Interpreting the RWA track of on-chain real estate Can it revolutionize the traditional trading and leasing market?

Can on-chain real estate revolutionize traditional trading and leasing with RWA tracking?Author: Jeff@Foresight Ventures

Summary:

- On-chain real estate can split the asset structure and rights of real estate into secondary parts, allowing for separate transactions of ownership, income rights, and usage rights. Especially, on-chain real estate can be further split into multiple layers in terms of time.

- The key to the current development of on-chain real estate projects is how to solve the problem of fragmented scenarios during the on-chain process. Platform tokens, DIDs, and on-chain payment platforms have the potential to become tools to solve the black box problem.

- The current compliance architecture has potential risks, as there is a lack of solid rights relationship between the NFT held by the buyer and the SPV company.

- It is suggested to explore bridging uncommon asset categories, such as extremely cheap distressed assets and extremely expensive scarce assets, and binding fractional ownership with NFT to meet the real trading needs of buyers and sellers.

- It is suggested to segment user groups and refine usage scenarios, for example, serving the rental needs of digital nomads and leveraging the web3 native genes of this group to create small and beautiful business models.

In the RWA track, the core of innovation lies in the split and recombination of asset structures. The total market size of the real estate industry reached 11 trillion US dollars in 2022. It is worth paying attention to how to bridge such a huge market onto the chain and form a new market ecosystem. This article reviews the on-chain real estate projects in the market, points out the common problems of on-chain real estate projects, and proposes corresponding assumptions.

1. On-chain Solution for the Full Lease Housing Problem in South Korea

The real estate crisis caused by the full lease housing system in South Korea has fully displayed many problems in the traditional real estate transaction chain. The full lease housing system refers to the system where tenants pay a deposit of 60-70% of the total value of the house to the landlord at one time and can use the house without paying rent for a fixed period of time (usually 2 years). Due to the lack of transparent regulatory mechanisms, the deposit used by tenants to offset rent is fully invested by landlords into new properties, and then the cycle of cashing out continues through the full lease housing system. The real estate market is extremely vulnerable under high leverage ratios. Once problems such as a significant decline in housing prices, loan defaults, and disruptions in the funding chain occur, it becomes extremely precarious. As a result, many landlords choose to quietly flee without being able to return the deposit. Since the deposit paid by tenants can only represent the personal debt of the landlord, they can only receive minimal compensation from the debt settlement with low priority after the auction of the property.

- Interview with Uniswap Founder Handing Over Routing Issues to the Market through UniswapX

- Can blockchain revolutionize the traditional real estate transaction and leasing market?

- Tokyo vs Kyoto Japan’s Cryptocurrency Twin Cities

Can the real estate crisis caused by full lease housing be avoided through on-chain real estate projects? Here are the main market problems and corresponding on-chain solutions:

- Issues with defaulting on deposits and other funds.

Tenants can track the flow of funds and debt situation of landlords by paying deposits through on-chain payments, and be alerted in a timely manner to situations where the assets do not cover the liabilities. Smart contracts can also be used to specify the unlocking date for funds and automatically return the deposit or guarantee to the payer.

- Landlords and tenants lack a background check platform, especially for tenants who cannot assess the risk of property mortgages.

If the property rights are put on the chain and NFTs are generated, tenants can clearly trace the mortgage status of the property rights NFT and effectively avoid “high debt” landlords, reducing unnecessary troubles.

- Once the landlord defaults on their debt, the tenant, who does not hold the property rights, can only wait for compensation with lower priority for debt repayment.

If the property rights NFT is further divided into fragmented NFTs on the chain, tenants can receive a corresponding proportion of the property rights NFT when paying the deposit, and return the corresponding NFT upon receiving the deposit. In the event of a landlord’s default and liquidation, they can also obtain corresponding compensation based on the corresponding property rights NFT.

- The real estate transaction market has local limitations.

During the process of liquidating defaulted properties through auctions, by putting the property rights on the chain and minting NFTs, the geographical restrictions of real estate transactions can be effectively reduced, expanding the range of users participating in transactions from local to all users on the chain.

- Restrictions on bulk transactions in real estate.

The majority of rental properties are concentrated in prime locations in Seoul, and the high price of individual properties discourages ordinary investors. By fragmenting the property rights NFT, buyers can purchase only a portion of the fragmented property rights NFT, greatly reducing the investment amount restriction.

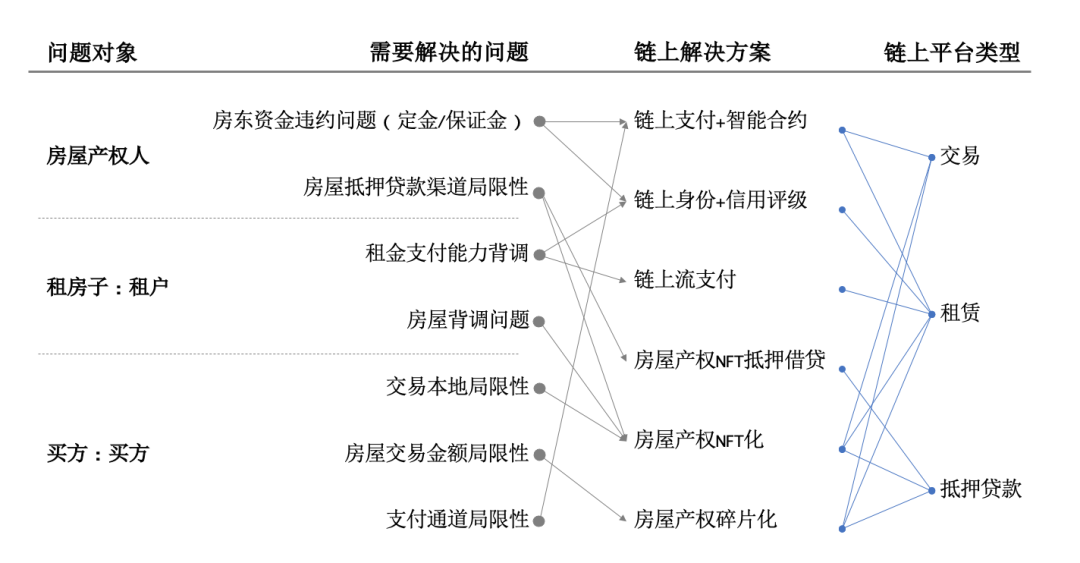

II. Target pain points and core links of on-chain real estate projects

Referring to the above examples, we have supplemented potential market pain points and issues in the real estate chain, and classified their on-chain solutions and existing on-chain real estate projects into the following three core links for discussion: transaction link, leasing link, and mortgage loan link.

> Figure: Summary of market pain points and on-chain solutions

In the real estate transaction link, the buyer’s needs are often prioritized. Existing on-chain real estate projects mainly split property rights and usage rights, recombine transaction content with the dimension of time, and attempt to solve potential market problems through on-chain payments, on-chain identities, property rights NFTs, and their fragmentation.

- Eliminate the limitations of local transactions, and on-chain property background checks make property information more reliable.

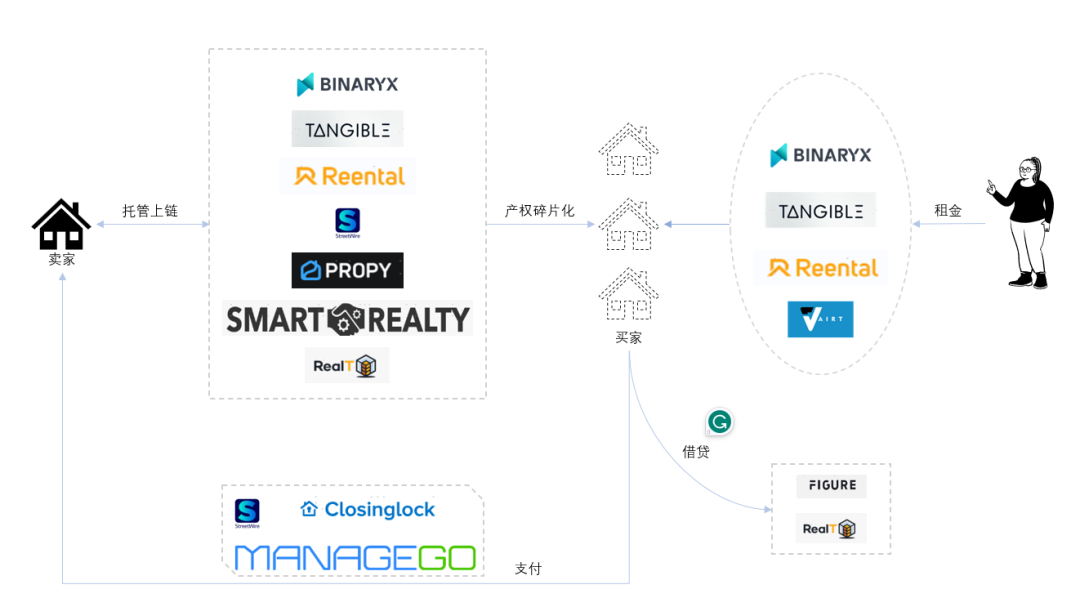

It is not difficult to understand that on-chain platforms provide global investors with a window of investment freedom. Platforms like Tangible package the property rights into SPVs (Special Purpose Vehicles) in the location of the property and mint all the property rights proofs, property information, etc., into property rights NFTs. Global traders can directly purchase the NFTs of the property through their portal website, representing ownership of the corresponding property. In this process, the Tangible platform first advances 10% as a deposit to the seller, and then opens subscription to the buyer. The buyer decides whether to purchase after reading the property rights and information of the property.

- Prevent assets such as down payments and deposits from being forfeited in breach of contract, and ensure the security of funds through on-chain payments.

By using on-chain payments for house down payments, smart contracts can be set up with time limits to automatically impose losses on the defaulting party. On-chain payments can also improve fund transparency and provide early warning for risks. As described earlier, after Tangible advances the down payment for selling a house, if the subscription is not completed within the agreed period, the down payment will be automatically refunded to the Tangible platform.

- Eliminate limitations on transaction amounts in housing transactions and lower the threshold for purchases.

Users can customize their investment amounts. In order to lower the entry barriers for cross-border house purchases, platforms like RealT split the property rights of houses into fragments, allowing small-scale investors to voluntarily subscribe to quotas. Some platforms also split the property rights and rental income of houses, allowing users to only purchase future rental income for N years. In addition, CityDAO fragments land property rights and governance rights by registering DAO companies, so that buyers not only have property rights but also governance rights.

- Eliminate limitations on payment channels.

The regulatory issues faced by fiat currency transactions also trouble global traders. Therefore, platforms like Smart Reality and ManageGo have specifically established virtual currency payment channels, which can host down payment funds. On the basis of mutual agreement between buyers and sellers, settlements can even be made directly in virtual currencies. Closing lock and other trading platforms act as intermediaries to monitor the security of funds and charge corresponding commissions.

The issues in the leasing process mainly revolve around rent collection and housing safety. Currently, leasing platforms in the market have not fully migrated leasing activities onto the blockchain. Without exception, platforms like Tangible, BinaryX, and Reental have adopted a form of collaboration with web2 outsourcing companies to ensure that tenants pay rent on time. However, there is more room for exploration in managing house rentals on the blockchain.

- On-chain leasing allows for two-way background checks on tenants’ rent payment capabilities and landlords’ housing backgrounds.

Through on-chain leasing, landlords can observe the on-chain activities of tenants to assess their asset levels and ability to pay, thereby proposing corresponding deposit payment plans. Tenants can also judge the reliability of a property by referring to its on-chain property rights information. Currently, StreetWire is developing a series of functionalities in this direction.

- On-chain payment of deposits ensures the security of assets, and flow payment platforms make rent payment mandatory.

As mentioned in the case of full-rent housing in South Korea earlier, on-chain payment of deposits can protect the interests of tenants through fragmented property rights. For traditional monthly rental models, on-chain flow payment platforms can be used to enforce timely rent payment by tenants through smart contracts, and ensure that deposits are promptly refunded after the rent expires. We have already seen successful cases of on-chain scheduled rent payment on the Sablier platform.

- Fragmented property rights NFTs allow for the splitting and combination of rental income from houses.

The fragmented property rights NFT can distribute the collected rent to each landlord according to the proportion of property rights through smart contracts. At the same time, external adjustment factors can be introduced to dynamically adjust the leasing conditions according to market demand. In this way, property rights NFT becomes composable, and users can freely sell “lease contracts” and impose time restrictions. The three leasing platforms mentioned above, such as Tangible, have already developed the function of splitting rental income. In addition to this model, platforms like Vairt are also trying to move short-term rentals to the blockchain to cope with housing vacancies.

The mortgage loan process for real estate is currently in a blank stage in the market, with only RealT and FIGURE attempting to provide mortgage lending functions to fragmented property rights NFTs. However, due to objective factors such as the immaturity of market pricing and imbalanced supply relationships, they have not yet been widely recognized by the market. In addition, lending platforms that reduce the cost of buying a house are also in a blank stage in the market, and the market is currently lacking the functionality of BNPL (Buy Now Pay Later).

> Figure: Core breakdown of on-chain real estate projects

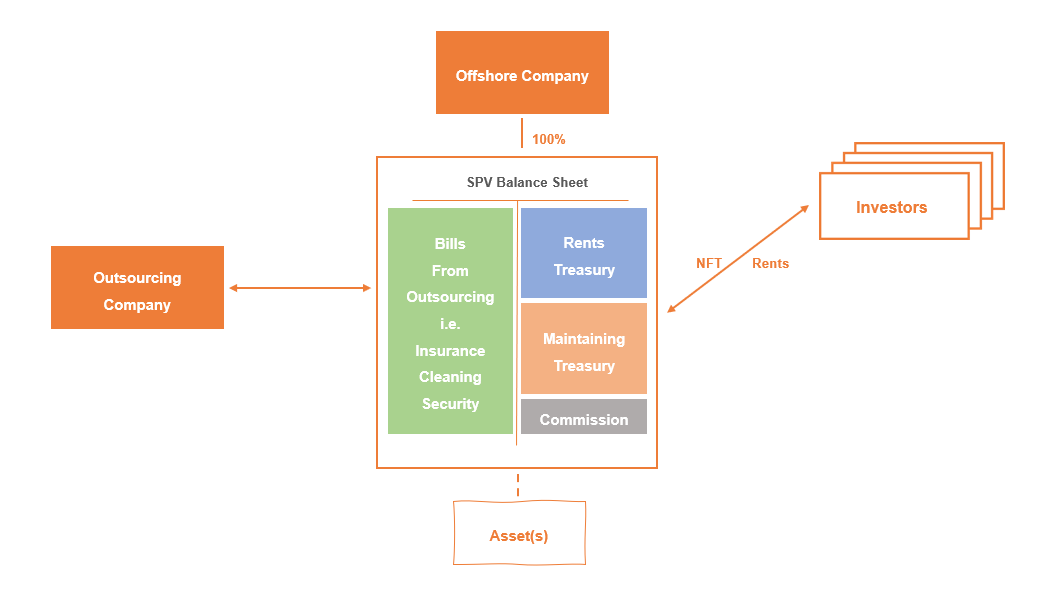

III. Compliance Architecture and Asset Security

The issue of ensuring the compliance of on-chain property rights is the most concerned issue in the author’s research. Currently, almost all on-chain real estate projects bypass market regulation by using offshore entities as holding SPVs. The author believes that this method is not completely secure and effective.

> Figure: SPV architecture diagram of on-chain real estate projects

Take Tangible’s compliance solution as an example. The UK properties sold on the Tangible platform are held by independent UK SPVs. The offshore entity of the Tangible platform directly controls each SPV company. The fragmented property rights NFT of the house is issued by the SPV entity and sold to buyers. To some extent, the transaction security and legality of the house are protected. However, strictly speaking, the fragmented property rights NFT of the house does not directly represent the equity of the corresponding SPV. Once the parent company or SPV encounters debt disputes, because the fragmented property rights NFT cannot directly confirm the property rights of the house or even directly correspond to any shares of the offshore company, buyers are likely to end up with nothing. The asset security issue that was originally hoped to be solved by the blockchain has been completely relied on the trading platform itself, which indirectly increases additional risks. In addition, if the fragmented property rights NFT of the house is issued by the SPV company, everything will return to the regulatory dispute of whether the token should be defined as a security.

From this, it can be seen that the only solution to bypass regulation while ensuring asset security is to strengthen the regulation of SPV companies. CityDAO provides us with a good example in this direction. It guarantees the interests of every NFT holder through a registered DAO-form company. We look forward to seeing CityDAO perform after breaking through geographical limitations in the future.

So, does the SPV company have the risk of debt disputes? Yes, especially the default risk in the process of house rental.

- Reserve fund risk: Taking Tangible as an example, the platform deducts a total of 7% of the total value of the property as idle reserve fund and maintenance reserve fund. If the reserve fund is lower than the above ratio, 20% of the rental income will be withheld or the rental payment will be suspended for replenishment. The reserve fund, as a non-chain asset, is not transparent in real operation. Since the SPV company has the right to dispose of the reserve fund, it is highly likely to use the reserve fund to pay the deposit for subsequent auctioned houses or even for other purposes. Once the property cannot be rented out for a long time and the funds from the sale of other properties do not return in a timely manner, the SPV will face the risk of debt default.

- Mortgage risk: Since the property rights of the houses are all owned by the SPV company and users cannot monitor in real time during actual operations, the SPV company may mortgage the houses and use the loan funds for other investments, which also increases the risk of debt default.

What other problems have not been solved? What could be the solutions?

In my opinion, the black box problem in the process of being on the chain is the most core issue that needs to be solved. The fragmentation of on-chain and off-chain scenarios leads to the uncertainty of on-chain transactions and rentals. This uncertainty directly leads to the following problems:

- Scarcity of high-quality assets: Good houses are not difficult to sell offline, but on-chain properties need to be investigated before being put on the chain. This additional step may result in lower transaction efficiency compared to offline real estate agents. The properties that users can see on the chain are often properties that are difficult to sell offline, or they need to bear costs higher than the market level as a whole. How to improve the efficiency of being on the chain and continuously supplement the housing resources according to customer needs is also a problem that needs to be solved.

- Actual investment returns are far lower than expected returns: When calculating expected investment returns, the platform considers both the potential increase in property value and rental income as expected returns. However, in the actual operation process, the rental and management of the houses are outsourced, and factors such as the duration of the lease and tenant defaults cannot be controlled. In particular, tenant defaults in Europe are a very difficult problem to deal with. If tenants refuse to pay rent, landlords can only enforce payment through legal actions, which can take up to six months. This also means that there will be zero rental income for six months.

- Imprisonment of property liquidity on the chain: On-chain purchased properties are fragmented due to ownership fragmentation. When holders want to resell, they can only wait for buyers who are willing to purchase equivalent fragmented ownership. Liquidity is relatively restricted, and it may even be confined to the chain. On-chain real estate mortgage loans are in a vacuum stage in the market and need to be filled urgently.

In addition to the black box problem, the commercial form of on-chain real estate platforms is not native to web3, and platform tokens are basically not empowered. The entire industry can only awkwardly be considered as on-chain web2 platforms.

- Most of the tokens of on-chain real estate platforms do not have any use cases. We hope to increase the use cases of tokens to improve platform user stickiness and stimulate the participation of non-investment users. For example, in addition to real estate transaction users, users who browse the web pages can also be participants and content contributors of the platform.

- The leasing process relies too much on outsourcing companies, which makes it impossible for users to form stickiness to the platform. By adding pure on-chain transaction links to the leasing process and combining user DID and credit accounts, the amount of collateral that users need to pledge can be determined. At the same time, by combining smart contract-controlled door locks or power switches, etc., users can be prevented from not moving out when the lease expires. In addition, maintenance processes can also be improved by using crowdsourcing token incentives to increase user stickiness.

- The platform overly relies on regional resources. Currently, 90% of on-chain real estate platforms are concentrated in the United States, while the global ranking of real estate transactions in 2022 is the United States, Japan, the United Kingdom, and Germany. However, there is little interest in the latter countries and regions, and few platforms can connect the global transaction market or leasing market. The author believes that the leasing market is a native scenario for web3 users and deserves attention. The following will be discussed in detail.

Four, Open Ideas for On-chain Real Estate Projects

Although there are many problems with on-chain real estate projects, and the biggest problem is that they do not address users’ real needs on the ground. However, we still maintain a positive and optimistic imagination for this track because there are still many niche scenarios and potential user needs that have not been specifically met.

In the real estate market, high-quality assets often lack liquidity. If we can broaden the categories of real estate and then reclassify them, we can obtain more focused categories. We have listed two categories.

- High-priced scarce immovable properties.

These high-priced rare immovable properties often discourage ordinary people. For example, castles, old houses, wineries, farms, etc. These assets generally have extremely high individual prices and are not used to meet daily residential needs. Middle-class investors can only stop at admiring them and do not have a good investment window. These assets also face long transaction cycles during the trading process, resulting in unsatisfactory liquidity. On-chain platforms provide a good solution by separating the property rights and usage rights of these assets. Let’s take wineries as an example. If the production of wine can be included in the winery transaction process, the ownership of the winery represents the fixed amount of wine produced each year. After purchasing the ownership NFT, buyers can sell the wine produced each year. This creates an innovative trading market. Through on-chain contracts, property rights and usage rights are dispersed over the timeline, and users can freely combine and trade, forming a non-standardized innovative market. This not only reduces the threshold for investors but also quickly improves the liquidity of these assets.

> Figure: Concept of winery property rights and equity NFT

- Extremely cheap distressed assets.

These types of assets are often acquired and restructured by specialized acquisition companies. For example, abandoned buildings, dilapidated old houses in need of repair, etc. Such assets often have an expected commercial use after renovation, but at the same time, there is no way to open a secure window to ordinary investors. On-chain platforms can solve this problem by splitting property rights NFT and equity NFT, which can reduce the investment threshold and provide a reasonable exit path. For example, for a house in need of repair, if it can be planned as a guesthouse hotel, investors can enjoy the equity NFT for accommodation, which can then be sold on the market or used for personal use. At the same time, the entire fundraising process is centralized on the chain, and all investors can easily monitor the flow of funds, reducing improper expenses of the project.

Currently, most on-chain real estate platforms do not segment users, and the scenarios are relatively rough. Segmenting target users can make the leasing track more accurate, align the platform’s tone with user needs, and increase usage frequency. We have cited two possible scenarios:

- Digital nomads are a large group in the web3 community, with over 35 million worldwide and growing. Digital nomads often travel globally and often have a strong demand for renting, but due to objective factors, they cannot sign long-term lease contracts. Short-term rentals also come with high market premiums. I believe that launching an on-chain leasing platform for digital nomads is very effective. They are very familiar with the on-chain ecosystem, and most people can track the source of their assets through on-chain behavior, making it easier to trace the landlord. On-chain leasing platforms can also lock deposits through on-chain smart contracts. Users can evaluate landlords’ properties and use on-chain reputation to effectively constrain both parties by tagging tenants and landlords with DID.

> Figure: Global distribution of digital nomads

- Launch community-based real estate projects, create autonomous communities similar to Anaya and CityDAO through the “people mine” and utilize the 2Earn mechanism of the WEB3 platform. Community members control legal entities through property rights NFT, release rights and profits through platform tokens, and have reasonable autonomy rights. All property rights and equity can also be resold or even mortgaged through on-chain platforms, forming a new community-based real estate format.

Stay optimistic

Although it may seem too early to discuss on-chain real estate projects at this moment, many problems are difficult to solve in a short period of time. However, in the face of such a huge market capacity and real market demand, I still choose to remain optimistic. I believe that on-chain real estate projects can create a revolutionary market ecosystem.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Reading the Bitcoin ETF 5 futures ETFs with total assets of nearly $1.3 billion. How much does the news of the Bitcoin application affect?

- Analysis of Bitcoin ETFs The total assets of 5 futures ETFs are nearly 1.3 billion US dollars, how much impact does the application news have on Bitcoin?

- Some ‘dirt’ on the SEC Chair

- Bitcoin Lightning Network + Nostr Decentralized Social Payment New Paradigm

- Is CoinDesk selling at a loss with a valuation of $125 million after being in business for ten years?

- The fourth halving of Bitcoin is imminent, will the cryptocurrency market repeat yesterday’s story?

- Why has the significant discount on GBTC gradually narrowed recently?