any single currency, it will still exhibit low volatility, low inflation, universal acceptance and fungibility.

The second is reserve assets : Libra issuance is based on 100% fiat currency reserves. These fiat currency reserves will be held by investment-grade custodians around the world and invested in bank deposits and short-term government bonds. The investment income of the fiat currency reserve will be used to cover the operating costs of the system, ensure low transaction fees, and pay dividends to early investors (the "Libra Alliance"). Libra users do not share the investment income of fiat currency reserves.

The third is the issuance and price stabilization mechanism : The Libra Alliance will select a certain number of authorized dealers (mainly compliant banks and payment institutions). Authorized dealers can trade directly with the fiat currency reserve pool.

The fourth is the underlying technology : Libra blockchain belongs to the alliance chain. Libra plans to recruit 100 verification nodes in the early stage and support 1000 transactions per second to meet the normal payment scenario. 100 verification nodes form the Libra Alliance, which is registered as a non-profit organization in Geneva, Switzerland.

Fifth, the governance structure : The governing body of the Libra Alliance is the board of directors, composed of member representatives, and each verification node can assign a representative. All decisions of the Libra Alliance will be made through the Board of Directors, and major policy or technical decisions require more than two-thirds of the members to vote.

Libra, as a unit of synthetic currency based on a basket of currencies, is a super-sovereign currency like the IMF's special drawing rights. Governor Zhou Xiaochuan has a profound elaboration on super-sovereign currencies.

During the issuance stage, Libra is based on 100% fiat currency reserves. Because it represents a basket of existing currencies, Libra has no currency creation function. The only way to expand Libra's issue is to increase fiat currency reserves. If Libra is widely circulated and there is a Libra-based deposit and loan activity, is there any money creation? We don't think so. This depends on whether the deposits derived from Libra loans (ie, the "50 Libra deposits from enterprises" at the bottom of Figure 7 belong to the account paradigm, not the Token paradigm) are considered currency. But it is certain that Libra represents a basket of currencies. There is no real monetary policy, and it is far from currency denationalization.

(Before the loan, the bank held 100 Libra)

(Banks lend 50 Libras to businesses)

(Business deposits 50 Libra to the bank)

Figure 7: Libra-based deposit and loan activities

Libra has valuable storage capabilities. However, because of the currency network effect and the fact that there are no goods or services denominated in Libra in reality, Libra's trading medium and pricing unit functions will be restricted in the early stages of Libra development. For example, when consumers use Libra to shop in a country, they may have to exchange Libra for local currency during the payment process. This affects payment efficiency and experience.

Libra can promote financial inclusion. According to the Libra Alliance, as long as a Calibra digital wallet is installed on the mobile phone, the user has the physical conditions to own and use Libra. Libra transaction fees are low. Members of the Libra Alliance have a rich industry background and a deeper understanding of user needs, which helps to flexibly embed Libra in many aspects of user life and improve the convenience of users using Libra.

In the lower right area of Table 3 to which Libra belongs ("Private Institution Issuance + Retail Type"), there have been many stable cryptocurrencies (such as USDC). These stable cryptocurrencies are mainly used in cryptocurrency exchanges and have not really entered the daily lives of ordinary people. Whether Libra can become a real payment tool remains to be tested by the market. One limitation that cannot be ignored is the performance of the Libra alliance chain. 1,000 transactions per second is definitely not able to support the daily payment needs of hundreds of millions of people. The Libra alliance chain has a plan to turn into a public chain. The public chain is more open, but its performance is more limited.

Libra's biggest controversy currently comes from currency substitution: In countries with political and economic instability and failure of monetary policy (such as high inflation), can Libra replace the currency of the country, thereby achieving a similar "dollarization" effect? This raises complex issues regarding currency sovereignty.

The Libra Alliance did not disclose the rebalancing mechanism of the Libra currency basket, the fiat currency reserve pool management mechanism, and the two-way exchange mechanism between Libra and the constituent currencies. Therefore, it is difficult to accurately analyze the market risks, liquidity risks and cross-border capital fluctuation risks facing Libra. Once the relevant information is disclosed in detail, we can analyze these types of risks and assess the corresponding prudential regulatory requirements. In particular, the rebalancing of the Libra currency basket is the biggest challenge facing Libra's economic mechanism design. At present, the following four risk points are relatively certain.

First, if Libra's fiat currency reserve pool implements a more aggressive investment strategy (such as investing in high-risk, long-term, or low-liquidity assets) in order to pursue investment returns, when Libra faces concentration and large redemptions, fiat currency reserves The pool may not have enough high liquidity assets to cope. The Libra Alliance may have to "sell" the fiat currency reserve assets. This may put pressure on asset prices, worsen the liquidity of the Libra system and even solvency. Libra does not have the support of the lender of last resort of the central bank. If Libra is large enough, Libra runs may trigger systemic financial risks. Therefore, Libra's fiat currency reserves will be subject to prudent supervision, which is reflected in the requirements of bond types, credit ratings, maturity, liquidity and concentration.

Second, Libra's fiat currency reserves are held by investment-grade custodians distributed around the world. However, investment grade does not mean zero risk. Libra's custodian should meet certain regulatory requirements. If Libra's fiduciary reserve includes one or more central banks, then Libra is equivalent to a "synthetic CBDC".

Third, Libra naturally has a cross-border payment function, and the use of Libra will be cross-border, cross-currency and cross-financial institutions. Libra will have a complex impact on cross-border capital flows and will also be carefully regulated for risks in this area.

Fourth, if Libra-based deposit and loan activities are accompanied by currency creation, Libra should be regulated accordingly for its impact on the implementation of monetary policy. But Facebook and the Libra team made it clear during a US Congressional hearing that Libra will not have deposits and loans.

Libra involves multiple countries and currencies, and must meet the compliance requirements of relevant countries. For example, there are already regulatory frameworks for the issuance of stable cryptocurrencies in the United States and the Eurozone, and these regulations will apply to Libra. Relevant US regulations include: 1. Money service business (MSB) license of the Financial Crimes Enforcement Network (FinCEN) under the US Department of the Treasury; 2. State-operated currency transfer licenses; 3. US dollar reserves must be deposited in FDIC-protected Banks; 4. The authenticity and adequacy of the USD reserve must be regularly audited and disclosed by third parties; 5. KYC, AML, and CFT regulations.

Gao Weishen Law Firm has comprehensively combed the compliance issues facing Libra: 1. According to the Howey test, will Libra be considered as a security under US securities law? 2. If Libra is considered a virtual currency, the US Commodity Futures Trading Commission may have the power to regulate fraud and manipulative behavior. 3. Because of the existence of fiat currency reserves, Libra may be considered as a collective investment scheme in the EU and regulated accordingly. 4. Data privacy protection issues related to Libra users and transactions. 5. Tax regulatory issues.

On October 24, 2019, the government learning conference stated that "the application of blockchain technology has been extended to digital finance." The key to understanding digital finance is to understand the DC / EP (Digital Currency / Electronic Payment) of the People's Bank of China. But so far, the People's Bank of China has not publicly documented the design of DC / EP. The introduction of DC / EP was scattered in the speeches and papers of the leaders and responsible comrades of the People's Bank of China. After combing and comparing these public channel information, DC / EP should have the following core characteristics:

The first is to replace M0 and prepare 100% of the trips based on 100%. Digital currency does not count interest payments, and does not undertake other social and administrative functions in addition to the four functions of currency (value scale, means of circulation, means of payment, and value storage). In order to ensure that digital currency issuance and withdrawal do not change the total amount of central bank currency issuance, there is an equivalent exchange mechanism between the deposit reserve of commercial banks and digital currencies. At the issue stage, the central bank deducts the deposit reserve of commercial banks and issues digital currencies in equal amounts. ; In the withdrawal phase, the central bank increased the reserve reserve of commercial banks by an equal amount and cancelled the digital currency.

The second is to follow the traditional central bank-commercial bank dual model operating framework. The central bank issues digital currency to the commercial bank's business bank. The commercial bank is entrusted by the central bank to provide digital currency access and other services to the public, and works with the central bank to maintain the normal operation of the digital currency issuance and circulation system.

The third is the expression form of digital currency. Digital currency is an encrypted digital string representing a specific amount guaranteed and signed by the central bank in form, including the most basic number, amount, signature of the owner and issuer, and so on. Among them, the number is the unique identifier of the digital currency, and the number cannot be repeated, and it can be used as an index of the digital currency. Digital currency is programmable and user-defined executable scripts can be attached.

The fourth is the registration center and certification center for digital currencies. The registration center not only records digital currency and the identity of the corresponding user, and completes the ownership registration; it also records the flow, and completes the entire process of digital currency generation, circulation, inventory verification, and extinction. Based on the traditional centralized method, the registration center is a digital coinage center with a new concept. The authentication center is an important part of the controllable anonymous design of digital currency. The authentication of financial institutions or high-end users can use the Public Key Infrastructure (PKI, Public Key Infrastructure). IBC, Identity Based Cryptography).

Fifth, the account is loosely coupled and put into a centralized management model. Digital currency is less dependent on accounts in the transaction link. It can be as easy to circulate as cash and can achieve controlled anonymity. The meaning of controllable anonymity is that digital currencies only disclose transaction data to a third party, such as a central bank. However, if the holders do not wish, even commercial banks and merchants cannot cooperate to track the history and use of digital currencies. Digital currency holders can directly apply it to various scenarios, which is conducive to the circulation and internationalization of the RMB. In contrast, bank cards and Internet payments are based on a tightly coupled account model.

Six is the application of distributed ledgers. Digital currency registration centers do not use distributed ledgers. In DC / EP, the distributed ledger is used for digital currency right confirmation registration, providing a website for external digital currency right confirmation inquiries through the Internet, and realizing the function of digital currency online banknote detectors. This has two advantages. On the one hand, the core issuance registration system is isolated and protected from the outside world, and the advantages of distributed ledger are used to improve the data and system security of rights inquiry. On the other hand, because the distributed ledger is only used to provide query access to the outside, the transaction processing is still completed by the issuance registration system, so it effectively avoids the bottleneck of the existing distributed ledger in transaction processing.

Seven is system independence. Digital currency is universal and ubiquitous. It can complete transactions on a variety of transaction media and payment channels, and can take advantage of existing financial infrastructure. In theory, digital currency can also be reached by the payment network boundary that bank deposit currencies and electronic money can reach.

I am mainly based on the central bank digital currency prototype system introduced by Yao Qian in 2018, and the speculation on the DC / EP design is as follows:

The first is account loose coupling = Token paradigm. From the public disclosure of the People's Bank, DC / EP does not use a real blockchain like Libra. Although DC / EP is not a token in the blockchain, it has the same key features as non-double spending, anonymity, non-forgeability, security, transferability, separability, and programmability. Token is similar. Therefore, DC / EP still belongs to the token paradigm, not the account paradigm.

The second is that DC / EP uses a centralized ledger based on the UTXO model. This centralized ledger is embodied as a digital currency issuance registration system, maintained by the central bank, is centralized, and does not need to run consensus algorithms, so it will not be subject to the performance bottleneck of the blockchain. . Centralized ledgers can be organized by hash functions and Merck trees, but because they are maintained by the central bank, it makes little difference whether or not to do so. More importantly, the credit of the central bank is significantly higher than that of commercial banks and other private institutions. It is not necessary to introduce a distributed trust mechanism represented by the blockchain in DC / EP, so it makes sense for DC / EP to use a centralized ledger. Of course, the centralized ledger based on the UTXO model can also be regarded as a "degraded" blockchain (or a blockchain with only one node). In addition, the blockchain may be used for the right registration of digital currencies and is in a subsidiary position.

The third is DC / EP wallet. Users need to use a DC / EP wallet. The core of the wallet is a pair of public and private keys. The public key is also the address, and the digital certificate in RMB is stored in the address. This digital voucher is based on a 100% RMB preparation bank. Users can see the addresses of other users, but they do not necessarily know the identity of the address owner. The central bank knows the correspondence between addresses and user identities through the digital currency registration center it manages, but it is not necessarily a strong real name system.

The fourth is DC / EP transactions. Users can initiate transfer transactions between addresses using the wallet's private key. DC / EP transfer transactions are not broadcasted to a peer-to-peer network like token transactions in the public chain, and then miners are packaged into blocks and run consensus algorithms.

Fifth, the DC / EP implementation strategy : wholesale (to B), and then retail (to C or for general purposes); first use in China, then use for cross-border payment.

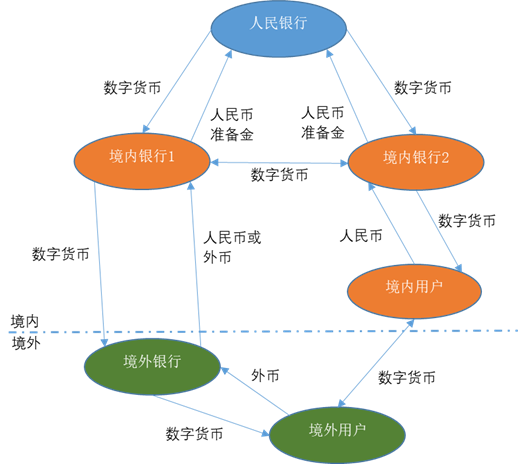

Figure 8 shows the flow of funds in DC / EP:

Figure 8: Flow of funds in DC / EP

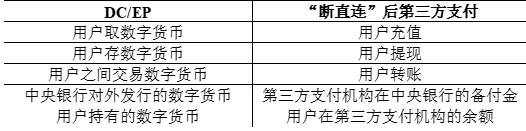

In a certain sense, DC / EP has an isomorphic relationship with third-party payments after “disconnecting directly” (Table 5). If DC / EP is good enough in terms of technical efficiency and business development, from the perspective of users, theoretically, the third-party payment after DC / EP and "disconnected direct connection" should bring the same experience. Therefore, for users, there is a mutual substitution relationship between DC / EP and third-party payment in the application.

Table 5: Comparison of DC / EP and third party payment

In addition, there are the following similarities between DC / EP and third-party payments after “disconnecting directly”: 1. They are aimed at general users, especially retail users, so they are all called “General Purpose”. 2. They are all centralized and based on the central bank-commercial bank dual model. 3. Both have complex effects on money supply and money multipliers (for a detailed analysis, see Section 4). 4. Digital currencies do not pay interest, and users' balances at third-party payment institutions do not pay interest (Yuebao products are not applicable in this case, see Part II).

The difference between DC / EP and third-party payment after “disconnecting directly” is also very obvious. First, after "disconnecting directly", the third-party payment is based on the account of the third-party payment institution and the reserve account of the third-party payment institution in the central bank, which is a tightly coupled account model. Digital currency is based on the digital currency issuance and registration system managed by the central bank and is a loosely coupled account model.

Second, third-party payments are based on accounts, and there is a link between accounts and identification, so they are not anonymous. Digital currencies are controlled and anonymous. This will cause a difference in privacy protection between the two.

Third, users' balances at third-party payment institutions are a payment tool. Third-party payment transfers are limited to users who use the same third-party payment agency. For example, WeChat payment users and Alipay users cannot transfer transactions directly. Digital currency belongs to M0 and is legally compensable in any scenario.

Fourth, the substitution effect of DC / EP on cash is very obvious, and it has a strong policy meaning for the central bank to monitor the flow of funds and the supervision of anti-money laundering, anti-terrorist financing and anti-tax evasion. DC / EP programmability has brought space for intelligent macro-control, such as "forward-looking guidelines" for monetary policy. Yao Qian has a special analysis on this. It should be said that the application of digital currency programmability is an important content of digital finance. Third-party payment mainly replaces payment tools such as bank cards and checks, and has no strong policy tool significance.

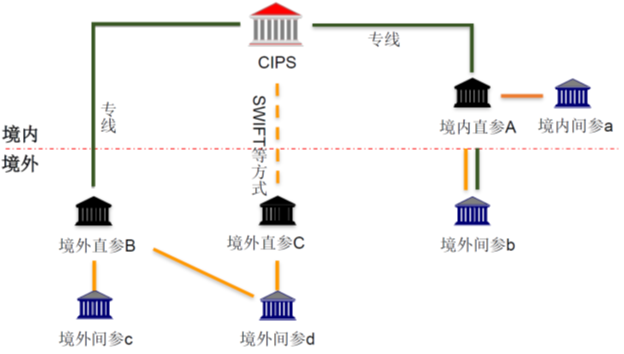

The impact of DC / EP on RMB internationalization is mainly reflected in cross-border payments based on digital currencies. Before 2015, RMB cross-border settlement mainly had two models: correspondent bank and clearing bank. In 2015, the RMB Cross-border Interbank Payment System (CIPS) was launched as a “highway” for RMB internationalization, providing cross-time zone clearing and settlement of funds for RMB cross-border and offshore businesses (Figure 9, (Cited from the July 2018 "Main Functions and Business Management of RMB Cross-border Payment System (CIPS)" in the Research and Planning Division of the Payment Settlement Department of the People's Bank of China).

Figure 9: RMB cross-border payment system (CIPS) architecture

The above cross-border payments are based on bank accounts. To this end, offshore banks need to have RMB business, and overseas enterprises and individuals need to open RMB deposit accounts. DC / EP only requires users to have a DC / EP wallet, which is much lower than opening a RMB deposit account. Digital RMB transactions are naturally transnational, and DC / EP can effectively expand the use of RMB abroad. At this point, DC / EP has similar logic to Libra.

Overseas banks, enterprises and individuals can obtain digital RMB in two ways. First, exchange it with domestic banks, enterprises or individuals through your own RMB. This is essentially that the digital currency issuance and circulation system extends overseas through cross-border payment networks. Second, exchange digital RMB with foreign currencies. This implies the requirement for RMB convertibility. Digital RMB obtained by overseas banks, enterprises and individuals will flow back to China through cross-border trade, investment and financing, and financial market operations (Figure 10).

Figure 10: DC / EP and cross-border payments

Although cross-border payments, including DC / EP, can promote RMB internationalization, cross-border payments are only a necessary condition for RMB internationalization, not a sufficient condition. The internationalization of the RMB is inseparable from a series of institutional arrangements. Currency internationalization has three dimensions: trade settlement currency, investment currency and reserve currency. International currencies should meet: 1. Freely convertible; 2. Stable currency value, low internal inflation rate and external exchange rate stability; 3. Reliance on deep and wide cross-border trade scenarios; 4. High acceptance abroad The domestic financial market is mature and highly open; 6. The domestic legal environment is perfect, especially in terms of property rights protection. These requirements go beyond cross-border payments.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Opinion: Blockchain games are still an experiment until commercial success

- Vitalik 4D Long Text: What will happen to the hard core puzzles that plague cryptocurrencies in five years?

- Opinion | Why it is inevitable that the stablecoin introduces the KYC program

- Babbitt Original 丨 Two blockchain listed companies were born this week. Why did Hangzhou grab the nation?

- USDT Alchemy: Concealment, Additional Issues, and Manipulation

- One article to read Singapore's central bank digital currency plan, Ubin

- Overview: What are the DAOs on Ethereum?