Depth Latest analysis of asset risk assessment for stablecoin TrueUSD (TUSD)

Latest analysis of TrueUSD (TUSD) stablecoin asset risk assessmentAuthor: LLAMARISK

Translation: Block unicorn

- Analyzing the Unique Aspects of Puffer Finance’s Design from the Perspective of Node Validation Rights

- In-depth Analysis of Base Standing on the shoulders of giants, emerging in the fiercely competitive Layer2 race.

- How can Base chain without tokens start Onchain Summer?

Relationship with Curve

TrueUSD (TUSD) plays an important role in crvUSD, as one of the Pegkeeper pools (crvUSD/TUSD), along with USDC, USDT, and USDP. Pegkeepers mint or burn crvUSD tokens based on market conditions to algorithmically control the peg of crvUSD to 1 USD, essentially supporting the outstanding crvUSD supply with a portion of its Pegkeeper pair.

Pegkeepers enforce balance in each Pegkeeper pool, so if the pegged value of Pegkeeper assets falls below 1 USD, it leads to an excess circulation of crvUSD, resulting in the unpegging of crvUSD. Curve intends to introduce an improved version of Pegkeeper that checks the token price against the composite of other tokens. This will provide better protection by preventing crvUSD deposits from entering unpegging Pegkeeper pools. Currently, the stability of crvUSD depends on strong confidence in the stability of its Pegkeeper pair and low-risk stablecoins.

In the context of being the asset of crvUSD Pegkeeper, there are some criticisms about the transparency policy of TUSD, which deserve special emphasis. TUSD’s transparency is lacking in many aspects, including custodial partnerships, reserve management, verification, on-chain operations, and ownership structure. This report will cover the most concerning issues, which revolve around the status of TUSD reserves, to provide information for DAO voters to determine whether action needs to be taken to limit the risk exposure of crvUSD to TUSD.

Introduction to TUSD

Issuer and Custodian

At a high level, TUSD is a custody stablecoin backed by fiat currency. The design goal of TUSD is to maintain a 1:1 peg with the US dollar, providing stability in the volatile cryptocurrency market. TrueCoin, LLC (a subsidiary of Archblock, Inc.) was the initial issuer of TUSD, but ownership was transferred to Techteryx on December 15, 2020.

According to representatives of TUSD, Techteryx is referred to as an Asia-based conglomerate with operations in Hong Kong, Singapore, Guangzhou, Shenzhen, Beijing, and other locations, spanning traditional real estate, entertainment, environmental, and information technology industries.

However, contrary to its self-proclaimed status as an Asia-based conglomerate, Techteryx Ltd. appears on the register list of the BVI Financial Services Commission. There is very little public information available about Techteryx, which has led to speculation about its subsidiaries and the ultimate beneficial ownership of TUSD.

As of July 13, 2023, Techteryx has taken full responsibility for the management of all offshore operations and services related to TUSD, including minting, redemption, customer registration, compliance, and oversight of banking and trustee relationships.

TUSD has three custodial partners, which are described in the audit report as Hong Kong custodian, Swiss custodian, and Bahamas custodian (the audit report can be downloaded from tusd.io).

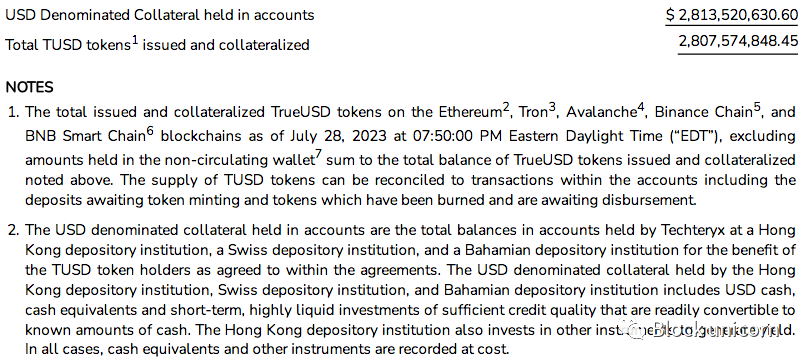

The reserve portfolio is not specifically disclosed, but described as: US dollars, cash equivalents, and short-term, highly liquid investments with sufficient credit quality, which can be easily converted into known amounts of cash. The Hong Kong custodian also invests in other instruments to generate income, and in all cases, the recorded cost of cash equivalents and other instruments.

The main source of TUSD’s revenue is interest earned on the statutory reserve held as collateral. The income generated from these activities helps cover the operational costs of maintaining the stablecoin infrastructure, compliance costs, and supporting the growth and development of TUSD.

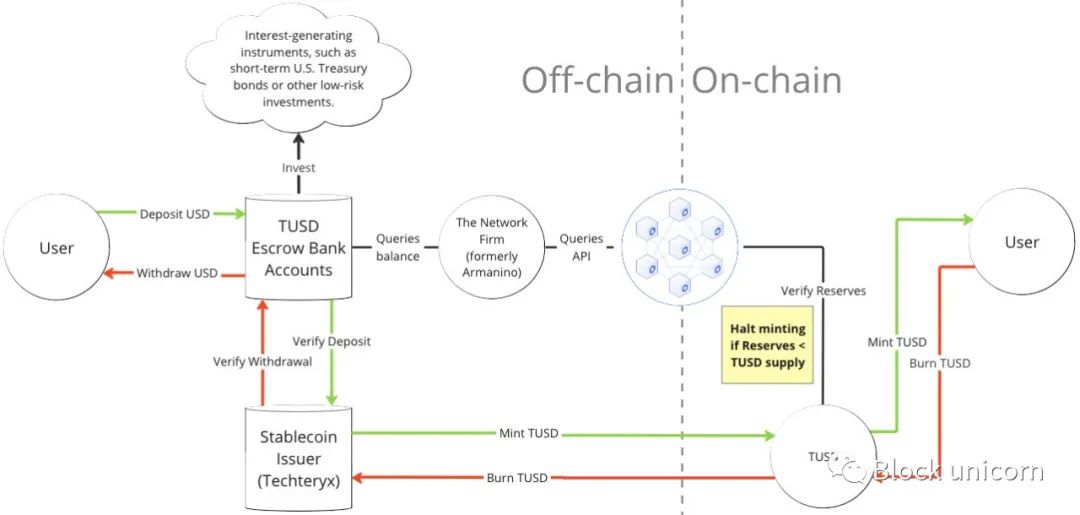

Minting/Redemption Process

The system architecture of TUSD is as follows:

Users who wish to mint TUSD must have an account at https://tusd.io/ and undergo KYC/AML checks. Then, users wire transfer US dollars to a designated bank account managed by the custodial partners. Techteryx emphasizes that fund management is entirely handled by its custodians, and the issuer never has the authority to handle user funds.

TUSD undergoes real-time admission through collaboration with The Network Firm LLP and Chainlink Proof of Reserve (PoR). TUSD can only be minted when the total TUSD supply + newly minted TUSD is less than the reserve reported by Chainlink (provided by The Network Firm). Verified deposits through the minting process are subsequently tokenized, and the corresponding amount of TUSD is issued to the user’s designated receiving wallet.

On the other hand, when users wish to redeem their TUSD for US dollars, they initiate the redemption process with the stablecoin issuer by undergoing KYC/AML checks and specifying their Ethereum and bank wire transfer addresses. TUSD tokens are sent to the TUSD smart contract for burning, and the corresponding amount of US dollars is transferred back to the user’s bank account.

Expansion of TUSD in March 2023

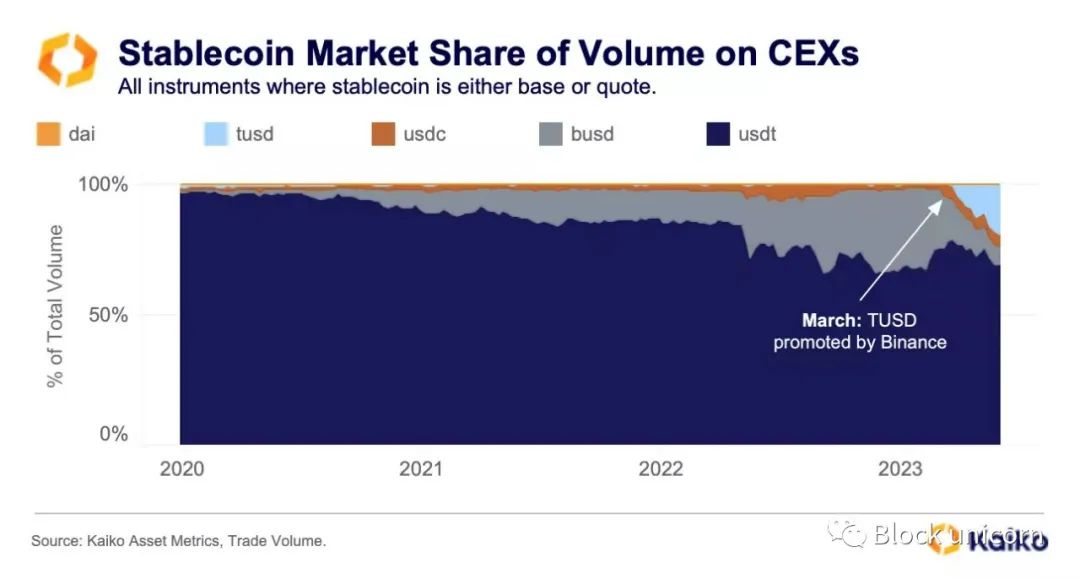

Until March 2023, TUSD was a small-scale stablecoin with limited trading activity, accounting for less than 1% of the overall stablecoin market share. However, Binance decided to adopt TUSD as the successor to BUSD and subsequently promoted the BTC-TUSD trading pair, offering zero trading fees. This significantly increased its visibility and trading volume, rapidly expanding its market share from less than 1% to 19% in just a few months.

Two large transactions worth $1 billion each suddenly appeared, both from the same address, directly sent to Binance exchange. These events occurred on March 12th and June 16th (data date in the following figure: June 27th).

The rapid rise of TUSD may be related to Binance’s zero fee trading promotion and the widespread promotion of TUSD on the exchange. Binance announced this promotion on June 21. Observers may also notice that TUSD’s unusual growth trend coincided with the period before its Prime Trust custody partner closed in mid-June.

After the New York Department of Financial Services (NYDFS) ordered BUSD issuer LianGuaixos to stop issuing its BUSD stablecoin, Binance turned to support TUSD stablecoin. This is because the regulatory issues with Binance’s issuance of BUSD by LianGuaixos have not been resolved. Binance’s move seems to be aimed at maintaining market share in the stablecoin field and reducing dependence on a single stablecoin. Promoting TUSD has made Binance the largest holder of TUSD. It is worth noting that most of TUSD’s trading volume is concentrated in Binance’s BTC-TUSD trading pair.

Token Distribution

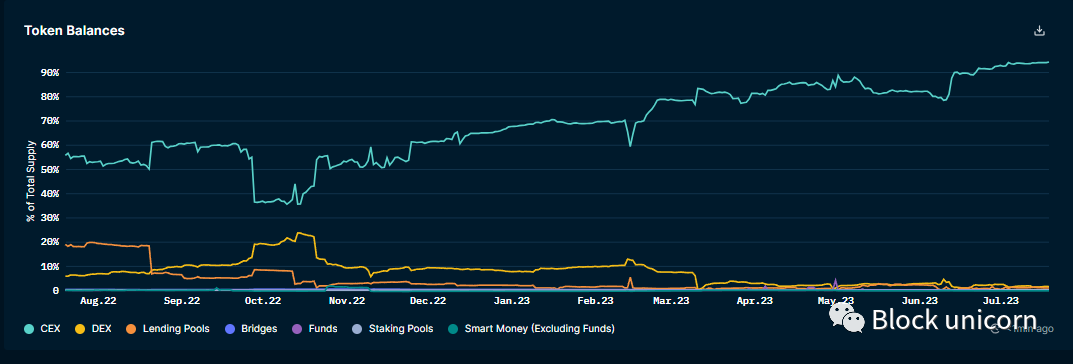

According to data from Nansen on July 19, the majority of TUSD’s supply is held on centralized exchanges (CEX), with 94% of token supply associated with CEX addresses. As shown below, the majority of TUSD is actually held on Binance.

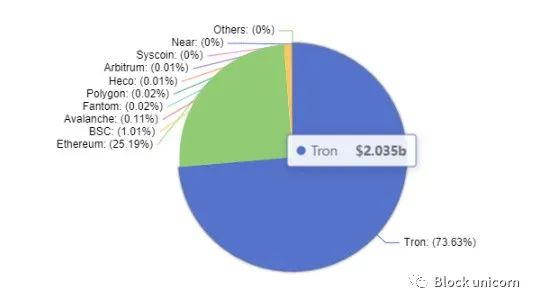

As of the time of writing, the majority of TUSD’s token supply is held on TRON (73.56%), worth approximately $2.035 billion. TUSD’s official website promotes its usage on TRON, Ethereum, Avalanche, Binance BNB Beacon Chain (BNB), and Binance BNB Smart Chain (BSC), and includes the token supplies on these chains in its attestation report (the following image is from data from DeFiLlama on July 19).

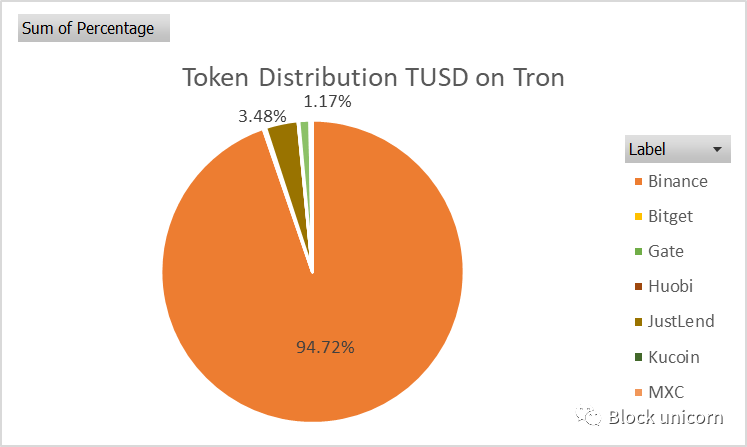

Distribution - TUSD on TRON

On TRON, the majority of TUSD is held by Binance (94.7%), with a small amount held on the DeFi lending platform JustLend (3.5%) and Gate.io (1.2%).

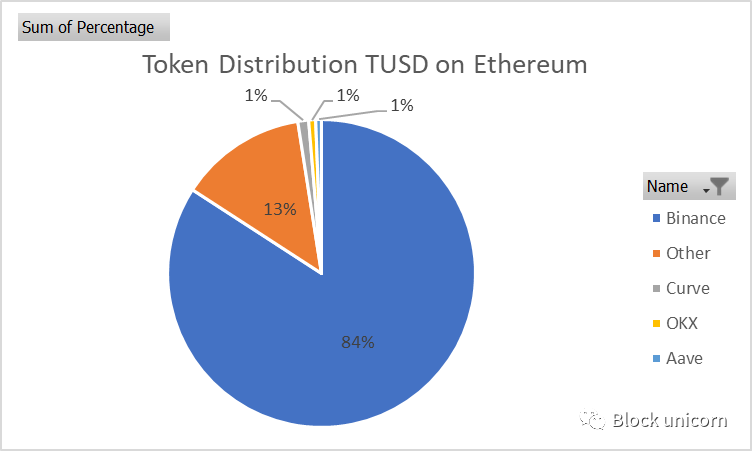

Distribution - TUSD on Ethereum

On Ethereum, TUSD token holders are heavily skewed towards Binance, which holds 83.53% of the total tokens. Curve, OKX, and Aave have smaller shares, at 1.12%, 0.73%, and 0.60% respectively. Curve’s crvUSD/TUSD Pegkeeper pool contains the most TUSD tokens of any contract on Ethereum.

crvUSD Pegkeeper and Decoupling Risk

1. TUSD/crvUSD Pool Contract

2. TUSD Pegkeeper Contract

3. AggregatorStablePrice Contract

The Pegkeeper stabilizes crvUSD’s peg by algorithmically supplying and withdrawing crvUSD to/from the designated Pegkeeper pool. Currently, there are four pools: crvUSD/USDT, crvUSD/USDC, crvUSD/USDP, and crvUSD/TUSD. Each Pegkeeper is allocated a maximum debt that can be supplied to its respective pool. Currently, each Pegkeeper has a maximum debt of 25 million crvUSD, and the total maximum debt for all Pegkeepers is 100 million crvUSD.

The AggregatorStablePrice Contract is crucial for Pegkeepers as it aggregates the price of crvUSD from at least three price sources (currently the four Pegkeeper pools). Only when the crvUSD price referenced by the Aggregator is above $1 will Pegkeepers supply crvUSD.

Using TUSD as an example, the following conditions must be met for Pegkeepers to supply crvUSD:

-

At least 15 minutes have passed since the last update.

-

The TUSD balance in the pool is greater than the crvUSD balance.

-

The crvUSD price referenced by the Aggregator is above $1.

-

If the conditions are met, the supply is equal to 1/5 of the balance difference in crvUSD.

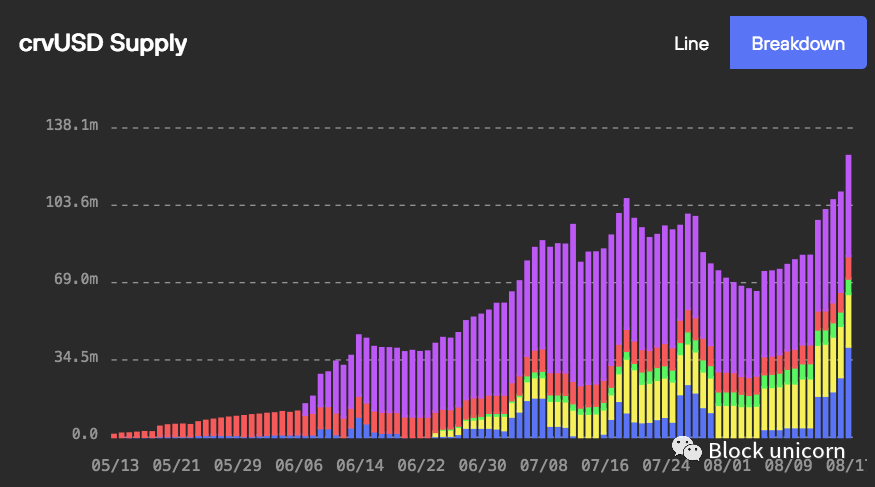

The chart below shows the supply of crvUSD over time divided by source. The blue bars represent the crvUSD supplied by Pegkeepers, reaching a peak of 40.6 million crvUSD (utilization rate of 40.6%) in mid-August. The recent increase in Pegkeeper utilization coincided with a sharp decline in the cryptocurrency market, driving demand for crvUSD. As of August 18th, the total crvUSD supply was 125.5 million, with 85 million borrowed from collateral. This corresponds to Pegkeepers supplying 32.27% of crvUSD and borrowing 67.73% from collateral.

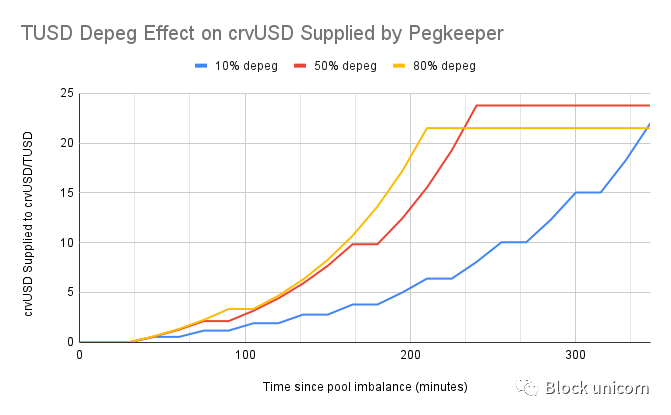

Any decoupling of Pegkeeper assets, whether permanent or long-term, will have adverse consequences. As the Aggregator checks pool balances to determine the price of crvUSD, when Pegkeeper assets decouple, it may mistakenly set the crvUSD quote to >$1. This allows Pegkeepers to supply crvUSD to the pool up to their maximum debt limit. The chart below shows a simulation of how quickly Pegkeepers may supply crvUSD under different degrees of decoupling severity:

This data was collected by simulating the decoupling scenario in Brownie on August 8th, under the pool’s state. Regardless of the degree of decoupling, in a decoupling event lasting 4-5 hours, almost all available Pegkeeper debt will be introduced.

It should be noted that these data are isolated, which in reality would lead to a decrease in the liquidity provided by other crvUSD pools and a proportional loss of anchoring with the unsupported amount of crvUSD entering circulation. The loss of anchoring will lower the price of AggregatorStablePrice quotes, restrict additional Pegkeeper crvUSD from entering circulation, and enable the DAO to take mitigating measures. The crvUSD provided by the Pegkeeper pool that has lost its anchoring will become bad debt for the protocol (assuming the loss of anchoring is permanent).

crvUSD not only relies on its Pegkeeper pools to maintain stability but also depends on them to ensure the continuous solvency of crvUSD. Therefore, it is crucial to assess the protocol’s exposure to potential Pegkeeper debt (i.e., maximum debt) in proportion to the total crvUSD supply and consider the anchoring confidence of each Pegkeeper asset.

Criticism of TUSD Transparency:

1. Non-transparent reserve management: TUSD provides less transparency in its custodial partners and reserve portfolio compared to its competitors.

2. Non-transparent verification: TUSD provides relatively little detail in its documentation, raising questions about the effectiveness of its reserve verification system and potentially giving users a false sense of security.

Criticism 1: Non-transparent reserve management

Vague handling of reserve accounts

TUSD’s documentation does not specifically mention the names of its reserve accounts but rather generically describes its reserves being held in a Hong Kong reserve institution (previously disclosed as First Digital Trust), a Bahamian reserve institution (previously disclosed as Capital Union Bank), and a Swiss reserve institution.

As a significant portion of TUSD’s reserves has been moved to offshore entities, the custodial account structure has become more ambiguous. In a report dated March 16, 2023, TokenInsight stated that the previous operator of TrueUSD, Archblock, had transferred $1 billion of the token’s reserves to Capital Union Bank in the Bahamas due to worsening banking conditions for the US crypto industry. Capital Union Bank, located in Lyford Cay, Nassau, is an independent banking institution that provides private banking services and is regulated by the Central Bank of the Bahamas and the Securities Commission.

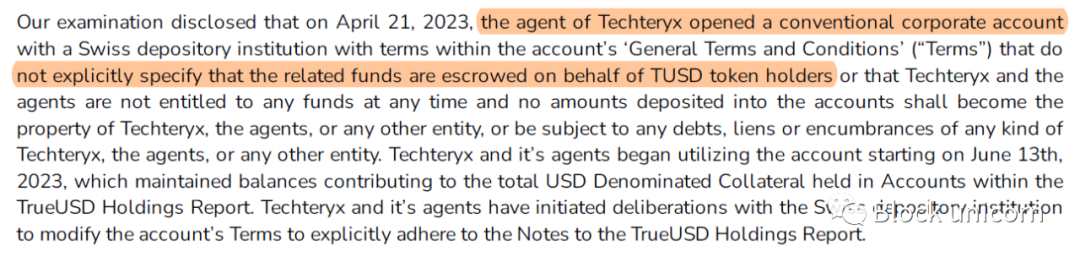

In addition, a recent annotation added to the documentation indicates that Techteryx opened a corporate account with a Swiss reserve institution on April 21. The terms of this account disclosed in the documentation do not explicitly provide significant protections for TUSD holders, namely:

The funds in the account are held on behalf of TUSD token holders.

The agent has no authority to use the funds in the account.

Any amount deposited into the account does not become the property of Techteryx, its agent, or any other entity.

Any amount deposited into the account is not subject to any debt, lien, or encumbrance of Techteryx, its agent, or any other entity.

Excerpts from the documentation regarding the verification are as follows:

The recent addition of this account further highlights the lack of transparency between the reserves held by Techeryx partners and the funds of issuers and users. Such a setup can easily lead to commingling of client deposits or misuse of corporate account funds.

As for the assets held by the unnamed custodian, the portfolio supporting TUSD is disclosed in general terms to include: US dollars, cash equivalents, highly liquid, short-term investments with sufficient credit quality that can be easily converted into known amounts of cash. The custodian in Hong Kong also invests in other instruments to generate income.

There is no further detailed explanation regarding the balance of portfolio assets or the amount held by each custodian, except for this general description. The phrase “other instruments” used in the Hong Kong account is vague. The riskiness of the assets in this account is not clearly indicated, and because the financial statements used for audits are disclosed on a cost basis, these investments may have experienced significant depreciation, which is not reflected in the statements.

Readers are advised to compare the latest statements of TUSD (available on the TUSD website) with those of its main competitors, USDC (June 2023), USDT (June 2023), and USDP (June 2023). In comparison, these issuers disclose more information about custodians and reserve asset portfolios.

June 2023 Market Panic: Prime Trust Bankruptcy

Prime Trust is a Nevada-chartered trust company that provides B2B custody, custody, compliance, regulatory processing, trading software, and other financial services. TUSD has maintained a continuous partnership with Prime Trust since August 2019 when the first cooperation agreement was announced. It utilizes Prime Trust for 24/7 fiat transfers for its stablecoin products, including TrueUSD (TUSD), TrueGBP (TGBP), TrueAUD (TAUD), and TrueCAD (TCAD).

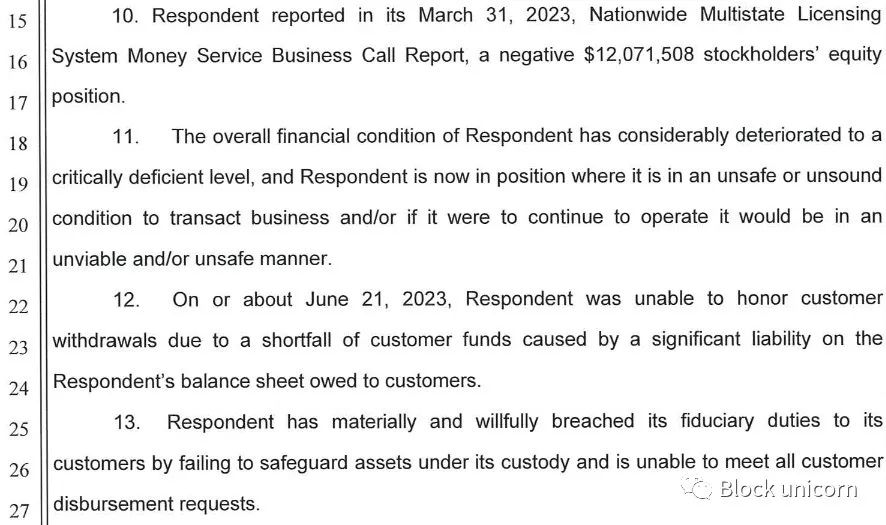

On June 21, 2023, the Nevada Department of Business and Industry’s Financial Institutions Division (FID) ordered Prime Trust to cease all operations due to violations of state regulations. The company’s financial condition was found to be severely deficient, leading to the inability to fulfill customer withdrawals and protect its custodied assets.

In 2020, issues arose with the upgrade of its wallet management system, which apparently led to the discovery in December 2021 that Prime Trust had made funds in its traditional wallets inaccessible. It is alleged that Prime Trust started using deposits from other users to purchase cryptocurrencies to meet withdrawal requests. The Nevada Department of Business and Industry found that the custodian owed customers $85 million in fiat currency while having only $3 million on hand. It claimed that Prime Trust had negative shareholder equity of $12 million and had become effectively unable to repay its debts.

TUSD is exposed to Prime Trust risk.

Before the financial regulatory department in Nevada issued a cease and desist order, there were rumors circulating in the market about TUSD being insolvent. TUSD announced on June 9 that it would temporarily suspend minting through Prime Trust until further notice (other minting/redeeming services are still available). This news triggered a relatively short-lived market panic.

Subsequently, TUSD sharply deviated from its peg on Binance US, dropping to a low of $0.80. It is worth noting that this was not an off-peg event within the market. Binance US faced difficulties in its fight with the U.S. Securities and Exchange Commission, finding banking partners, and the risks associated with Prime Trust, which threatened the exchange’s reliable deposits and withdrawals.

After the issuance of the cease and desist order, TUSD initially announced on June 22 that they had no risk exposure to Prime Trust. However, in the TUSD fund report on June 28, a $26,000 TUSD risk exposure seemed to appear. Although this amount is insignificant, some users reported being unable to mint/redeem TUSD, which continued to cause market panic as market participants remained wary of undisclosed additional risk exposures.

According to TUSD representatives, this $26,000 came from random users’ funds at Prime Trust, which the auditors included in TUSD’s balance sheet, emphasizing that this amount is actually unrelated to TUSD.

Reports of redemption failures

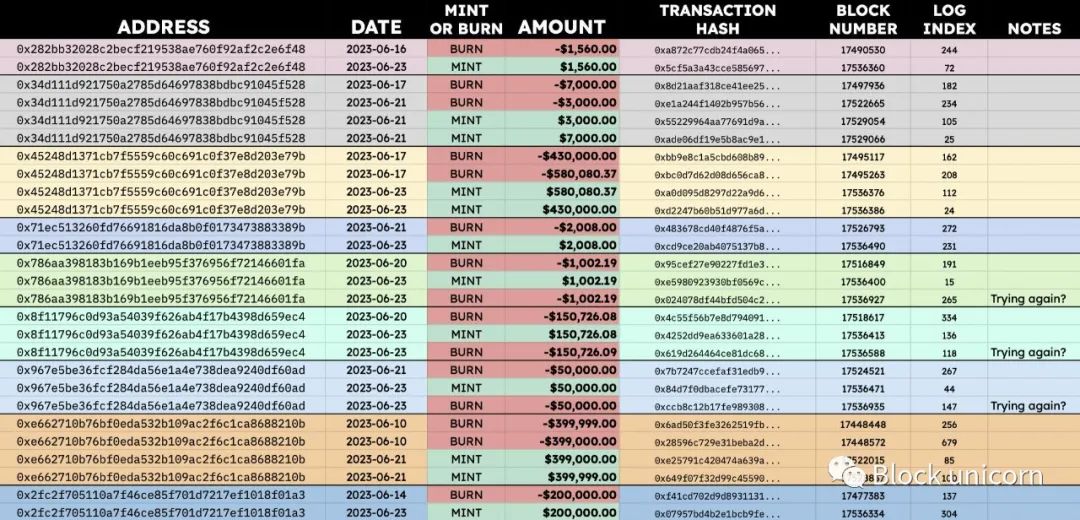

In mid-June, when Prime Trust encountered issues, reports began to emerge claiming that several users seemed unable to cash out TUSD and instead had their TUSD returned to their wallets. This contradicted TUSD’s announcement on June 9, which stated that although minting through Prime Trust had been suspended, all other custodial partners were intact, and minting or redeeming services were not interrupted.

Prime Trust was shut down on June 21, which aligns with the reports of redemption issues. Blockchain analytics company @Chainargos and self-proclaimed former TUSD employee @willmorriss4 provided on-chain transaction records of failed redemption attempts between June 10 and June 23:

TUSD representatives responded that these transactions were attempts by users to send transactions to Prime Trust, despite the public announcement that minting/redeeming through Prime Trust had been suspended. They further emphasized that anyone can still redeem TUSD 24/7 without restrictions through other custodial partners.

Criticism 2: Lack of transparency in verification

LedgerLens system

Real-time confirmation is provided by The Network Firm LLP through their LedgerLens system, which provides real-time reserve data. The service queries the total supply of TUSD on all chains (ETH, AVAX, BNB, TRON, BSC) and the total account balance of Techteryx’s custodial partners across multiple custodial institutions, as shown in the confirmation report from July 28:

Ripcord is an alarm system embedded in the verification service that defines blocking conditions for automatic confirmation updates. They are used to detect systems where external APIs used for confirmation may be unavailable due to maintenance, downtime, or inaccuracy.

There are four types of Ripcord (with a focus on “Balance” Ripcord):

1. Management: Unacknowledged statements, declarations, or terms of participation in the protocol by management during the previous reporting interval.

2. Integration: Errors returned by smart contract calls during the previous reporting interval that would trigger a Balance Ripcord (see below) if excluded.

3. Pricing: Confirmation of stablecoins is irrelevant. Indicates an API error or lack of response from the pricing source application when valuing collateral assets in USD (or other fiat currency).

4. Balance: The response, error, or lack of response from a third-party system or account during the previous reporting interval results in a total liability greater than the total assets. This may be due to normal operations, such as temporary imbalances caused by customers opening bank accounts that have not yet been integrated, or it may be due to actual imbalances between liabilities and assets.

As the situation with Prime Trust gradually unfolded, the “Management” Ripcord was triggered on June 13, followed by the “Balance” Ripcord on June 20. TrueUSD clarified on June 22 that this trigger was caused by delays in the API interface of a newly added banking partner (presumably an unnamed “Swiss custodian”), and at that time, confirmations had returned to normal. A representative from TUSD also mentioned that they are the only stablecoin with real-time confirmations, and the bank’s API cannot reflect the amount in real-time.

Prior criticism in March 2023 pointed out that confirmations for other stablecoin products (including TrueAUD, TrueHKD, TrueCAD, and TrueGBP) have become increasingly outdated, raising concerns about transparency. As of the time of writing, the confirmations for these stablecoins were last updated on June 22, and the “Management” Ripcord is currently triggered.

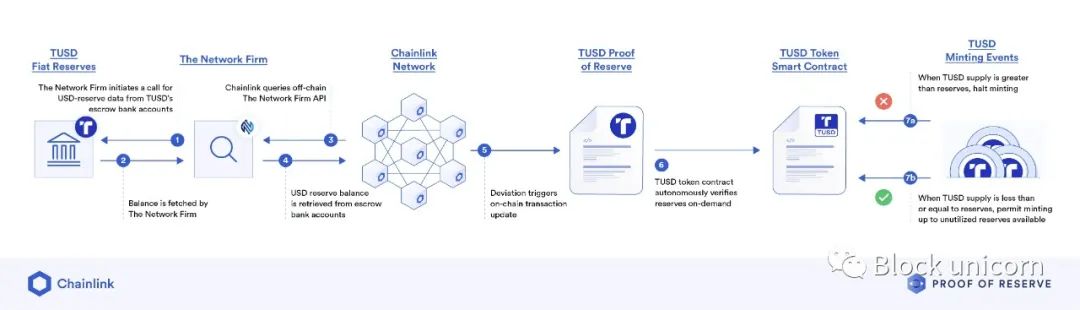

Chainlink PoR Integration Introduction

TrueUSD utilizes Chainlink’s Proof of Reserve (PoR) technology to enhance the transparency and reliability of TUSD by regularly verifying the full collateralization of the stablecoin.

As shown in the above diagram, the minting and redemption processes depend on available reserves and involve the following steps:

1. The independent accounting firm, The Network Firm, requests reserve data in USD from TUSD’s custodial bank account using its LedgerLens attestation service.

2. The USD reserve balance in the custodial bank account is obtained.

3. The decentralized oracle network, Chainlink, queries The Network Firm’s API off-chain.

4. Chainlink retrieves the USD reserve balance reported by The Network Firm API.

5. If there is a discrepancy in the account balance, an on-chain transaction is executed to update the TUSD Proof of Reserve contract.

6. The TUSD token contract autonomously verifies the reserve when necessary.

7. The availability of TUSD minting depends on the comparison between the reserve and TUSD supply:

-

If the TUSD supply exceeds the available reserve, the minting of new TUSD tokens will be stopped to ensure the stablecoin remains fully backed.

-

If the TUSD supply is less than or equal to the reserve, the minting of TUSD tokens will be allowed, up to the unused reserve, to maintain an appropriate collateral ratio.

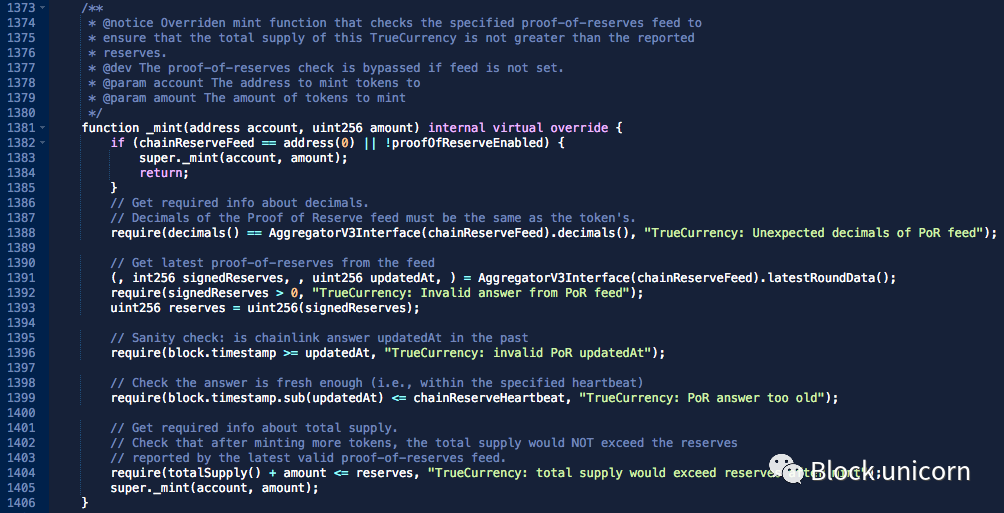

As shown in the following figure, the _mint function of TUSD checks if the reserve value passed from chainReserveFeed is sufficient before allowing the minting of TUSD:

The integration with Chainlink claims to provide users with accurate and transparent information about the reserves supporting TUSD, making it a more reliable collateral and payment method in the DeFi space.

Stablecoin Verification: Insufficient Information

The reserve report of TUSD provided by The Network Firm through Chainlink’s PoR lacks transparency and does not disclose specific details such as:

-

The full scope of the company’s liabilities

-

Bank relationships

-

Composition of the asset portfolio

-

Market value of the reserve (reserve calculated on a “cost” basis)

This makes it difficult for users to comprehensively assess the stability and legitimacy of the reserve.

The purpose of stablecoin verification is to demonstrate the full redeemability and solvency of the entire stablecoin supply, which can be achieved by ensuring both the reserve and liabilities are fully accounted for.

Solvency Proof = Reserve Proof + Liability Proof

Although most of TUSD’s liabilities can be found on-chain (i.e., issued TUSD), there may be significant off-chain liabilities. Audit providers for stablecoins, including The Network Firm (TNF), typically provide reserve snapshots that do not capture the full scope of the company’s liabilities. Hidden or undisclosed liabilities can affect the availability and support of the stablecoin, making the determination of solvency proof more complex.

As mentioned earlier, the custodial institutions that control TUSD reserves are only described as custodians in Hong Kong, the Bahamas, and Switzerland in the audit. The support portfolio for TUSD is also similarly opaque, with disclosure limited to include US dollars cash, cash equivalents, and short-term, highly liquid investments of sufficient credit quality that can be easily converted into known amounts of cash (the custodian in Hong Kong also invests in other income-generating instruments).

Trust Assumptions of The Network Firm LLP

According to the disclosure of TUSD in the Chainlink PoR data source, the audit data is completely dependent on The Network Firm LLP. The credibility and independence of the auditor have been questioned, especially considering the association between The Network Firm and Armanino, which has been subject to scrutiny due to its previous business relationship with FTX US.

The Network Firm has responded to the issue of its association with Armanino, stating it as “accidental or intentional misinformation,” and emphasizing that The Network Firm is an independent accounting firm specializing in the field of digital assets, distinct from Armanino. Many current team members are founding members of Armanino’s digital asset practice. After the failure and controversy surrounding FTX, Armanino decided to reduce its audit services in the digital asset field. The Network Firm LLP was established in October 2022, without any equity from Armanino, and only one founding member has worked on the audit of FTX US’s 2021 financial statements.

The representative of TUSD responded that considering this association as the premise of malicious dissemination (FUD) is unfounded, as Armanino has a business relationship with FTX US, but the latter did not lose customer funds. Armanino is also the auditor for major cryptocurrency platforms such as Kraken. Armanino has confidence in the results of its collaboration with FTX US, and apart from unfavorable media reports related to this association, there is no evidence to suggest any charges of Armanino or The Network Firm failing to fulfill their responsibilities or engaging in any improper behavior.

Regarding the final statement on PoR, although the verification of stablecoins is far from perfect and requires trust in auditors and stablecoin issuers to provide accurate data and responsibly operate their businesses, they are positive steps towards transparency and accountability. By voluntarily conducting and publishing audits, TUSD demonstrates efforts to establish trust between users and regulatory agencies, showcasing a commitment to financial transparency and responsible practices.

On the other hand, some key information has not been disclosed, including custody partners and the relative risk exposure to each institution, the asset composition supporting TUSD, and the company’s liabilities, all of which may impact the support for TUSD. When such information is not disclosed, users need to understand the trust assumptions involved, particularly being aware of the limited usefulness of reserve proof systems like Chainlink PoR when many details are still undisclosed.

Risk Advisory

TUSD has made significant efforts in building trust through real-time verification and on-chain reserve proof, with the feature of being the first USD-backed stablecoin implementing minting restrictions based on off-chain reserves.

However, there is valid criticism regarding Techteryx’s transparency policy, as the issuer does not provide reasonable guarantees regarding the solvency of the stablecoin. Compared to its competitors, TUSD provides limited information about its reserve status. It does not disclose the names of custodial institutions, the balances of each custodian, or the detailed contents of the portfolio. TUSD is currently the only Pegkeeper that does not disclose such information (in comparison to the latest verifications of USDC, USDT, and USDP).

The current Pegkeeper model may cause crvUSD to deviate from its peg or result in protocol bad debt in the event of Pegkeeper asset deviation. Considering the importance of Pegkeepers to the stability of crvUSD, these assets must be specially reviewed and minimum requirements set. Generally, Pegkeeper candidates need to meet the following conditions:

1. Have strong confidence in the anchoring at the technical, operational, and regulatory levels;

2. Candidates should complement the Pegkeeper asset basket by introducing diversity in issuers, custodians, and geographic jurisdictions.

To achieve this goal, candidates should be convertible stablecoins with efficient arbitrage paths and must comply with regulations in their operating jurisdictions. Overall, the Pegkeeper asset basket should not be concentrated in any single jurisdiction, nor should it be concentrated in white-label products with the same issuers and/or custodians (e.g., LianGuaixos USDP and PYUSD).

We believe that TUSD should not be included in the crvUSD Pegkeepers until upgrades are made to crvUSD Pegkeepers and preventive measures are taken to mitigate the negative impact of Pegkeeper asset deviation. Our reason is that, given Techteryx’s current transparency policy, we cannot have confidence in TUSD’s solvency or its anchoring. Reducing the maximum debt of TUSD as a Pegkeeper to zero would not have a significant impact on the overall situation (meaning that even if TUSD cannot continue to act as a Pegkeeper, there are other Pegkeepers that can continue to function and maintain stability) because there are still three other Pegkeepers with a total maximum debt of $75 million. Since May, the highest historical debt utilization of crvUSD by Pegkeepers was $40.6 million (as of August 18).

An argument for reducing the maximum debt, rather than reducing it to zero, may be to ensure geographic diversity among Pegkeepers. Increasing the proportion of Pegkeeper assets established in the United States may increase risks related to US stablecoin regulation. If the DAO agrees with this reasoning, it is suggested to set the maximum debt for TUSD Pegkeeper to a conservative amount, such as $5 million.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Interpreting US Cryptocurrency Taxes General Taxation, Cryptocurrency Taxation, and Future Development Trends

- Outlier Ventures What pain points does the Web3 marketing model solve?

- Ketacoin collides with All In and soars a thousand times, who will be the next Wang Dalu?

- Curve CEO Michael Egorov From Physicist to Cryptocurrency Pioneer

- Quick look at a16z’s new SNARK-based zero-knowledge proof tools Lasso and Jolt

- Social application Friend.tech is hot, how are individual stocks priced?

- A Brief Understanding of the Current Situation of CyberConnect