When can we buy at the bottom? Just like waiting for the fish to die in the market.

When can we buy at the market bottom, like waiting for a dying fish?Source: Metrics Ventures

Crypto Market Secondary Fund Metrics Ventures September Market Observation Guide:

1. The overall market in September was sluggish, with multiple indicators at their lowest levels of the year. Bitcoin and Ethereum chip data show a large number of losses, chips being dumped, and contract positions significantly reduced.

2. MVC’s buying operation. **In mid-September, we conducted moderate buying operations, purchasing about 20% of Ethereum positions. The transaction price was around $1,600. This was mainly based on the following positive signals: after three months of chip fluctuations, potential selling pressure was released to a certain extent; market sentiment showed panic, etc.

3. The main contradiction in the market is still the lack of funds, which cannot be resolved at present.

- Analyst The difference in bull and bear market returns between BTC and ETH can be ignored.

- Galaxy Report The Revolution of Bitcoin Itself

- Bitget Survey Chinese Investors Have Higher Investments in Cryptocurrencies

4. The monthly report uses the metaphor “fish dying in the vegetable market” to describe our current investment strategy. Before determining the trend, we will remain patient and wait for true allocation opportunities to appear.

This article is Metrics Ventures’ overall review and commentary on the market situation and trends of the cryptocurrency market in September.

The title of this month’s report comes from a famous internet meme. An aunt goes to the vegetable market to buy fish and stands by a stall staring at the fish. The vendor is puzzled and asks why the aunt doesn’t buy the fish she likes. The aunt says, for the same fish, the live fish costs 13 yuan and the dead fish costs 3 yuan. I’m waiting for it to die. This is similar to the mentality of many secondary investors who hold a large amount of coins in the current market. They sit on the sidelines and observe quietly, only waiting for the live fish to die before rushing in to buy cheap goods.

Of course, our mentality is also similar. The lively token2049 conference in September is especially like a vegetable market, where some fish have already turned white in their bellies, and some seemingly fat and delicious fish are still flapping. However, everyone knows very well that they won’t last long.

In mid-September, we initiated some position-building actions and mainly bought about 20% of the ETH positions, with an average transaction price of around $1,600. This is because we have observed some marginal changes in emotional and chip signals that we have been watching.

From a chip perspective, we can observe that as the market declines, Bitcoin chips accumulated in the $29,000-$30,000 range are shifting towards the $25,000-$26,000 range. This indicates that the trapped chips due to the expectations of Bitcoin ETF approval and XRP/DCG lawsuit positive expectations are surrendering and selling chips. In addition, the on-chain volume funds provide relatively supportive buying pressure. ETH also has corresponding chip characteristics. Currently, nearly 50% of ETH chips on the chain have realized losses. This is similar to the characteristics of previous panic bottoms, indicating that blood-stained chips at the spot level are being dumped. (Through the observation of on-chain data, we also found that on September 10-11, Arbitrum experienced large-scale whale-selling behavior, with a general loss range of 30-40%. This also represents that since June, the patience of large holders and whales in the market has finally reached its limit.)

From the emotional perspective, market sentiment has quickly turned pessimistic.

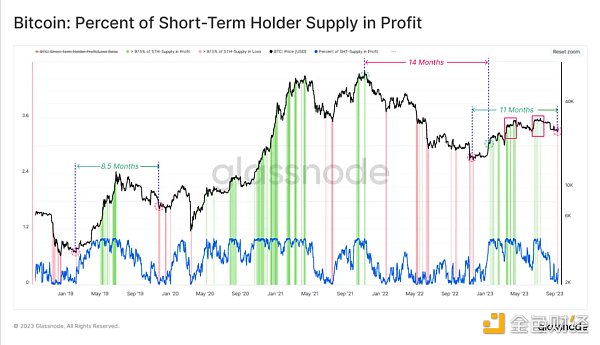

From the above chart, it can be observed that after nearly 11 months of market consolidation, more than 97.5% of short-term BTC chips are in a floating loss. The price dropped from around $30,000 to around $25,000, which may not seem like a huge decline, but the pain of cutting losses and selling off is actually very intense. This level of market clearance should bring about a calm period of about one month.

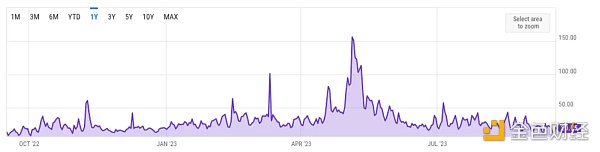

From the observation of contract positions, in early September, the BTC contract positions on Binance platform alone decreased from a peak of $4.81 billion to $2.88 billion, a decrease of about 40%. At the lowest point in January 2023, this number was $2.52 billion, and during the March US banking crisis, this number was about $2.85 billion. This indicates that a series of positive expectations falling short in September has indeed greatly destroyed the confidence of market participants and led to a strong cleansing of leverage in the market. Moreover, during the whole of September, the contract’s OI position volume recovered slowly, the fees were moderate, and it was basically in a depressed sentiment where no one dared to go long or short.

If we look more closely, from the following chart of BTC’s hourly market, we can roughly observe that the narrow range volatility in September was hellish for contract funds. The phenomenon of trapping traders occurred frequently, leading to liquidation whether the price went up or down. The liquidation happened repeatedly (poor traders). So it is quite obvious that the sentiment around $27,000 for Bitcoin is actually more depressed than the sentiment around $16,000, showing clear bearish characteristics. The whole of September and even October belong to a phase of oscillation and digestion of trapped selling pressure.

Not only is the sentiment of spot and contract trading low, even the on-chain Meme market that extreme left players like to speculate on is completely cold. As shown in the chart below, ETH network Gas base has reached a new low for the year, and ETH has entered a rare state of inflation since the completion of the Merge, with a heavier sense of coldness compared to the freezing point in December 2022. Based on our monitoring of Mempool transaction data, the activity of tokens without transaction fees has sharply decreased.

Furthermore, in September 2023, the DEX trading volume has not exceeded 30 billion, which is even lower than the 40 billion in December 2022, and it has set a new record low for monthly DEX trading volume since 2021. This also matches the market sentiment that we intuitively feel. The market heat at $27,000 for BTC is even lower than when it was at $16,000.

When we observe trapped selling, extreme low sentiment, and choose to enter the market with small-scale bottom fishing, it does not mean that we believe there will be significant rebound opportunities in the short term. It’s just that the current position has released blood-stained spot chips (realized loss chips account for a high proportion), leverage cleaning is relatively thorough (position volume is close to the lowest for the year, long/short ratio is low), sentiment is extremely low (volume is weaker), and the market has given a signal of inclination to take over. The current position has a relatively good risk-reward ratio, and as a long-term allocation, the price is also reasonable. Even if there are signs of potential sharp declines in the short term, we can stop loss and exit at a clear target with minimal cost.

Recently, there have been screenshots circulating widely in the market about the BTC calendar effect, which mainly means that the cryptocurrency market tends to perform well in October each year, and there will also be a grand Alt Season. The calendar effect can be considered mystical, and we do not have high expectations for the market in October.

Currently, the market has barely caught its breath from the game of reduced supply. The total market value of the top five stablecoins has not significantly decreased in the past month, and it can be considered an upgrade to a stock game. In this situation, the market is more inclined towards oversold rebounds, with limited upside potential and upward momentum at the spot level. Since all on-exchange players generally have low positions, there is buying pressure from short covering. Through market research, we have found that secondary institutions and individual investors with funds over one hundred million US dollars choose to make small-scale bottom fishing with a dollar-cost averaging mentality.

If there really is an alt season, due to weak market liquidity and low market capitalization, the funds from some short covering may bring about significant price increases. However, there will also be a large number of altcoins competing for funds, resulting in extremely rapid sector rotation and poor sustainability of the market. It is estimated that there will be limited profit-making effects, and the value of participating in short-term trading is low. Moreover, if one does not escape quickly enough, they may become unfortunate victims of the liquidity drain.

The market is stagnant, with consecutive new lows in volatility and a slow increase in the proportion of long-term locked chips. Short-term investors repeatedly chase high and cut losses, leading us into a dull state where we cannot go up or down – the main contradiction in the market is still the lack of funds, which cannot be solved at the moment.

The core constraint of the main contradiction lies with the Federal Reserve. In the September Fed interest rate meeting, an interest rate hike was put on hold, but the market interpreted it as interest rates remaining high in the long term. During the October holiday period, which also coincides with the US government’s new fiscal year budget resolution, US bond yields rose to 2008 levels, and US stocks, gold, and oil plummeted, while the US dollar strengthened. Overseas markets experienced severe shocks, and signs of liquidity tightening have already emerged – this is also the main consensus in the current crypto market. Those whales who have not lost all their money and are closely monitoring the fishpond are generally waiting for the collapse of the US stock market in 2023Q4-2024Q1, using the stock market crash or interest rate cuts as a signal that the fish has completely stopped breathing (the echoes of the 312 memory linger).

We will continue to keep an eye on this, but we must emphasize that since 2023, we will not rely on macro information to guide our investment decisions in the crypto market. We are not macro experts, and the end of an interest rate hike cycle does not necessarily mean the beginning of an interest rate cut cycle. Each interest rate cut only happens after risks have emerged, and it is not a prior signal; at the end of each interest rate hike cycle, a bubble will burst in some corner of the earth, and it may not necessarily be the US stock market this time; whether it will collapse or not, and when it will collapse – these various factors are not helpful for our decision-making process.

In short, the market is currently short of money, and for a while, we don’t know where the liquidity will come from. What we may need to face is a situation where Bitcoin oscillates within a 15% fluctuation range indefinitely. Oh fish, oh fish, when will you suffocate?

In summary, the cryptocurrency market remains in a slump in September, and we maintain a cautious attitude. Volatility and oscillation may continue until the market’s funding situation improves. We will continue to focus on the fundamentals, make appropriate allocations, and patiently wait for the right buying opportunities.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Will the super bear steepening of the US Treasury yield curve be a blessing or a curse for the cryptocurrency market?

- LianGuai Daily | Hong Kong officially regulates stablecoins and temporarily does not allow retail trading; El Salvador launches its first Bitcoin mining pool

- Understanding the Current Status and Future Development Direction of Blockchain Data Business with One Article

- NDV Practical Insights Profit and Cost Analysis of BTC Mining Industry

- Calls for the adoption of cryptocurrencies are rising in sub-Saharan Africa.

- Galaxy Digital Bitcoin Ordinals Protocol Research Report Important Data, Impact on Bitcoin, and Latest Developments

- Andrew Kang Cryptocurrency and stock market correlation has dropped to a low level and will continue to stay that way.