How to value DCG with three core businesses: Grayscale, Genesis and CoinDesk?

Author: Jack Purdy

Translation: Zoe Zhou

Source: Crypto Valley

- Legal analysis of smart contracts: What is the difference between smart contracts and traditional contracts?

- US SEC proposal proposes to expand the scope of "qualified investors"

- Inventory: Who will predict the price of Bitcoin in 2019?

Introduction

Compared with traditional start-ups, digital asset companies and projects have easier access to cash, whether through the release of $ 4 billion in pre-issued tokens or the first bucket of gold mined by early-stage entrepreneurs.

In the past few years, we have seen more and more traditional venture capital participation, but eventually these companies will need to enter a larger capital market. Mining giants Bitmain and Canaan Technology have applied for listing in Hong Kong, but have failed in the end (recently, Canaan Technology was successfully listed on the NASDAQ, stock code "CAN"). If you asked a year ago who would be the first major crypto company to go public in the United States, I would unambiguously say Coinbase. However, since then, we have seen a huge staff turnover in their management team, with President and Chief Operating Officer Asiff Hirji, Chief Technology Officer Balaji Srinivasan, and most recently Engineering Vice President Tim Wagner leaving the company. You wouldn't expect a company with such a high turnover rate to go public. Now, I think the most likely candidate is the Digital Currency Group (DCG, Digital Currency Group), which plows the industry track. They have been around for a while and have formed corporate networks represented by Grayscale, Genesis and CoinDesk.

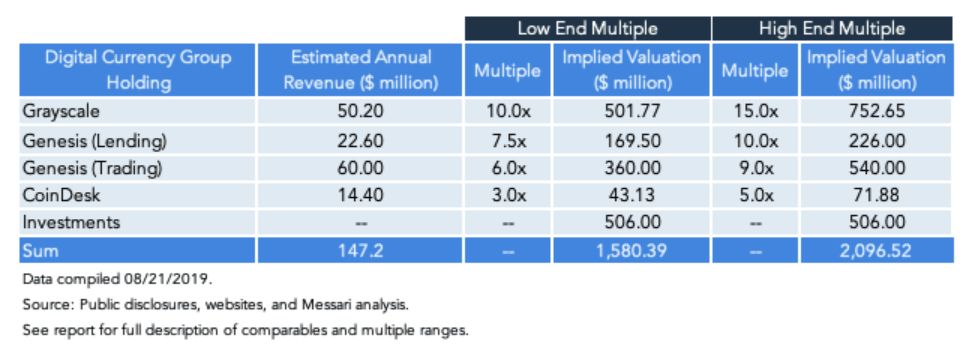

But before other peers came out, the question became the value of a crypto company in the open market. To answer this question, we used a sum-of-the-parts (SOTP) analysis method to get a rough estimate. Simply put, the SOTP valuation method is to divide an enterprise into different parts, get a value, and then add them up. However, assessing the value of each sector is difficult and largely depends on the amount of information available. In this case, we decided to estimate the annual revenue and then derive a value range by looking at the market value / income ratio of listed comparable companies. Because companies engaged in digital asset business are inherently risky but also have high returns, we have selected this range and marked it as multiples to illustrate this point.

Grayscale Investment

The first is Grayscale Investment. Grayscale is an asset management company that manages $ 2.5 billion in assets (AUM). They are well-known suppliers of GBTC products, which mimic exchange-traded funds (ETFs) and have a wealth of products, such as Ethereum, Litecoin, XRP, and so on.

Since we manage the assets and annual fees of each fund, we can roughly estimate the total income. As of the latest data as of July 26, 2019, we extrapolated revenue of $ 50.2 million.

Initially, we focused on ETF providers such as Wisdom Tree, but most of them invested in stocks on the open market with a commission fee of less than 0.50%. The commission charged by Grayscale is slightly higher, ranging from 2.0% to 3.0%. To better estimate GBTC, we looked at asset management companies that offer private or alternative investments in less liquid markets. Companies like Hamilton Lane, Cohen & Steers and Victory Capital will provide more non-traditional investments and adopt a similar business model to link revenue to the fees charged in asset management. The revenue multiples of these companies are between 7 and 12 times, so we can believe that Grayscale's revenue multiples are between 10 and 15 times, that is, between 501.8 and 762.6 million US dollars.

Genesis Capital

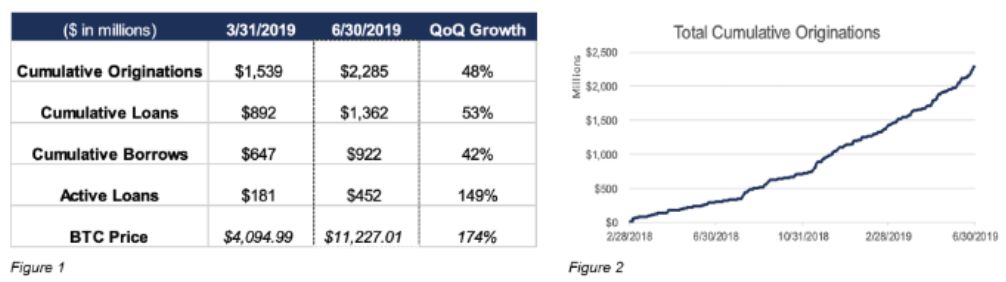

Genesis Capital is the largest over-the-counter lending company in this space, providing mortgages to institutions seeking to short assets, gain exposure or manage working capital.

They provided a quarterly loan report that stated that there were $ 452 million in outstanding loans in the second quarter of 2019. Like most lending businesses, their income model is based on interest received minus interest paid to depositors. We believe that deposits account for only a small part of the balance sheet, so income is mainly derived from interest income. From conversations with similar lenders, we estimate that the return on outstanding loans is about 5.0%, which translates into annual income of $ 22.6 million.

There are hundreds of listed companies in the market that provide loan services, so we need to narrow down to find companies similar to the Genesis business model, that is, to provide high-risk digital currency loan services that require mortgages. As a result, we found that some companies hold secondary mortgages or subordinated debt in mid-markets (companies with lower credit ratings and less debt cannot get debt repayment as soon as the borrowing company goes bankrupt).

Companies such as Ares Capital, Capital Southwest, Golub Capital, and Bain Capital SF have revenue multiples between 5.9 and 9.3. After readjustment, the income multiple increased to 7.5 times to 10 times, that is, the valuation was 169.6-2226 million US dollars.

Genesis Global Trading

Genesis trading is DCG's OTC trading division. This department enables investment institutions and high net worth individuals to trade large amounts of digital assets. Although they are trading companies, because they are not investors and are generally neutral, they do not benefit from capital appreciation. Instead, profits are made by investors buying and selling assets with small spreads over a specific period of time. Although this spread is small, it can make money by facilitating a large number of transactions. Currently, there is very limited information on Genesis's trading volume, but its main competitor, Circle, revealed that it had traded $ 24 billion last year. Although this is far from perfect, it provides an estimate. Assuming a spread of 0.25%, we estimate that Genesis Trading's revenue can reach $ 60 million. The only one that performed relatively well was the OTC group. Its trading multiplier is 6.8 times, which is between our estimated 6.0 times and 9.0 times, that is, the valuation is between 360 and 540 million US dollars.

Coindesk

DCG also has a media platform, Coindesk. For the past few years, the site has been known as the main source of digital asset news. Most of its revenue comes mainly from the annual consensus conference hosted. According to reports, CoinDesk's revenue last year was 25 million US dollars, 85% of which came from the consensus conference. About half of the time last year went to the consensus meeting, so this 50% part brought about $ 14.3 million in revenue. We did not find a public company with a similar business model. Fortunately, a leading fintech media company called Money 2020 reportedly sold for $ 120 million a few years ago. We looked at attendance and the classification of different pricing, and inferred that the expected revenue was $ 34.2 million, which is 3.7 times the event revenue. Calculated at a revenue multiple of 3-5 times, the valuation of CoinDesk is between US $ 43.1-71.9 million. This result is in line with rumors that CoinDesk was rumored to be sold for $ 70 million in May 2019.

Investment Business

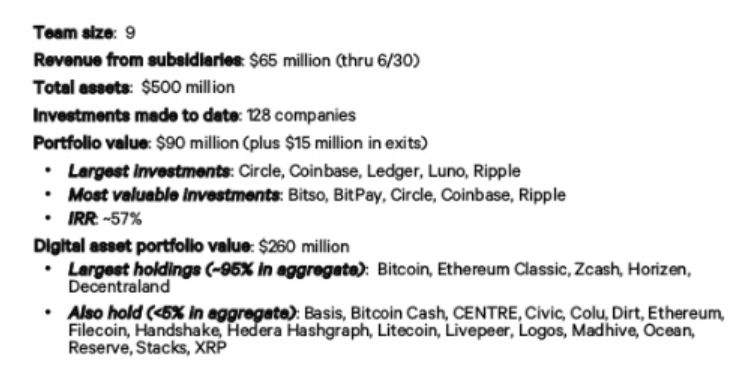

The last part of DCG's business is investment in digital assets and venture capital companies. As of June 30, 2018, the value of its two business assets was US $ 260 million and US $ 90 million, respectively. The price of BTC at that time was $ 6,178. Since then, the price of BTC has increased by 60%. Therefore, we use this number to calculate their digital asset holdings. It is estimated that their total investment amount has reached 506 million US dollars.

Now, as part of the SOTP valuation, adding it to the SOTP valuation results in a SOTP valuation of $ 158-21 billion. It was included in TBI's list of digital asset unicorns.

Like everything in this field, DCG's valuation is highly dependent on the price movements of BTC and the ups and downs of the entire crypto asset industry. If we see price levels approaching previous historical highs, this will change revenue estimates. As asset prices rise, revenue drivers such as asset management scale, outstanding loans, and transaction volume will all increase directly, which means that a USD 20,000 BTC is likely to bring DCG's market value closer to USD 3 to USD 4 billion.

Valuation is usually an art, not a science, and comes with many subjective assumptions. But we think this is a good starting point for assessing the value of a company like DCG. If DCG does go public, it will provide investors with a way to directly access the field without holding digital assets and potentially fill the long-awaited BTC ETF gap.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Global Blockchain Financing Track Top 20: 1,543 venture capital investments with a total funding of more than 79.2 billion yuan

- Satoshi Nakamoto's theory of the crypto market after the bulls' collapse?

- Perspectives | Five conjectures for the blockchain industry in 2020

- Blockchain can't save traffic NetEase circle and other products failure revelation

- Comment: Why did Satoshi Nakamoto give up being the richest man in the world?

- Looking for "new rich mines" in the automotive industry: blockchain may become a breakthrough

- Opinion: 5 predictions for DeFi in 2020